Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

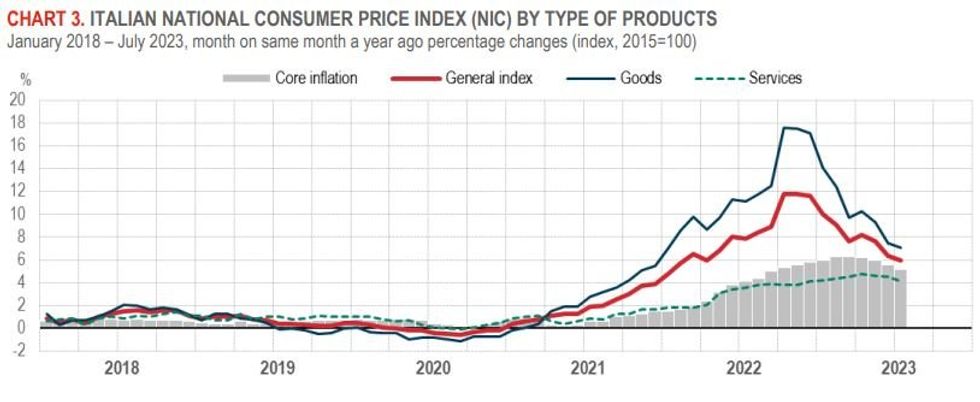

Italian NIC (CPI for the whole nation) inflation readings came in on the high side vs expectations in July's flash estimates vs June, at +0.1% M/M (vs -0.2% survey , 0.0% prior) and +6.0% Y/Y (5.9% survey, 6.4% prior). But the latter was the lowest since April 2022, and HICP was a little soft vs expectations, at -1.5% M/M (-1.4% survey, +0.1% prior) and +6.4% Y/Y (6.5% survey, 6.7% prior).

- There were no analyst survey expectations for core, but NIC core came in at 5.2% Y/Y vs 5.6% prior; ex-energy was +5.6% vs 5.8% prior. And core HICP (ex energy and unprocessed food) decelerated to 5.7% Y/Y from 6.1% prior.

- Energy prices had been largely expected to be a major driver in the headline slowdown and decelerated to 0.7% Y/Y vs 2.1% prior, helping goods prices retrace to 7.1% Y.Y vs 7.5% prior; services pulled back to +4.1% Y.Y vs 4.5% prior.

- The divergence in the monthly NIC vs the relatively soft HICP appears to be methodological, with Istat noting "summer sales (in HICP) not considered by NIC"). Non-energy industrial goods rose +0.1% M/M in the NIC CPI, vs -5.2% M/M in the HICP series.

- Breaking the Y/Y NIC slowdown further, it came on the back of a slowdown in price pressures in transport services (2.4% Y/Y vs 4.7% prior), non-regulated energy products (7.0% vs 8.4% prior), with other disinflationary categories noted by Istat including processed food incl alcohol; nonenergy industrial goods; misc services; and tobacco.

- On the upside, stronger contributors included unprocessed food (10.4% Y/Y vs 9.4% prior) and housing services (+3.6% vs 3.5% prior).

- On a monthly basis, the major contributors in processed food including alcohol (+0.9%, as opposed to the Y/Y slowdown) and various services, while unprocessed food, energy products, and tobacco prices all declined M/M.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok