Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

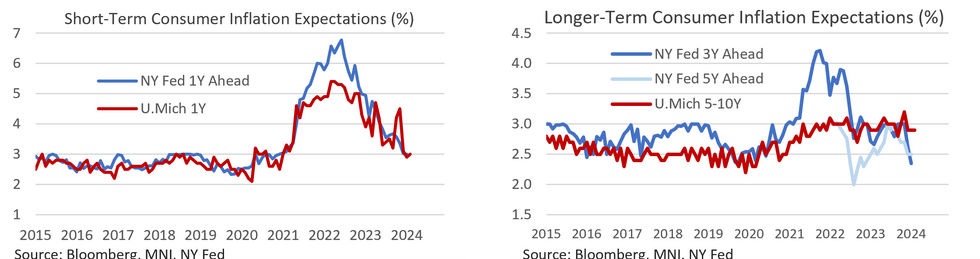

U.Mich prelim 1-year inflation expectations printed a touch higher than consensus at 3.0% (vs 2.9% prior and cons). Longer term 5-10-year expectations were steady at 2.9% Y/Y, 0.1pp above the 2.8% consensus.

- It means that longer-term expectations have remained steady for three consecutive months, with 1-year ahead expectations oscillating between 2.9-3.1% in that time.

- Longer-term expectations have failed to see a similar moderation to the NY Fed's 3Y and 5Y measures, which were 2.35% and 2.50% respectively in January.

- Consumer sentiment and current conditions indices both fell short of consensus (sentiment 79.6 vs 80.0 cons, 79.0 prior; conditions 81.5 vs 82.5 cons, 81.9 prior), while the expectations component overshot at 78.4 (vs 77.0 cons, 77.1 prior).

Some key notes from the report:

- Sentiment improved for a third month as Americans grew more optimistic about the outlook for the economy and inflation.

- While prices remain high, Americans are taking solace in the fact that inflation has largely been cooling. That, combined with a labor market that continues to support resilient consumer spending, is contributing to the recent improvement in sentiment.

- Five-year business expectations at their highest in more than three years.

- While consumers’ perception of their current financial situation improved slightly, their expectations eased.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok