Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

KRW

Spot USD/KRW got close to 1298 earlier, through the 2020 high and fresh highs going back to 2009. Net equity outflows persist, but we remain above previous trough points from a momentum standpoint. Spot USD/KRW is also elevated relative to its own 200 day MA but implied vols and risk reversals paint a more benign picture.

- The Kospi remains an underperformer in the regional equity context, down close to 2%. As we highlighted earlier, equity outflows persist, now at $281mn for day.

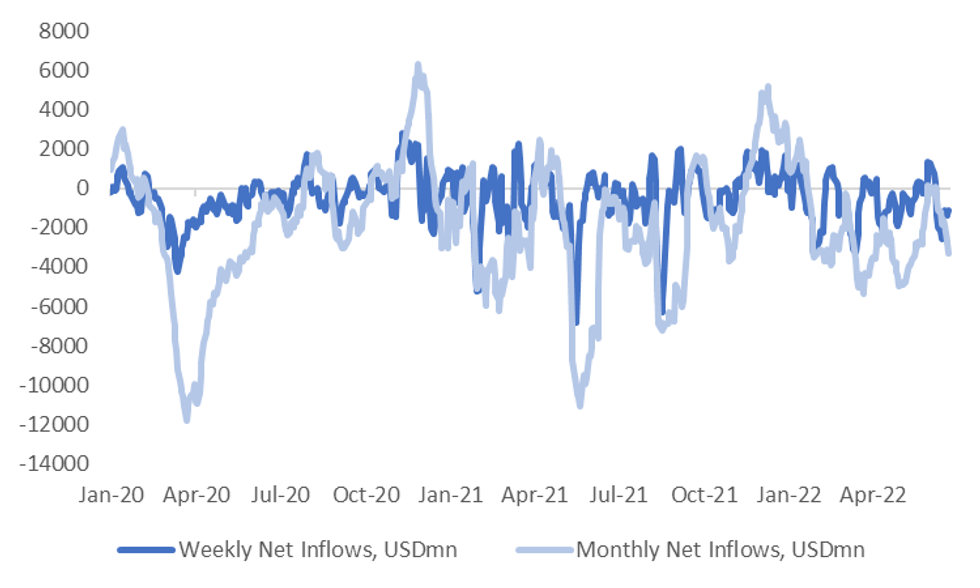

- The first chart below plots the trends for the rolling weekly and monthly net equity flow picture. The past 5 trading sessions has seen just over $1.1bn in net outflows according to exchange data, while the past month has seen just under $3.3bn in net outflows.

- Whilst clearly negative, we remain above trough points seen in recent years, as the chart demonstrates.

- Year to date net outflows are also very large at more than $15bn, but remain below net outflows seen for 2020, 2021 and 2008.

Fig 1: Equity Outflows Persist But Not at Extremes Yet

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

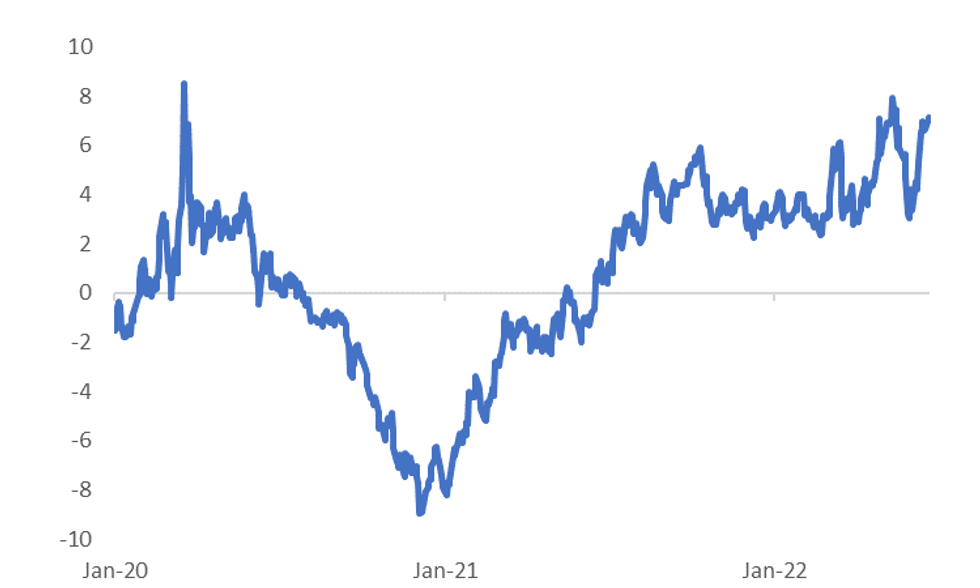

- USD/KRW spot is sitting quite elevated relative to its 200 day MA, see the second chart below. We are +7% above the 200 day MA, which is close to levels we got to earlier this year, but below highs we saw in 2020.

- 1 month implied vol remains elevated at +10%, but we aren't at fresh highs for the year. The picture is more benign in the risk reversal space, with the latest 1 month reading at +1.25, versus earlier YTD highs at +2.0.

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok