Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Fed' Harker Reiterates Taper View, Time To Talk Timing

Rather muted midweek rally in rates on light volume (TYU 815k) by the bell, 10YY slips to 1.5858% -- low end of range.- No substantive data (May Redbook store sales +13.1%; MBA REFIS -5%), Fed Beige Book underscores inflation pick-up: "Input costs have continued to increase across the board," especially in raw materials, freight, packaging, and petrochemicals, as a result of supply chain disruptions, the Beige Book said. "Strengthening demand, however, allowed some businesses, particularly manufacturers, builders, and transportation companies, to pass through much of the cost increases to their customers."

- Reminder, Fed media blackout starts midnight Fri through June 17, say after the next FOMC policy annc. That said, Philly Fed Pres Harker took the opportunity to reiterate opinion it's time to start debate over taper timing, but "MUST ACT WITH CARE, DON'T WANT TO TRIGGER TAPER TANTRUM" Bbg.

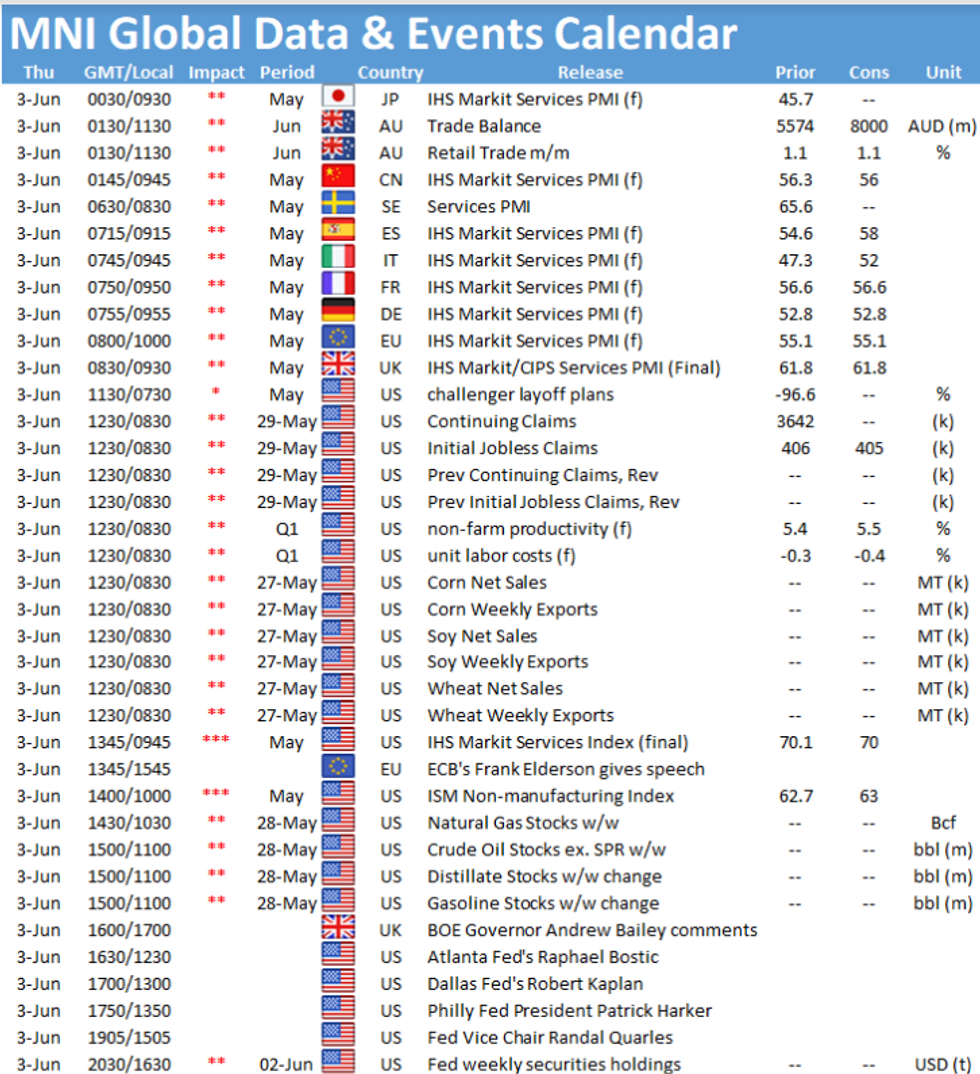

- Focus turns to ADP private employment data and weekly claims Thursday, May NFP Friday (+653k est vs. +266k prior).

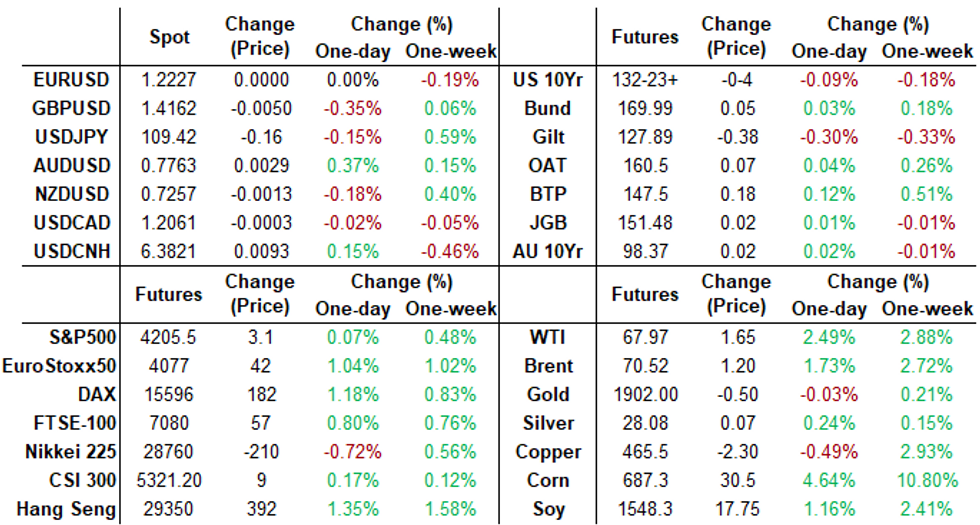

- The 2-Yr yield is down 0.2bps at 0.1446%, 5-Yr is down 0.8bps at 0.7964%, 10-Yr is down 1.5bps at 1.5909%, and 30-Yr is down 0.7bps at 2.2796%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest Settles

- O/N -0.00075 at 0.05500% (-0.00613/wk)

- 1 Month -0.00325 to 0.08550% (-0.00038/wk)

- 3 Month +0.00550 to 0.13400% (+0.00262/wk) ** (Record Low 0.12850% on 06/01/21)

- 6 Month -0.00750 to 0.16738% (-0.00362/wk)

- 1 Year -0.00200 to 0.24488% (-0.00325/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $60B

- Daily Overnight Bank Funding Rate: 0.04% volume: $233B

- Secured Overnight Financing Rate (SOFR): 0.01%, $977B

- Broad General Collateral Rate (BGCR): 0.01%, $404B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $366B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, $1.201B accepted vs. $2.828B submission

- Next scheduled purchases:

- Thu 6/03 1100-1120ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 6/04 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- +20,000 Green Dec 83/86/87/90 put condors, 4.75

- 5,000 Red Sep 90 puts even over Red Mar 83/88 put spds

- Update +10,000 short Sep 95/96/97 put trees, 2.0

- -2,000 Green Jun 99.37/99.43 strangles, 4.75

- +3,000 Green Aug 87/90 put spds, 3.0

- +5,000 Blue Sep 97.87/98.25 put spd w/

- +5,000 Gold Sep 97.50/97.87 put spds, 12.0 total db/package

- Block, +13,000 Green Dec 92/93/95/96 call condors, 3.5 vs. 99.09/0.05%

- +7,500 short Mar 87/92/97 put flys, 12.0

- +4,000 Sep 100 calls, 0.5

- Overnight trade

- 1,500 Blue Sep 80/82 put spds vs. 98.87/99.12 call spds

- -4,000 TYN 132 puts, 37

- +2,000 TYN 130/131 put spds, 10

- +5,000 TYU 130/131/132 put flys, 8

- -1,500 TYQ 132 straddles, 134

- +3,500 FVN 123.5 puts 9.5-10

- +5,000 TYU 129/130/131 put flys, 6

- +4,000 FVU 120 puts, 2.5

- +6,000 TYU 135 calls, 10 vs. 131-29.5/0.12%

- Overnight trade

- -33,000 wk1 TY 131/wk2 TY 130.5 put spds, rolling out and down for 1 net

EGBs-GILTS CASH CLOSE: Positive Session

Wednesday was a constructive if quiet session for the space, with yields falling steadily over the course of the day amid light news / trade flow, and Eurex futures roll proceeding apace.

- Germany had yet another weak auction, this time for Bobl; UK 10-/25Y Gilt auctions decent.

- Data was 2nd tier (German retail sales and Spanish unemp disappointed; UK mortgage approvals higher than expected; Eurozone PPI in line).

- Heavy issuance ahead Thursday, with Spain selling up to E6.25bln in nominal + linkers, and France selling up to E11bln in OAT (incl Green OAT).

- Spain and Italy Services PMIs are Thursday's data highlights (the rest are Finals). BOE's Bailey the only scheduled speaker.

Closing German/UK Yields And 10-Yr Spreads To Germany

- Germany: The 2-Yr yield is down 0.4bps at -0.663%, 5-Yr is down 1.5bps at -0.579%, 10-Yr is down 2bps at -0.198%, and 30-Yr is down 1.9bps at 0.363%.

- UK: The 2-Yr yield is down 1bps at 0.06%, 5-Yr is down 2.2bps at 0.337%, 10-Yr is down 2.7bps at 0.799%, and 30-Yr is down 1.7bps at 1.328%.

- Italian BTP spread down 0.3bps at 107.6bps / Spanish spread up 0.5bps at 65.2bps

OPTIONS/EUROPE SUMMARY: Greens And Blues

Wednesday's options flow included:

- RXN1 168.5/168ps, bought for 2 in ~9k

- 3RZ1 99.75/100.375 combo, sells the put at 1.75 in 5k (v 100.13)

- 2LU1 99.375^ vs 0LU1 99.625^ (v 99.675) bought for 8 in 1.5k (bought the green)

- 2LU1 99.375 put vs 3LU1 99.00 put, bought for 1 in 1.5k (bought the green)

FOREX: USD Gains Short-Lived, DXY Hovers Above Multi-Month Low

- The USD started the Wednesday session particularly well, rallying against all others pushing the USD Index firmly back above the 90.00 handle. The gains were short-lived however, as NY traders responded with waves of USD sales against the rest of DM and GBP in particular.

- GBP/USD's near 80 pip rally off the day's lows was aided by continued confidence from UK PM Johnson that the UK remains on course for a full economic reopening in just over 2 weeks. While UK COVID figures were unable to maintain the streak of 0 daily fatalities, the continued stability in hospital admissions is giving cause for confidence.

- CAD, GBP and NOK were the session's best performers, while JPY, NZD and AUD all traded weaker.

- Markets watch the release of ADP employment change, weekly jobless claims and ISM services data on Thursday. The manufacturing ISM earlier this week showed a sharp slowdown in the employment subcomponent, raising focus for Friday's nonfarm payrolls release, in which markets see net gains of around 650k jobs.

- China's Caixin services and composite PMIs are due as well as speeches from BoE's Bailey, Fed's Bostic, Kaplan, Harker and Quarles.

FX OPTIONS/Expiries for Jun03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2000-15(E1.4bln), $1.2067-75(E587mln), $1.2100-15(E1.3bln-EUR puts), $1.2150-70(E532mln), $1.2300-05(E1.0bln-EUR puts)

- USD/JPY: Y109.00-10($1.7bln-USD puts), Y109.15-25($1.1bln), Y109.45-50($695mln), Y109.98-110.00($1.5bln)

- GBP/USD: $1.3990-00(Gbp653mln), $1.4100(Gbp721mln)

- AUD/USD: $0.7715-25(A$622mln), $0.7835-40(A$812mln)

- USD/CNY: Cny6.42($700mln)

PIPELINE: $5.5B ADB Priced

- Date $MM Issuer (Priced *, Launch #)

- 06/02 $5.5B *ADB $4B 3Y -3, $1.5B 7Y +10

- 06/02 $3B #Indonesia $1.25B 5Y 1.5%, $1B 10Y +2.55%, $ 750M 30Y 3.55% Sukuk

- 06/02 $2.5B #Societe Generale $1.25B each: 6NC5 +100, 11NC10 +130

- 06/02 $1.5B #Petrobras 30Y 5.75%

- 06/02 $Benchmark Citigroup 6NC5 +65a, 6NC5 FRN SOFR

- 06/02 $Benchmark NY Life Ins 5Y +40a, 5Y FRN SOFR

- Expected later in week:

- 06/03 $Benchmark IADB 10Y FRN SOFR

- 06/03 $500M Council of Europe Development Bank (CoE) 3Y -2a

COMMODITIES: Oil Testing Cycle Highs as Vienna Talks Drag On

- Macro drivers remained unchanged for WTI and Brent crude futures, with both benchmarks trading firmly as negotiations with Iran are expected to slide into Thursday. Markets expect little material outcome from the discussions, with Tehran's lack of compliance with nuclear curbs likely hindering any near-term oil supply deal. This keeps first key resistance unchanged for WTI at this week's high of $68.87.

- Gold and silver traded at the whim of the US dollar Wednesday, with initial greenback strength weighing on precious metals prices throughout the European morning. This price action swiftly reversed, with waves of USD sales in US hours helping boost both metals back into positive territory ahead of the close.

EQUITIES: Stocks Just Above Water as Meme-Driven Names Rally

- Headline indices all traded very modestly higher Wednesday, with weakness in bellwether names like Home Depot, Disney and Goldman Sachs countered by outsized rallies in meme-driven names including AMC, Gamestop and Bed Bath & Beyond.

- The net effect on the e-mini S&P was minimal, with the index trading inside the week's range to retain the overarching bullish technical outlook. The week's highs of 4230 remain the first target ahead of all-time highs.

- Energy and real estate names were the strongest sectors Wednesday, with materials and consumer discretionary among the poorest performers.

- Gains were more uniform across Europe, with the French CAC-40 rallying well (higher by 0.5% at the close), although Spain's IBEX-35 drifted 0.1%.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok