Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Knock-On Rates Sales Started With EGBs

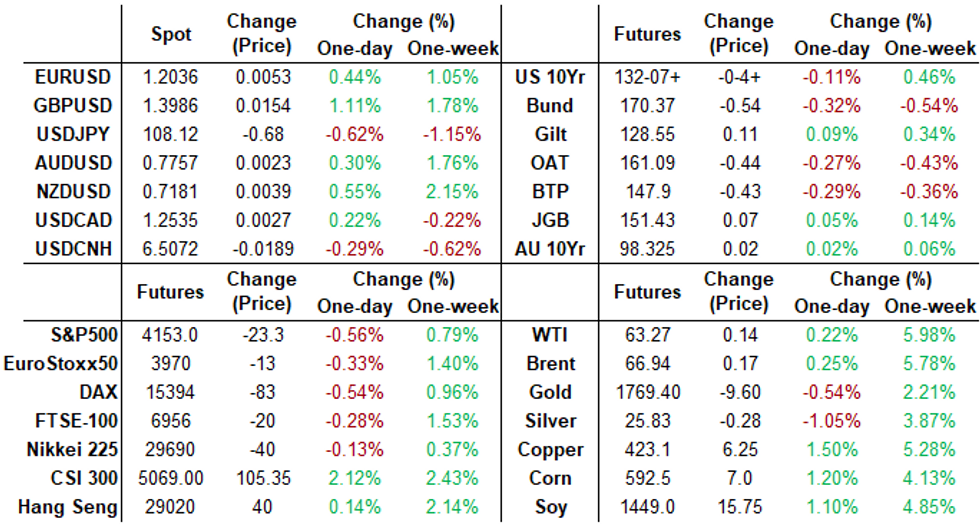

Tsys reversed early strength along with equities Monday, both finishing near session lows. Early duration selling pushed Tsys back to early Thursday levels, knock-on pressure as EGBs hit after dealer recommendations ahead Thursday's policy announcement (Bank of Canada rate annc Wednesday includes Monetary Policy Report).- No significant data Monday through Wednesday after the Fed entered media blackout regarding monetary policy through Apr-29 late Friday, Bill auctions and NY Fed Buy-backs on tap.

- While risk metrics remain (US/Russia tensions tied to Ukraine border troop build not to mention calls for mass protests over Kremlin opposition leader Navalny's health while incarcerated, debate over restarting J&J vaccine), Monday's move deemed more short term tactical selling than headline driven at the moment as 30YY climbs to 2.3002% high, 2.2902% last.

- Deal-tied selling in the mix as Morgan Stanley issued $7.5B debt over 3 tranches, total swappable supply for week estimated over $30B.

- The 2-Yr yield is down 0.2bps at 0.1592%, 5-Yr is down 0.2bps at 0.8292%, 10-Yr is up 1.8bps at 1.5976%, and 30-Yr is up 2.5bps at 2.2902%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settles

- O/N +0.00000 at 0.07275% (-0.00200 total last wk)

- 1 Month -0.00213 to 0.11375% (+0.00463 total last wk)

- 3 Month -0.00225 to 0.18600% (+0.00075 total last wk) (Record Low of 0.17525% on 2/19/21)

- 6 Month -0.00188 to 0.22175% (+0.01325 total last wk)

- 1 Year -0.00563 to 0.28675% (+0.00663 total last wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $66B

- Daily Overnight Bank Funding Rate: 0.06%, volume: $246B

- Secured Overnight Financing Rate (SOFR): 0.01%, $913B

- Broad General Collateral Rate (BGCR): 0.01%, $387B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $358B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, appr $8.801B accepted vs. $28.148B submission

- Next scheduled purchases:

- Tue 4/20 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Wed 4/21 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Thu 4/22 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 4/23 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

US TSYS/OVERNIGHT REPO: Steady-On Specials

Holding steady, Bills unchanged. Current levels:

T-Bills: 1M 0.0051%, 3M 0.0127%, 6M 0.0355%; Tsy General O/N Coll. 0.01%

| Duration | Current | Old Issue |

| 2Y | -0.01% | -0.01% |

| 3Y | 0.00% | -0.07% |

| 5Y | -0.11% | -0.07% |

| 7Y | -0.02% | -0.08% |

| 10Y | -0.09% | -0.09% |

| 30Y | -0.03% | -0.04% |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +20,000 Green Jun 87/90 put spds, 1.0

- -10,000 Green Jun 90/93 put spds, 8.25/legged

- Block, +20,000 Red Dec'22 95/97 put spds, 9.0 vs. 99.865/0.25%

- Block, 10,000 Red Dec'22 95/96/97 2x1x1 put trees, 12.0 vs. 99.585/0.37%

- -10,000 Green Jun 90/92 put spds, 4.5

- +5,000 Blue Jun 83/85/86/87 put condors, 3.25

- +5,000 short Dec 92/95 put spds, 4.5

- +2,500 Sep 99.81/99.87/99.93 call flys, 1.25

- Overnight trade

- 5,750 Blue Jun 83/86 put spds

- Block, 6,750 Blue Jul 98.125 puts, 6.0 vs. 98.54/0.21%

- 3,000 TYM 129.5/134 strangles, 27

- +2,500 TYK 132 calls, 21-22

- +3,500 TYU 133 calls, 56

- Overnight trade

- 6,300 TYK 132 puts, 8

- 3,800 FVM 123 puts, 7

- Block, +20,000 TYM 130/131 put spds, 11, more on screen

- Block, -10,000 TYK 132.5/TYM 133.5 2x1 call calendar, May over 19 net cr

- Block, +5,000 FVM 124/124.5 4x5 call spds, 52.5

EGB/Gilt Summary: Core and semi core stay offered

Core and semi core remains better offered throughout the European session. Bund saw short term play long, bail out.

- This morning piece on Bond strategist recommending shorting Bunds into the ECB (Thursday) has been one of the contributing factor.

- "Barclays short via swaps, Goldman says sell 30-year bunds"

- Also, news that Pfizer, BioNTech will raise the delivery amount to the EU, which will bring the total number of doses this yr to 600mln,have been the contributing factors.

- Peripheral spreads are tighter against the German 10yr.Greec leads at 2.9bps.

- Looking ahead, at 13.15ET, The US President meets with a bipartisan group of Members of Congress to discuss historic investments in the American Jobs Plan

- Bund futures are down -0.54 today at 170.37 with 10y Bund yields up 3.4bp at -0.230% and Schatz yields up 1.2bp at -0.684%

- BTP futures are down -0.45 today at 147.88 with 10y yields up 4.1bp at 0.787% and 2y yields up 1.3bp at -0.347%.

- OAT futures are down -0.48 today at 161.05 with 10y yields up 3.0bp at 0.019% and 2y yields up 1.1bp at -0.653%.

FOREX: USD Hits the Skids, Tests 100-dma Support

- As was the case throughout the European morning, the USD remained weaker across the NY session, keeping the USD index under pressure throughout. The USD index hit the lowest level since early March and tests key 100-dma support at 91.051. A break below here opens another test on the multi-month low printed on Feb 25 at 89.683.

- GBP was the strongest currency Monday, reversing much of the early April weakness. GBP/USD convincingly cleared the 50-dma at 1.3869, opening further strength in the coming sessions. The next resistance is layered ahead of March's 1.4001/05.

- The USD, CAD were the weakest in G10, while GBP, JPY and NOK were the strongest performers in G10.

- Focus Tuesday turns to UK jobs data and a speech from ECB's de Cos. The RBA minutes also cross from their unchanged April meeting.

FX OPTIONS: Expiries for Apr20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1850-65(E1.0bln), $1.1885-00(E760mln), $1.1925-40(E1.7bln-EUR puts), $1.1985-00(E740mln)

- USD/JPY: Y108.65($540mln), Y109.95-00($515mln)

- GBP/USD: $1.3650(Gbp570mln)

- AUD/USD: $0.7770-90(A$978mln)

- USD/CNY: Cny6.40($520mln), Cny6.60($580mln)

PIPELINE: $7.5B Morgan Stanley 3Pt Kicks-Off Week

- Date $MM Issuer (Priced *, Launch #)

- 04/19 $7.5B #Morgan Stanley $2B 3NC2 +57, $3.5B 6NC5 +77, $2B 21NC20 +105

- 04/19 $3B #Republic of Colombia $2B 11Y +175, $1B 20Y +205

- 04/19 $1.5B #Bank of NY Mellon $600M 3Y +20, $400M 3Y FRN SPOFR+26, $500M 7Y +42

- 04/19 $1B Charter Communications Holdings 12NC6 +3a

- Expected over next few days:

- 04/20 $4B EIB 3Y -1a

- 04/20 $500M Japan Int Cooperation Agcy 10Y +32a

- 04/20 $Benchmark New Development Bank (NDB) 5Y +27a

- 04/26 $Benchmark Tokyo Metropolitan, investor calls re: 3-10Y

- 04/?? $Benchmark EQUATE Petrochemical B.V. 7Y

- 04/?? $Benchmark Abu Dhabi National Energy Company PJSC ("TAQA") investor calls re: 7Y, 30Y Formosa bonds

EQUITIES: Stocks Fail to Print New Highs For First Session in Nine

- US equity markets snapped a solid winning streak Monday, closing lower as the e-mini S&P dipped back below 4,150. The index had printed a new all time high for eight consecutive sessions, with Monday's pullback possibly presaged by the RSI inching into overbought territory at the tail-end of last week.

- Tech and consumer discretionary names led losses, with both sectors falling by over 1% apiece in the cash S&P 500. Re-opening names were among the poorest performers, largely on profit-taking, but partially on vaccine concerns, with Penn National and Caesars Entertainment lower by over 4%.

- The pullback in stocks Monday has provided some much-needed support for the VIX, which managed to re-gather above 18 points, close to the April highs.

COMMODITIES: Copper Extends Rally, Gaining 1.75%

- Copper prices advanced 1.75% on Monday after posting their best weekly performance in two months last week. The softer US dollar provided a solid foundation for the red metal to extend higher after a multitude of sell-side forecast upgrades. The focus in Copper futures (HGA) remains the Feb 25th highs at 437 (9,617 in LME) with prices currently trading 423.75.

- Precious metals were unable to continue their recent constructive run amid the weaker dollar. Spot gold (-0.3%) and silver (-0.7%) turned from positive to negative on Monday as US long end yields rose. Recent gains in the yellow metal, however, have confirmed a double bottom reversal and primary support is found at $1757.9, the 50-day EMA.

- Oil Benchmarks approached the NY close in marginally positive territory, rising around 0.4%. Despite spending most of the European session slightly in the red, a softer US dollar provided impetus to post small gains on Monday.

- Following a positive technical weekly close, Brent resistance to watch comes in at $67.55, former trendline support drawn off the Nov 2 low and $67.76, the Mar 18 high.

- Bitcoin continued to trade under pressure after a big retracement over the weekend that saw lows of $51,700 print. Sentiment had been soured late last week following the coinbase IPO and an announcement that Turkey's central bank decided to ban the use of cryptocurrencies for payments from the end of the month.

- Commentators are viewing the pullback as a pause in optimism including former Goldman Sachs hedge-fund manager Raoul Pal who described a feeling of relief as a recent liquidation of leveraged longs "cleans up the market".

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok