Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ECB

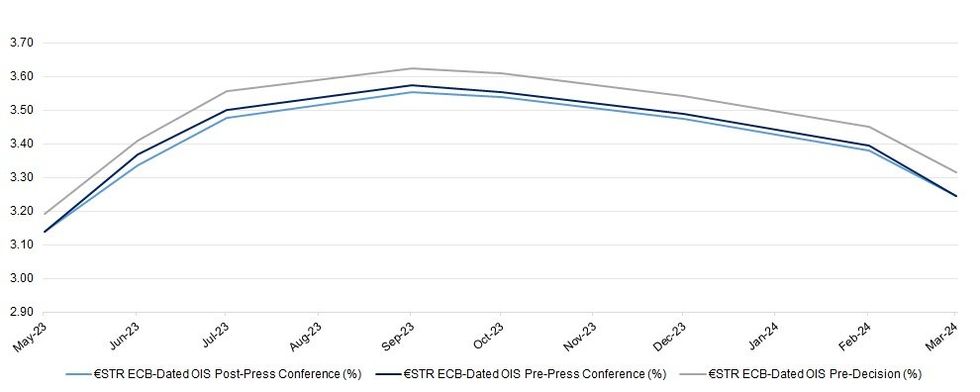

Little in the way of net movement in ECB-dated OIS pricing during Lagarde’s press conference, allowing the post statement downtick to consolidate/extend at the margin, with terminal rate pricing pulling in by ~10bp vs. pre-meeting levels, sitting at 3.55% in €STR terms, which equates to ~3.65% in deposit rate terms (or 40bp more of tightening, give or take).

- As a reminder Lagarde played down the idea that the move re: expectations to discontinue reinvestments under the APP as of July 2023 was a trade-off to placate the hawks that were calling for a 50bp step today (pointing to a liquidity impact that would complement interest rate settings), while she gave a bit of a mixed response re: the idea of sufficiently restrictive interest rate levels and highlighted more work to do, refuting any idea of an imminent pause in the tightening cycle and pointing to the deliberate use of the plural “meetings” in the statement.

- On the TLTRO front, her response to a question re: potential concerns surrounding the large repayment due in June was that “there is no surprise about TLTRO. If anything (we) have managed to get banks to accelerate repayment and reduce the cliff effect. It's a due date, banks have prepared for it. There is a lot of liquidity out there.” She also noted that she wouldn’t be surprised if liquidity windows available start to become used. If anything were to happen on that front, she noted that the ECB has those facilities in place with full allotment available. There was no rhetoric re: a bridging facility surrounding the TLTRO repayment.

| ECB Meeting | €STR ECB-Dated OIS Post-Press Conference (%) | €STR ECB-Dated OIS Pre-Press Conference (%) | €STR ECB-Dated OIS Pre-Decision (%) |

| May-23 | 3.140 | 3.140 | 3.192 |

| Jun-23 | 3.335 | 3.369 | 3.410 |

| Jul-23 | 3.476 | 3.500 | 3.557 |

| Sep-23 | 3.553 | 3.573 | 3.623 |

| Oct-23 | 3.539 | 3.555 | 3.608 |

| Dec-23 | 3.473 | 3.488 | 3.541 |

| Feb-24 | 3.380 | 3.394 | 3.450 |

| Mar-24 | 3.245 | 3.246 | 3.315 |

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok