Highlights:

- Undecided voters the focus for first Presidential debate between Trump and Biden

- SEK slips as Riksbank choose easier policy path for 2024/25

- Tertiary GDP, weekly claims and prelim durable goods mark calendar highlight

US TSYS: Consolidation Of Bear Steepening, Data Ramps Up With Further Supply

- Treasuries consolidate yesterday’s sizeable bear steepening ahead of important data including GDP revisions, preliminary durable goods and jobless claims, all before tomorrow’s May PCE report. Further supply is in the mix as well with 7Y supply coming after yesterday’s solid (but shrugged off) 5Y auction added to a well-received 2Y on Tuesday.

- Cash yields sit within 0-0.5bp either side of yesterday’s close having rallied a little in recent trade. 2s10s at -41.8bps is off recent ytd lows of -50.8bps.

- TYU4 has kept to narrow ranges overnight on strong cumulative volumes of 400k.

- At 109-31+ (-02+) it’s close to the earlier low of 109-27+ that marked a step closer to support at 109-26 (50-day EMA) in a further test of the bullish trend. Clearance here could open a key support at 109-00+ (Jun 10 low).

- Data: GDP Q1 3rd release (0830ET), Durable goods May prelim (0830ET), Weekly jobless claims (0830ET), Advance trade balance May (0830ET), Wholesale & retail inventories May prelim/May (0830ET), Pending home sales May (1000ET), KC Fed mfg Jun (1100ET)

- Note/bond issuance: US Tsy $44B 7Y Note auction - 91282CKW0 (1300ET)

- Bills issuance: US Tsy $80B 4W, $75B 8W bill auctions (1130ET)

- Presidential debate 2100ET

STIR: Fed Rates Hold Reversal Of Retail Sales Miss But Struggle To Push On

- Fed Funds implied rates consolidate yesterday’s increase, which came primarily from further overseas inflation strength before a small lift late in the session.

- The Dec’24 implied rates of 4.89% (for 44bp of cuts) has unwound the decline seen on last week’s retail sales miss but has struggled to push much higher ahead of important data over the next two days after a light start to the week. For context, it remains below the 4.94% seen prior to the May CPI report.

- Cumulative cuts from 5.33% effective: 3bp Jul, 17bp Sep, 26bp Nov, 44bp Dec and 57bp Jan.

- There’s no Fedspeak scheduled today. There are some limited appearances scheduled tomorrow but focus is on Powell’s Sintra appearance on Tuesday.

US TSY FUTURES: OI Suggests Little Net Positioning Movement On Wednesday

Little to note when it comes to net positioning movement on Wednesday.

- The combination of the move lower in Tsy futures and open OI points to a mix of relatively modest net long cover and short setting, with the former slightly more prominent.

- Pre-supply concession and firmer-than-expected Australian CPI provided much of the pressure.

| 26-Jun-24 | 25-Jun-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,143,790 | 4,152,718 | -8,928 | -343,718 |

| FV | 6,199,179 | 6,200,108 | -929 | -39,315 |

| TY | 4,343,021 | 4,329,185 | +13,836 | +893,493 |

| UXY | 2,048,224 | 2,053,436 | -5,212 | -466,031 |

| US | 1,643,773 | 1,645,762 | -1,989 | -261,686 |

| WN | 1,670,416 | 1,672,550 | -2,134 | -432,799 |

| Total | -5,356 | -650,056 |

STIR: OI Points To Mix Of SOFR Short Setting & Long Cover On Wednesday, Aus CPI The Latest Driver

The combination of OI data and yesterday’s move lower in SOFR futures points to a mix of net short setting and long cover.

- Individual contract OI swings were limited, with the most prominent net positioning moves seemingly coming via net long cover in SFRM4 through Z4 and net short setting in SFRH5 through Z5.

- Firmer-than expected Australian CPI data provided much of the pressure.

- FOMC-dated OIS moved to priced ~41bp of cuts through ’24 vs. 44.5bp late on Wednesday.

| 26-Jun-24 | 25-Jun-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRM4 | 1,222,899 | 1,226,551 | -3,652 | Whites | -3,525 |

| SFRU4 | 1,146,990 | 1,149,041 | -2,051 | Reds | +11,594 |

| SFRZ4 | 988,112 | 991,030 | -2,918 | Greens | +875 |

| SFRH5 | 814,748 | 809,652 | +5,096 | Blues | +8,744 |

| SFRM5 | 699,230 | 692,763 | +6,467 | ||

| SFRU5 | 626,394 | 621,084 | +5,310 | ||

| SFRZ5 | 813,704 | 810,760 | +2,944 | ||

| SFRH6 | 560,626 | 563,753 | -3,127 | ||

| SFRM6 | 479,142 | 479,720 | -578 | ||

| SFRU6 | 420,158 | 420,447 | -289 | ||

| SFRZ6 | 357,030 | 354,082 | +2,948 | ||

| SFRH7 | 239,295 | 240,501 | -1,206 | ||

| SFRM7 | 227,311 | 221,445 | +5,866 | ||

| SFRU7 | 183,818 | 182,205 | +1,613 | ||

| SFRZ7 | 172,721 | 171,129 | +1,592 | ||

| SFRH8 | 113,956 | 114,283 | -327 |

EUROPE ISSUANCE UPDATE:

Italy auction results

- E3.5bln of the 3.35% Jul-29 BTP. Avg yield 3.55% (bid-to-cover 1.42x).

- E3.5bln of the 3.85% Jul-34 BTP. Avg yield 4.01% (bid-to-cover 1.44x).

- E1.75bln of the 1.05% Apr-32 CCTeu. Avg yield 5.04% (bid-to-cover 1.61x).

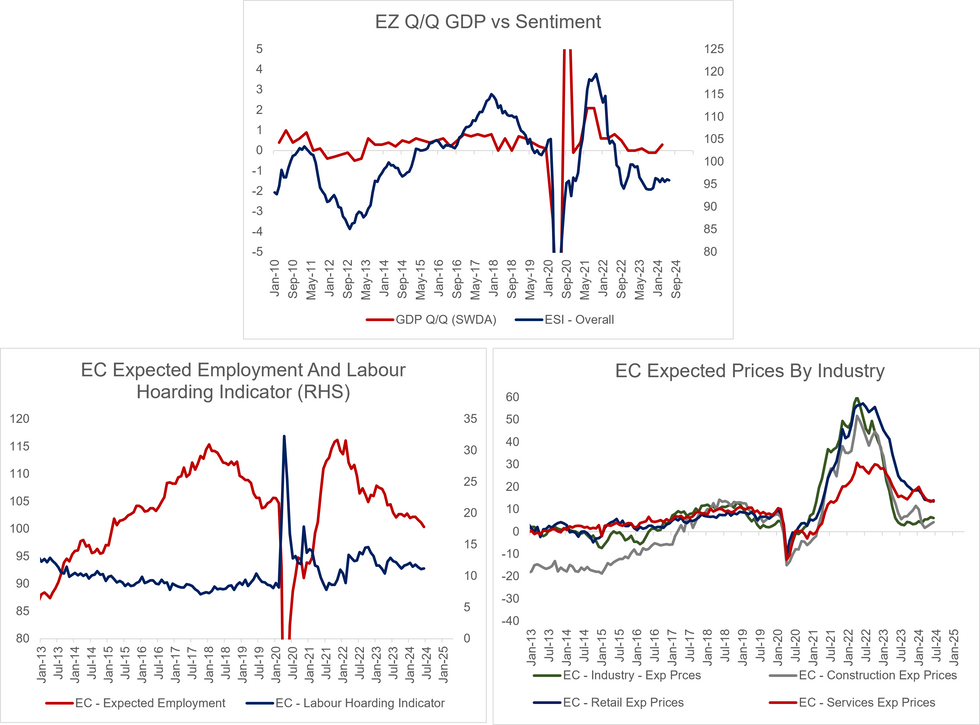

EUROZONE DATA: Services Expected Prices Remain At Elevated Levels

The EC’s June business and consumer survey saw overall Economic Sentiment (ESI) moderate slightly to 95.9 (vs a one tenth upwardly revised 96.1 prior and 96.1 cons). This reflected a small improvement in consumer sentiment (-14.0 vs -14.3 prior) but falls in business sentiment across industries.

- ESI, which is a reasonable forward-looking indicator for turning points in GDP growth, suggests little change from the 0.3% Q/Q registered in Q1. Bloomberg consensus for Q2 currently stands at 0.2% Q/Q.

- On the inflation front, services expected prices ticked up to 14.1 (vs 13.4 prior), reversing May’s fall. At a country level, Belgium saw a 4.1-point rise in expected prices, while Spanish and French expectations ticked higher to a lesser extent. Italian price expectations fell 1.3 points, while Germany was broadly unchanged.

- Overall, services expected prices are off cycle highs, but remain at elevated levels.

- Industry and retail expected prices fell in June, though the overall signal that core goods HICP should stall in the coming months remains intact.

- The Expected Employment metric fell slightly, while the labour hoarding indicator was broadly unchanged.

FOREX: SEK Slips as Riksbank Raises Risk of Summer Rate Cut

- Antipodean currencies trade well, with AUD and NZD firmer against most others to allow AUD/USD to consolidate the post-CPI gains from this week. Despite the Thursday strength, the pair remains just inside its well-worn range of the past six weeks, keeping the technical parameters unchanged for now: 0.6704/14 to the upside, and the 50-dma of 0.6612 to the downside.

- The USD Index remains above the 106.00 handle, and within range of yesterday's multi-month high printed at 106.130. Firmer-than-expected US data later today or renewed concerns surrounding French politics could tip the dollar again to multi-month highs.

- ECB members Muller, Kazimir and Lane stuck to the recent script in comments to press today, leading markets into a quieter Summer for ECB policy ahead of the September meeting, at which markets currently price a better-than-even chance of the next rate cut.

- The Swedish central bank kept headline policy unchanged, however a dovish set of rate path projections and CPI forecasts leant against the SEK, putting EUR/SEK to late June highs, pushing against the broader downtrend in the cross posted off the early May highs. SEK is comfortably the poorest performing currency in G10 headed into the NY crossover.

- The tertiary read of Q1 US GDP is set to cross alongside the weekly jobless claims data, although prelim durable goods orders could be more consequential for markets. The central bank speaker slate is far quieter, with no Fedspeak of note, however RBA deputy governor Hauser appears at 1030BST/0530ET.

Expiries for Jun27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0650(E2.4bln), $1.0700(E3.5bln), $1.0725(E625mln), $1.0740-50(E2.0bln), $1.0800(E912mln)

- USD/JPY: Y160.00($944mln)

- USD/CAD: C$1.3675-85($1.5bln), C$1.3700-05($1.4bln)

COMMODITIES: Current Bull Phase in WTI Futures Remains Intact

- WTI futures are still trading closer to their latest highs and the current bull phase remains intact. The recent move higher has resulted in a break of $80.11, the May 29 high and a key resistance. The clear breach of this hurdle cancels a bearish theme and paves the way for $82.24, a Fibonacci retracement point. Initial firm support to watch is $78.63, the 50-day EMA. A break would be seen as an early potential reversal signal.

- A bear threat in Gold remains present and the yellow metal continues to trade below resistance. A sharp sell-off on Jun 7 reinforced a short-term bearish theme. Price has again pierced the 50-day EMA, at 2317.7. A clear break of this EMA would confirm a resumption of the reversal from May 20 and open $2277.4, the May 3 low. Clearance of this price point would also strengthen a bearish theme. Initial firm resistance is $2387.8, the Jun 7 high.

EQUITIES: E-Mini S&P Consolidates Near Recent Highs

- The trend condition in Eurostoxx 50 futures remains bullish. The recovery from the Jun 14 low is potentially an early reversal signal highlighting the end of the May 16 - Jun 14 correction. Resistance to watch is at 5039.84, a Fibonacci retracement. Clearance of this level would be a positive development. A reversal lower would signal a resumption of the bearish corrective cycle. This would open 4846.00, the Apr 19 low and a key support.

- S&P E-Minis are in consolidation mode. The trend condition is unchanged and signals remain bullish with price trading closer to its recent highs. Resistance at 5430.75, the May 23 high and bull trigger, has been cleared. This confirmed a resumption of the uptrend. Note that MA studies are in a bull-mode position, highlighting positive sentiment. Sights are on 5594.66, a Fibonacci projection. Support to watch is 5473.37, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 27/06/2024 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 27/06/2024 | 1215/1415 | ECB's Elderson speech on Banking Supervision at Allen & Overy | ||

| 27/06/2024 | 1230/0830 | *** | Jobless Claims | |

| 27/06/2024 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 27/06/2024 | 1230/0830 | *** | GDP | |

| 27/06/2024 | 1230/0830 | * | Payroll employment | |

| 27/06/2024 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/06/2024 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 27/06/2024 | 1400/1000 | ** | NAR Pending Home Sales | |

| 27/06/2024 | 1430/1030 | ** | Natural Gas Stocks | |

| 27/06/2024 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 27/06/2024 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 27/06/2024 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 27/06/2024 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 27/06/2024 | 1900/1500 | *** | Mexico Interest Rate | |

| 27/06/2024 | 2000/1600 | Topic of meeting | ||

| 28/06/2024 | 2330/0830 | ** | Tokyo CPI | |

| 28/06/2024 | 2330/0830 | * | Labor Force Survey | |

| 28/06/2024 | 2350/0850 | ** | Industrial Production | |

| 27/06/2024 | 0100/2100 | Trump-Biden Debate | ||

| 28/06/2024 | 0600/0700 | *** | GDP Second Estimate | |

| 28/06/2024 | 0600/0700 | * | Quarterly current account balance | |

| 28/06/2024 | 0600/0800 | ** | Import/Export Prices | |

| 28/06/2024 | 0600/0800 | ** | Retail Sales | |

| 28/06/2024 | 0645/0845 | *** | HICP (p) | |

| 28/06/2024 | 0645/0845 | ** | PPI | |

| 28/06/2024 | 0645/0845 | ** | Consumer Spending | |

| 28/06/2024 | 0700/0900 | *** | HICP (p) | |

| 28/06/2024 | 0700/0900 | ** | KOF Economic Barometer | |

| 28/06/2024 | 0755/0955 | ** | Unemployment | |

| 28/06/2024 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/06/2024 | 0900/1100 | Flash inflation | ||

| 28/06/2024 | 1000/0600 | Richmond Fed's Tom Barkin | ||

| 28/06/2024 | 1230/0830 | ** | Personal Income and Consumption | |

| 28/06/2024 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 28/06/2024 | 1345/0945 | *** | MNI Chicago PMI | |

| 28/06/2024 | 1400/1000 | ** | U. Mich. Survey of Consumers | |

| 28/06/2024 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 28/06/2024 | 1600/1200 | *** | USDA Acreage - NASS | |

| 28/06/2024 | 1600/1200 | ** | USDA GrainStock - NASS | |

| 28/06/2024 | 1600/1200 | Fed Governor Michelle Bowman | ||

| 28/06/2024 | 1640/1240 | San Francisco Fed's Mary Daly | ||

| 28/06/2024 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |