Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The week ahead will be dominated by the Bank of England’s MPC meeting, the announcement of the policy decision and the publication of the Monetary Policy Report and Minutes. Markets are almost fully priced for a 25bp hike while all 23 sell side reports we have seen expect a 25bp hike (while only Santander and Swiss Life IM look for an on hold decision in the Bloomberg survey out of 37 submissions).

- Our full BOE preview will be published early this week but we note that assuming the MPC votes for a 25bp hike, it will almost certainly not reinvest the gilt holdings due to mature in March. This is largely expected by markets, but there are a couple of sell-side notes that caution that there may be a delay.

- The main focus will be on the medium-term outlook. Will the Bank push back against market rate expectations of 4.75 hikes in 2022? The easiest way to subtly do this would be for the inflation forecast at market rates to be below 2% at the forecast horizon. This seems the most likely scenario to us. Of course the Bank could be more explicit in its comments, but there seems little to gain from doing that when a steeper money market curve at this point in time will help the Bank’s inflation fighting credentials (particularly as the Bank’s previous communications have not particularly steered the market in the desired way). The Bank could alternatively point to two-way risks to the inflation outlook, which would mean that even if the inflation forecast was below 2%, market participants could still think that there was scope for the BOE to carry out tightening at the pace the market currently prices.

- Elsewhere this week, there will of course be no MPC speeches ahead of the decision, while the only notable data will be final PMI data with the manufacturing print due Tuesday and services due Thursday.

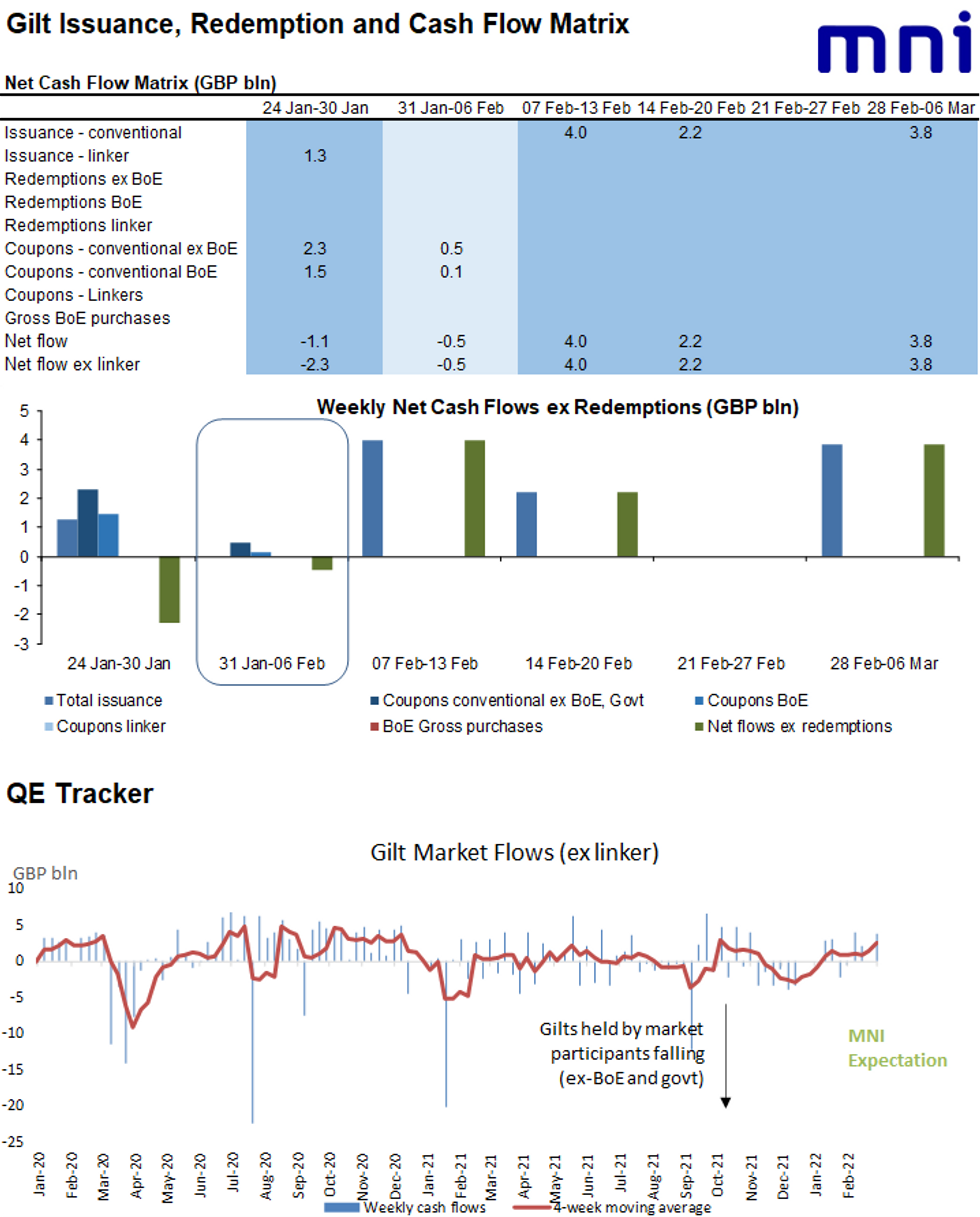

- See the full document for gilt supply previews for the week ahead, QE tracker and BOE purchase analysis, cash flow matrix and issuance calendar.

Full document:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok