Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL

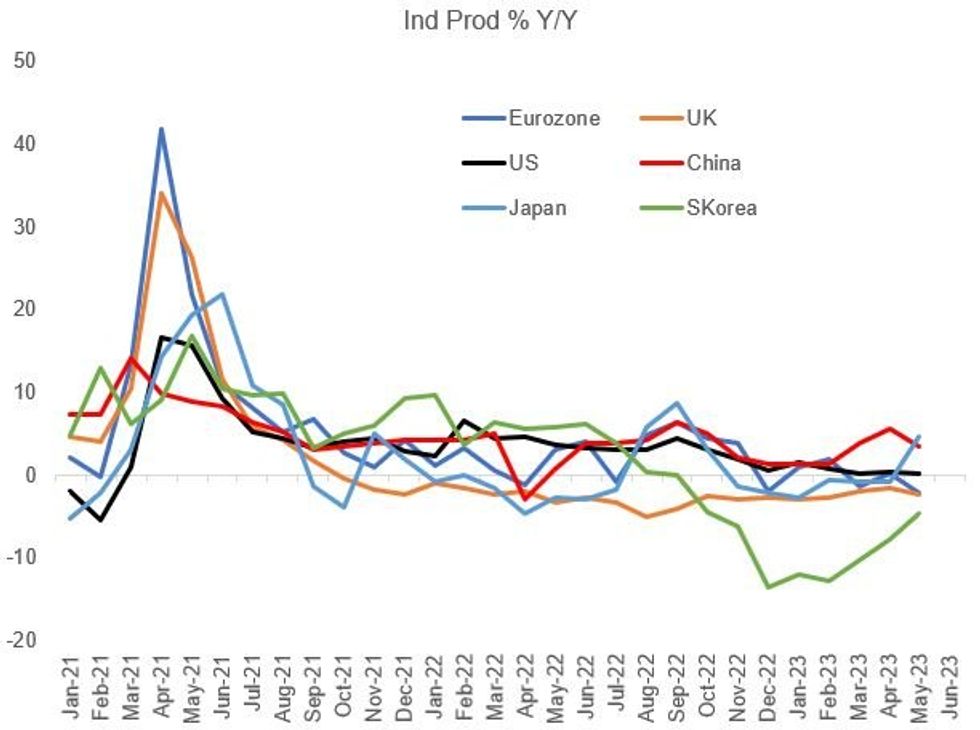

Current weakness in global industrial output is to some extent a developed vs emerging market story.

- Countries representing a combined half of global industrial output is either stagnant or contracting on a Y/Y basis (including the eurozone, UK, US, and South Korea), with Japan posting just its first Y/Y increase since October in May. Meanwhile Korean production remains contractionary though appears to be past the worst.

- On the other hand China, as well as other large producers including India, continue to post IP growth Y/Y.

- Global manufacturing PMIs suggest softness in both spheres: aggregate DM global PMIs remain in contractionary territory (3-year low of 46.3 in June), while EM momentum is weakening (51.1 in June, down 0.3pp from May).

- The most positive news for the global economy comes from the inflation implications. The drop in backlogs comes as supply chains are sharply easing (the NY Fed's Global Supply Chain Pressure Index is at its lowest on record for the series starting in 1997; container costs are dropping sharply, etc). Input and output prices are following suit in the major manufacturing economies, with consumer goods prices likewise softening from pandemic highs.

- So while global industry (and trade alongside it) will likely weaken further in H2, the upside for policymakers is that overcapacity will remain a disinflationary factor.

Source: National Statistical Agencies, MNI

Source: National Statistical Agencies, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok