Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI ASIA MARKETS ANALYSIS - Markets Await US CPI Report

HIGHLIGHTS:

- USTs and EGBs rallied and curves bull flattened.

- US CPI, as well as earnings and claims data, come into focus on Thursday

- Markets will also be carefully watching the ECB; particularly the wording around PEPP purchases

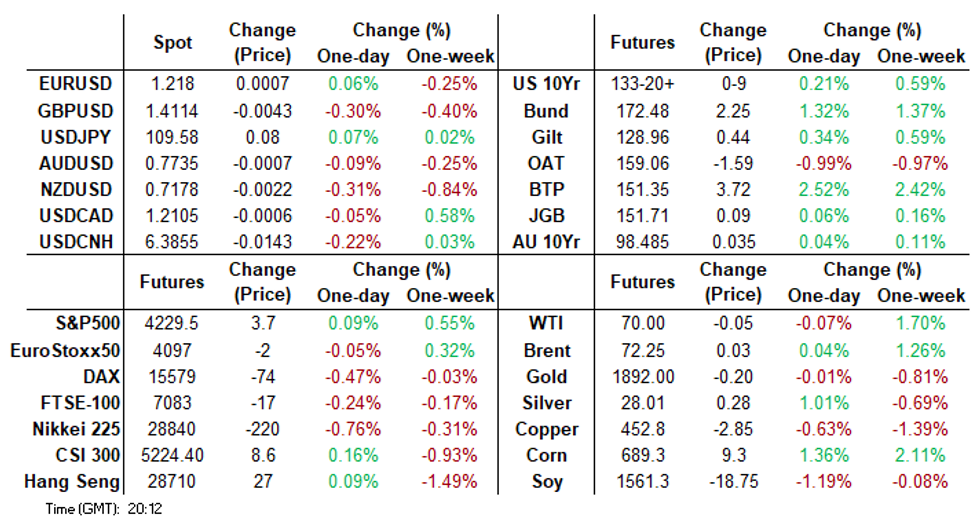

US TSYS SUMMARY: Long-End Outperforms As Market Awaits CPI Report

USTs have rallied through the session and the curve has bull flattened with the market eagerly awaiting tomorrow's inflation report.

- Cash yields are broadly 1-5bp lower on the day with the curve 4-5bp flatter. Last yields: 2-year 0.1508%, 5-year 0.7452%, 10-year 1.4891%, 2.1705%.

- TYU1 trades at 132-24, towards the top end of the day's range (L: 132-11+ / H: 1329).

- USD38bn of the 1.625% May-31 note was sold at auction with median yield of 1.497% and bid-to-cover of 2.58x.

- Looking ahead, focus tomorrow will be on the CPI report, as well as earnings and claims data. Tomorrow's ECB meeting will also be key to watch with markets paying paticular attention to the wording around PEPP purchases over the coming quarter.

EGBs-GILTS CASH CLOSE: Busy, Bullish Pre-ECB Session

A strong and busy afternoon for European govvies ahead of Thursday's ECB decision, with a US Treasury rally helping drive Bund and Gilt yields lower in a bull flattening move.

- Several potential reasons (though no singular one) for the rally, including short-covering / position squaring ahead of ECB. Stop-outs appeared to conclude around 1500BST, after which yields retraced a bit higher.

- Same moves in periphery yields as Tuesday: BTPs outperformed, while Greece (which tapped 10-Yr GGB via syndication, size E2.5bln) underperformed early before recovering.

- Supply elsewhere included Germany (Bund, EUR1.26bn allotted), Portugal (OTs, EUR1.0bn), UK (GBP1.0bln of linkers).

- Nothing on Thursday's docket until the ECB decision.

Closing German/UK Yields And 10-Yr Spreads To Germany

- Germany: The 2-Yr yield is down 0.7bps at -0.676%, 5-Yr is down 1.5bps at -0.615%, 10-Yr is down 2bps at -0.244%, and 30-Yr is down 1.5bps at 0.312%.

- UK: The 2-Yr yield is down 0.9bps at 0.058%, 5-Yr is down 2bps at 0.309%, 10-Yr is down 4bps at 0.73%, and 30-Yr is down 4.3bps at 1.266%.

- Italian BTP spread down 1.2bps at 107.3bps / Greek spread down 1bps at 107.8bps

EUROPE SUMMARY: Downside In Bunds

Wednesday's options flow included:

- RXN1 169.00 puts bought for 3 in ~17k

- RXN1 170.00/169.50/169.00 put ladder bought for 1.5 in 7k

- RXN1 171.50/170.50/169.50 put fly bought for 8 in 4k

- RXU1 171.00/170.5/170.00/169.5p condor, bought for 4.5 in 3k

- 2LU1 99.25/99.125 ps bought for 2 in 4k

FOREX: Late Greenback Squeeze As Markets Await US CPI

- Initial dollar weakness was largely attributed to the move lower in US yields throughout the European session. Moves advanced following 10yr yields closing at their lowest level since March on Tuesday.

- A small extension of dollar supply was evident as we broke Monday lows in the DXY, however, markets quickly ran out of steam and a consistent squeeze ensued during US trade. The Late resurgence leaves dollar indices almost exactly unchanged on the week as markets await significant US inflation data due on Thursday.

- GBPUSD weakness appeared to almost front run the move in the dollar amid souring sentiment with the E.U. Negative comments emerged from EU Commission VP Maros Sefcovic following his meeting with UK Cabinet Office minister Lord Frost earlier today. He said the EU will react "swiftly, firmly and resolutely" if grace period on chilled meat trade from GB to NI is extended unilaterally.

- Sterling retreated from 1.4170 against the dollar and never recovered, currently settled around the lows of the week ~1.4115.

- CAD had been the initial outperformer in G10, in anticipation of the Bank of Canada decision and aided by buoyant oil prices. The statement was broadly alongside expectations, reiterating slack expected to be absorbed sometime in H2 2022, in line with median sell-side forecasts. USDCAD held a very tight range but the path of least resistance caused a consistent squeeze for the pair from 1.2059 back to the highs of the day at 1.2118.

- Focus turns to Thursday's release of US CPI and the ECB's monetary policy decision and press conference.

FX OPTIONS: Expiries for Jun10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2080-1.2100(E1.8bln-EUR puts), $1.2140(E597mln), $1.2175-90(E1.4bln), $1.2200-10(E855mln), $1.2280-00(E1.1bln)

- USD/JPY: Y108.50-55($725mln), Y108.95-10($1.4bln), Y109.60-75($2.7bln), Y110.00($931mln)

- EUR/GBP: Gbp0.8600(E1.2bln-EUR puts)

- EUR/AUD: A$1.5630(E937mln-EUR puts)

Price Signal Summary - Bunds Clear The 50-Day EMA

- In the equity space, S&P E-minis are unchanged and still trading close to the all-time high of 4238.25 May 10 high. This remains the key resistance and the trigger for a resumption of the uptrend. Initial support is at 4165.25, Jun 3 low.

- In the FX space, EURUSD appears vulnerable following last week's price action. The focus is on 1.2105, the 50-day EMA. GBPUSD is consolidating and remains below 1.4248, Jun 1 high. A deeper pullback would expose 1.4006, May 13 low. Note the 50-day EMA intersects at 1.4024 and also represents a key support level. Recent USDJPY weakness has resulted in a probe of support at 109.33, Jun 1 low. A clear break lower would threaten the recent uptrend and expose 108.56, May 25 low.

- On the commodity front, Gold key short-term directional triggers are at; $1916.6, the Jun 1 and bull trigger and $1856.2, the Jun 4 low. Trend conditions in oil remain bullish and price has traded higher today. Recent Brent (Q1) gains have opened $73.00 next, a round number resistance. WTI (N1) similarly cleared resistance to hit new cycle highs, clearing the $70.00 psychological level in the process. The focus is on $70.92, 2.764 projection of Mar 23 - 30 - Apr 5 price swing

- Within FI, Bunds (U1) have topped the 50-day EMA at 172.00 and looks to have made a clear break. This counters the bearish outlook, with support still holding at 170.99. May 31 low. The break higher opens 172.64, 61.8% retracement of the Mar 25 - May 19 sell-off. Gilts (U1) challenged resistance at 127.74/82 this morning - marking the highs between Apr 20 and May 26. A bearish risk remains present. A breach of this resistance zone is required to highlight a base.

EQUITIES: Stocks Flatline as CPI, ECB Awaited

- Equity markets were broadly flat, with the S&P 500 trading inside recent ranges as traders sat on the sidelines ahead of the key pre-FOMC CPI release Thursday, as well as the ECB rate decision. The e-mini S&P stalled ahead of both the weekly high at 4236.75 as well as the alltime highs printed May 10th at 4238.25.

- Gains in the US health care and utilities sectors were countered by weakness in industrials and financials, which slipped as the US sovereign curve flattened further.

- Inside trade for the S&P 500 kept the VIX under pressure, which traded within range of yesterday's low of 15.15 points - a new post-pandemic low.

COMMODITIES: Oil Rolls Off Highs as Iran Progress Seen

- Both WTI and Brent crude futures struck fresh cycle highs Wednesday, with WTI touching $70.62, while Brent hit $72.87 ahead of the close. Markets were inclined to take profits from there, with headlines suggesting progress had been made between Iran and US diplomats.

- While oil matters were yet to be fully resolved, markets now look ahead to the next round of negotiations in Vienna due to kick off next week. On the supply front, Iran have already flagged that full supply could be put back online within a month should sanctions be removed.

- Gold and silver were mixed, with gold flagging ahead of $1900/oz resistance, while silver managed to benefit despite a rebound in the greenback ahead of the close.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok