Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

STIR

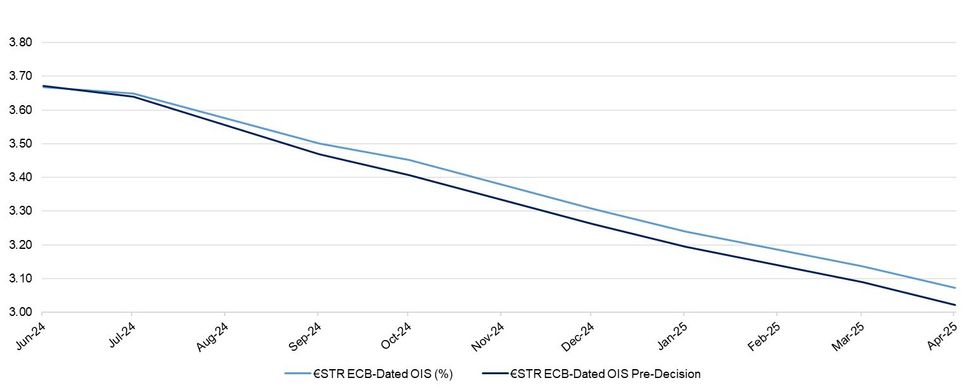

Initial market reaction to the ECB’s widely expected cut is hawkish, with the ECB not pre-committing to further cuts, underscoring its data dependent approach.

- ’24 and ’25 CPI inflation forecasts were marked higher, topping the median of sell-side forecasts that we saw ahead of the event by 0.1ppt, which also helps explain the hawkish move.

- Euribor futures are 1.0-8.0bp lower, just off post-ECB session lows.

- ECB implied rates are little changed to ~5bp above the levels we flagged ahead of the meeting, still showing very slim odds of a follow up cut in July.

- A follow up cut through October is now only ~85% priced, after being fully discounted in the lead up to the decision.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Cut Adjusted Effective €STR Rate (bp) |

| Jun-24 | 3.667 | +0.4 |

| Jul-24 | 3.648 | -1.5 |

| Sep-24 | 3.501 | -16.3 |

| Oct-24 | 3.451 | -21.2 |

| Dec-24 | 3.306 | -35.7 |

| Jan-25 | 3.239 | -42.5 |

| Mar-25 | 3.137 | -52.6 |

| Apr-25 | 3.073 | -59.1 |

Source: MNI/Bloomberg. 2025 dates are estimated.

Source: MNI/Bloomberg. 2025 dates are estimated.

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok