Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI ASIA MARKETS ANALYSIS - Congress Battles It Out For Spending Bill

- Congress continues to haggle over the federal spending bill

- Michel Barnier warned that Brexit negotiations are in the final moments

Haggling Over The Federal Spending Bill

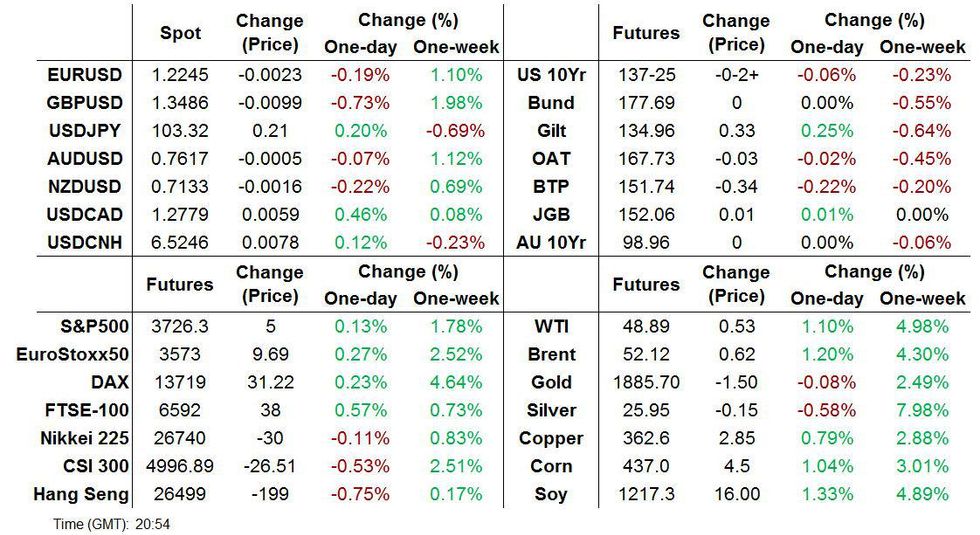

USTs lacked direction through the session and trade marginally below yesterday's closing levels.

- The UST curve has steepened on the back of the longer end trading weaker. Last yields: 2-year 0.121%, 5-year 0.3782%, 10-year 0.9429%, 30-year 1.6925%.

- TYH1 trades at 137-25, towards the bottom end of the day's range (L: 137-23+ / H: 137-30+)

- Congress continues to debate the terms of a federal spending bill with Republican Pat Toomey pushed to include a provision that would limit the Federal Reserve's pandemic-related lending.

- The Fed's Kaplan stated that purchasing bonds for too long could bring financial stability risks. Meanwhile, Richard Clarida suggested that while the economic recovery had someway to go, he does think there will be a double-dip recession.

- Vice President Mike Pence received the Covid vaccine today with President-elect Joe Biden reportedly following suit on Monday.

EGBs-GILTS CASH CLOSE: Bull Flattening As Brexit Talks Hit "Final Hours"

Gilts rallied with bull flattening in the curve as traders took heed of warnings on both sides of the Channel that we were entering the "final hours" of talks to avert a no-deal Brexit.

- Bunds had bear steepened in the morning but this eventually reversed on Brexit's gravity.

- Periphery spreads traded wider.

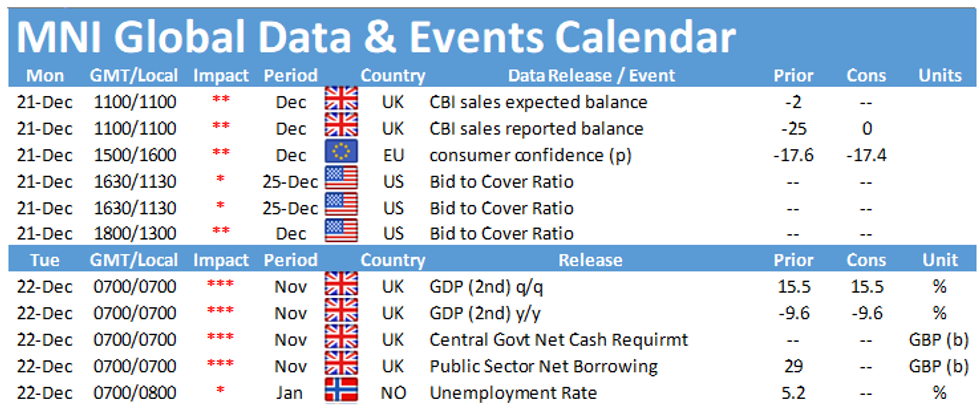

- After such a busy week, it's a relatively thin schedule for the upcoming week ahead of the Christmas holiday - most attention will be on Brexit.

Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is unchanged at -0.725%, 5-Yr is up 0.2bps at -0.744%, 10-Yr is down 0.1bps at -0.571%, and 30-Yr is down 0.5bps at -0.16%.

- UK: The 2-Yr yield is down 3.3bps at -0.084%, 5-Yr is down 3.6bps at -0.042%, 10-Yr is down 3.8bps at 0.249%, and 30-Yr is down 4.1bps at 0.806%.

- Italian BTP spread up 2.6bps at 113.6bps

- Spanish bond spread up 1.7bps at 61.6bps/Portuguese spread up 2.5bps at 60.6bps

OPTIONS SUMMARY:

Friday's options flow included:

US:

3EH1 99.50c, traded 4.5 in 1k

0EM1 99.62p, traded for 1 in 1k

2EM1 99.25/37/75/875c condor, traded 9 in 500

EDM1 99.25/50/75p fly traded half in 500

4EH1 99.12/98.87/98.75p fly 2x3x1, bought for 4.5 in 10k

EDZ2 99.62p EDU3 98.50p 1x2 (ref EDZ2 99.72, 22 del), bought the 2 (U3) for 1in 2k

EUROZONE:

IKF1 151/150.5ps 1x2, bought for 1 in 645

DUG1 112.30/112.20ps, bought for 4 in 2k

DUH1 112.10p, bought for 1.5 in 7.25k

DUH1 112.20/10ps 1x2, bought for 1 in 5k

2RM1 100.50/100.37/100.25p fly 1x3x2, bought for 1.75 in 5k

UK:

0LU1 99.87^, bought for 20.75 in 1k (ref 99.925)

LM1 100.12/100.37cs vs LH1 100.00/100.25cs, bought the June for 0.5 in 13k

LM1 100.00/100.125/100.25 call fly trades 1.5 in 15k all day

LM1 100.12/25/37c fly, bought for 1.25 in 2k

2LM1/LM1 100c calendar, sold the 2yr at flat in 4k

LZ1 99.87/100.00/100.12c fly, bought for 3.5 in 1k

FOREX: Sterling Sloppy Into Friday Close

Having outperformed for much of the first half of the week, GBP spiralled into the Friday close as markets pondered the likelihood of a deal by the end of the weekend. Betting markets had trimmed the implied probability of a deal by year's end by a decent margin into the Friday close, mirroring the pullback in the pound - the poorest performer in G10.

The greenback fared better, as softer equities state-side prompted some risk-off flow. The bounce in the dollar was modest, at best, however as the USD index still trades in close proximity to the multi-year lows posted Thursday at 89.730.

Markets should thin out in the coming week, with the proximity to Christmas holidays sapping activity and volumes.

Another read of US GDP for Q3, consumer confidence data and existing/new home sales are the only real releases. Central bank decisions come from Turkey.

FX OPTIONS: Expiries for Dec21 NY cut 1000ET (Source DTCC)

EUR/USD: $1.1880-90(E1.4bln), $1.2000(E665mln), $1.2050(E556mln), $1.2100-05(E534mln), $1.2150-60(E2.4bln), $1.2195-1.2205(E1.1bln), $1.2225(E677mln), $1.2250(E514mln)

USD/JPY: Y102.90-00($581mln), Y103.15-25($750mln), Y103.90-00($732mln)

GBP/USD: $1.3600-05(Gbp1.0bln)

AUD/NZD: N$1.0650(A$1.1bln-AUD puts)

USD/CAD: C$1.2675($515mln), C$1.2725($555mln), C$1.2750-55($1.1bln)

EQUITIES: Quadruple Witching Rocks Stocks

US equity markets sold off into the Friday close, with the e-mini S&P testing the Wednesday lows at 3680. As was the case at the open, no real headline catalyst or driver for the pull lower in equities, but volatility being propped up by quadruple witching as stock index futures & options and single stock futures & options all expire.

Real estate led losses in US equity space, closely followed by energy, with all ten sectors in the red.

The VIX saw decent support after a few sessions of losses, but gains were thin ahead of the Christmas break.

COMMODITIES: Oil Markets Erase Early Weakness

After a soft start for WTI and Brent crude futures, markets edged higher into the close, with WTI narrowing the gap with the $50/bbl mark, a sizeable psychological level. Early weakness in the energy complex came alongside a slight bounce in the dollar, but this faded at the NYMEX open, with markets still riding high on expected support from US lawmakers, as they near a deal for a COVID stimulus package.

Precious metals edged lower, but losses were muted as markets thinned out pre-holiday. Spot gold remains pinned between two directional parameters - the 100-dma to the upside at 1905.71, and the 50-dma just below at 1871.65.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.