Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Tsys Pared Gains Ahead Early Close

Futures pared into the early session close -- late chop on inside range session and two-way positioning, month-end flows. Decent volumes: TYU just over 1M. Sep took lead quarterly position while late hour Jun/Sep rolling continued. Large FVU Block earlier (16,036 FVU 123-25.25) helped start the rebound off lower levels about an hour after the open. Yield curves running mixed w/short durations flatter.

Early mixed data but largely leans positive in terms of the recovery in April - and core prices provide a little more ammo for inflation hawks:

- Personal income beats (though downward revision to March); personal spending in line (with upward revision).

- Meanwhile Wholesale Inventories +0.8% M/M beats expectations (of 0.7%), retail inventories on the weak side (-1.6% vs -1.2% exp). And advance goods trade balance shows a slightly smaller deficit than expected (-85.2B vs -92.0B survey), first time the gap narrowed this year.

- This is the highest level since Nov 1973 and the third consecutive increase. May's increase was led by a sharp rise of New Orders (80.0) to the strongest reading since Dec 1983 and Order Backlogs (80.7) which surged to a 70-year high.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N +0.00413 at 0.06113% (+0.00138/wk)

- 1 Month -0.00625 to 0.08588% (-0.00575/wk)

- 3 Month -0.00325 to 0.13138% (-0.01562/wk) ** (Record Low)

- 6 Month -0.00013 to 0.17100% (-0.00775/wk)

- 1 Year -0.00062 to 0.24813% (-0.01150/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $67B

- Daily Overnight Bank Funding Rate: 0.04% volume: $243B

- Secured Overnight Financing Rate (SOFR): 0.01%, $877B

- Broad General Collateral Rate (BGCR): 0.01%, $376B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $356B

- (rate, volume levels reflect prior session)

- Tsys 0Y-2.25Y, $12.401B accepted vs. $66.840B submission

- Next scheduled purchases:

- Tue 6/01 1100-1120ET: Tsys 2.25Y-4.5Y, appr $8.425B

- Wed 6/02 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Thu 6/03 1100-1120ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 6/04 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

MONTH-END EXTENSIONS: FINAL Barclays/Bbg Extension Estimates for US

FINAL forecast summary compared to avg increase for prior year and same time in 2020. TIPS 0.01Y. Note: MBS extension est surged to 0.22 from 0.13 prelim estimate that Barclays attributes to "yield changes, new production and principal paydowns."

| Indices | Estimate | 1Y Avg Incr | Last Year |

| US Tsys | 0.12 | 0.10 | 0.11 |

| Agencies | 0.04 | 0.08 | 0.01 |

| Credit | 0.11 | 0.10 | 0.08 |

| Govt/Credit | 0.11 | 0.10 | 0.10 |

| MBS | 0.22 | 0.13 | 0.05 |

| Aggregate | 0.13 | 0.11 | 0.09 |

| Long Gov/Cr | 0.11 | 0.11 | 0.10 |

| Iterm Credit | 0.08 | 0.09 | 0.08 |

| Interm Gov | 0.11 | 0.09 | 0.08 |

| Interm Gov/Cr | 0.09 | 0.09 | 0.08 |

| High Yield | 0.11 | 0.12 | 0.04 |

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +30,000 Sep 99.81/99.87 put spds, 1.5 vs. 99.885 - .89

- Overnight trade

- 5,000 Green Jun 99.43 calls, 3.0

- 10,000 Green Dec 88/90 put spds vs. 92/93 call spds

- 3,000 Green Dec 88/90 put spds vs. 91/92 call spds

- 3,000 Blue Jul 82/85 put spds

- 2,800 FVN 123.25/123.75 2x1 put spds

- -12,500 wk1 TY 131 puts, 3

- -4,600 TYN 130.25 puts, 8

- -2,000 TYN 131.5 straddles, 112

- +3,000 TYQ 130/132 put strip 4 over TY2 130.5/TYU 131.5 put strip

- +4,000 TYN 130 puts, 6

- +3,000 wk1 TY 131 puts, 5

- Overnight trade

- 12,000 wk1 TY 130.5/131/131.5 put flys

- 6,000 wk4 TY 131.5 puts, 2

EGBs-GILTS CASH CLOSE: Modest Rally Into The Weekend (And Month End)

EGBs and Gilts strengthened a bit Friday afternoon going into the long (UK and US) weekend, with month-end also a consideration. Periphery spreads came down slightly.

- Very little news flow; morning data suggested continued pickup in confidence in the Eurozone and strong Spanish retail sales, while France saw the highest inflation since 2018, while also unexpectedly posting a downward revision to Q1 GDP into contraction.

- MNI published a sources piece suggesting ECB asset purchases could be around half the current level after the PEPP concludes its active phase in March.

- A few sovereign ratings after hours include Belgium and Ireland.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.6bps at -0.662%, 5-Yr is down 1.4bps at -0.568%, 10-Yr is down 1.1bps at -0.183%, and 30-Yr is down 0.4bps at 0.385%.

- UK: The 2-Yr yield is up 1.1bps at 0.063%, 5-Yr is down 0.7bps at 0.342%, 10-Yr is down 1.5bps at 0.795%, and 30-Yr is down 1.5bps at 1.304%.

- Italian BTP spread down 1.2bps at 109.6bps / Spanish spread down 0.1bps at 65.5bps

OPTIONS/EUROPE SUMMARY: Sterling Put Fly vs Call In Large Size

Friday's options flow included:

- RXN1/RXU1 170/169.5/169/168.5p condor spread, sold July and receive half a tick in 2k

- 2RU1 100.50/100.62cs, bought for 0.75 in 2.5k

- 3RU1/3RN1 100.25 call calendar, bought for 2.5 in 3k

- 0LZ1 99.625/99.375/99.125p fly vs 99.875c, bought the fly for 3 in 15k

- 0LZ1 99.25/99.00ps, bought for 1.5 in 1k

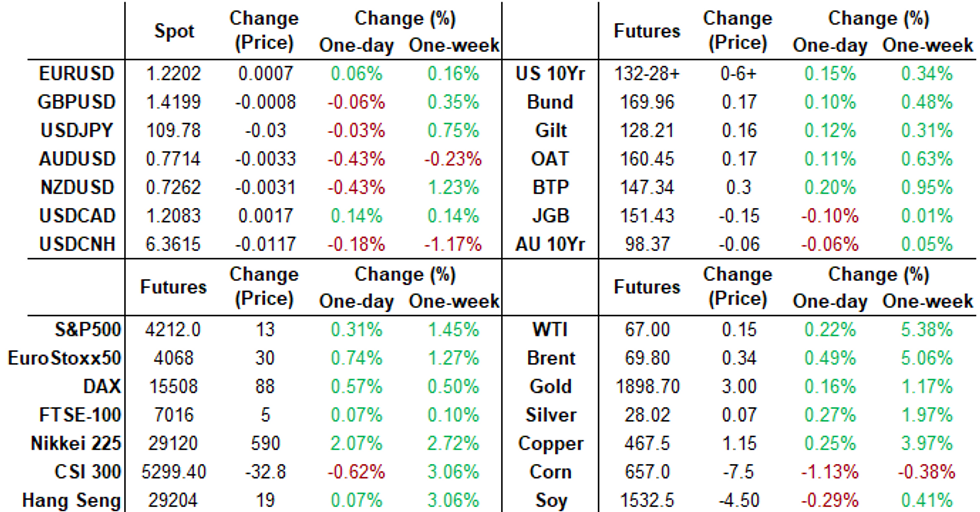

FOREX: Initial USD Strength Fades With Month-End Flow Eyed

- The greenback traded on the front foot for much of the Friday session, with markets watching for front-loaded month-end flow that was speculated to be USD positive. Initial USD gains helped spur further upside in USD/JPY, which spilled above Y110.00 for the first time since early April.

- This price action swiftly reversed following the Friday WMR fix, with the USD drifting to press the USD Index back toward the 90.00 handle.

- EUR/USD recouped the day's losses as markets eyed an MNI report citing sources as saying the ECB's PEPP purchases could half after the 'active' phase concludes in March. EUR/USD remains in the March-May uptrend, but Friday's initial weakness has worked against this pattern.

- The coming week will likely get off to a slow start, with a UK and US market holiday Monday likely keeping activity muted. After that, China's PMI, prelim inflation data from Germany, the RBA rate decision and the May nonfarm payrolls release.

FX OPTIONS: Expiries for May31 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2100-17(E764mln), $1.2145-55(E756mln)

- USD/CAD: C$1.2400($1.1bln-USD puts)

PIPELINE, May High-Grade Issuance Total $159.125B.

No new issuance on Friday's shortened pre-holiday weekend session. Total for the week at $37.9B puts total May high-grade issuance at $159.125B.- Date $MM Issuer (Priced *, Launch #)

- 05/27 $1.5B *Mamoura 10Y +95, 30Y Formosa 3.4%

COMMODITIES: Oil Gives Up Early Gains, Gold Non-Directional

- Energy markets started the session well, with WTI crude futures trading within range of the 2021 highs posted in early March at $67.98. These gains quickly faded, however, as markets looked to book profits ahead of the long weekend.

- Spot gold markets saw some volatility headed into the London close, but prices swiftly stabilised either side of the $1,900/oz handle.

- This leaves the directional parameters for gold unchanged, with support at $1872.8/52.3 - Low May 25 / Low May 19 and resistance just above at the Wednesday high of $1912.8.

EQUITIES: Stocks Edge Higher into Long Weekend, Vol Suppressed

- Continental stock markets traded well into the long weekend for US/UK markets, with the S&P 500 adding another 0.4% to narrow the gap with all time highs to around 20 points. Data proved supportive, continuing to point to a solid H2 rebound as PCE numbers and the MNI Chicago PMI generally fared better-than-expected.

- The US healthcare sector outperformed, with technology and real estate firms also solid. Sizeable gains in the likes of Boston Scientific and Medtronic helped fuel gains. The materials and energy sectors were the foremost laggards as commodity markets consolidated.

- Modest gains for stocks worked further against equity volatility, putting further pressure on the VIX, which looks well within range of post-pandemic lows.

OUTLOOK: Tuesday Look Ahead, ISMs, Fed Speakers Ahead June 5 Blackout

- Jun-01 US markets return from extended holiday weekend

- Jun-01 0945 Markit US Manufacturing PMI May final (61.5, 61.5)

- Jun-01 1000 Construction Spending MoM Apr (0.20%, 0.50%)

- Jun-01 1000 ISM Manufacturing May (60.7, 60.9)

- Jun-01 1000 ISM Prices Paid May (89.6, 89.3)

- Jun-01 1000 ISM New Orders May (64.3, --)

- Jun-01 1000 ISM Employment May (55.1, --)

- Jun-01 1000 Fed VC Quarles, Politico live event

- Jun-01 1030 Dallas Fed Manf. Activity May (37.3, 36.5)

- Jun-01 1120 NY Fed buy-op: Tsys 2.25Y-4.5Y, appr $8.425B

- Jun-01 1130 US Tsy 13W, 26W bill auctions, $57B, $54B resp

- Jun-01 1400 Fed Gov Brainard on mon-pol, NY Econ Club, moderated Q&A

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.