Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Improved Risk Appetite Holding

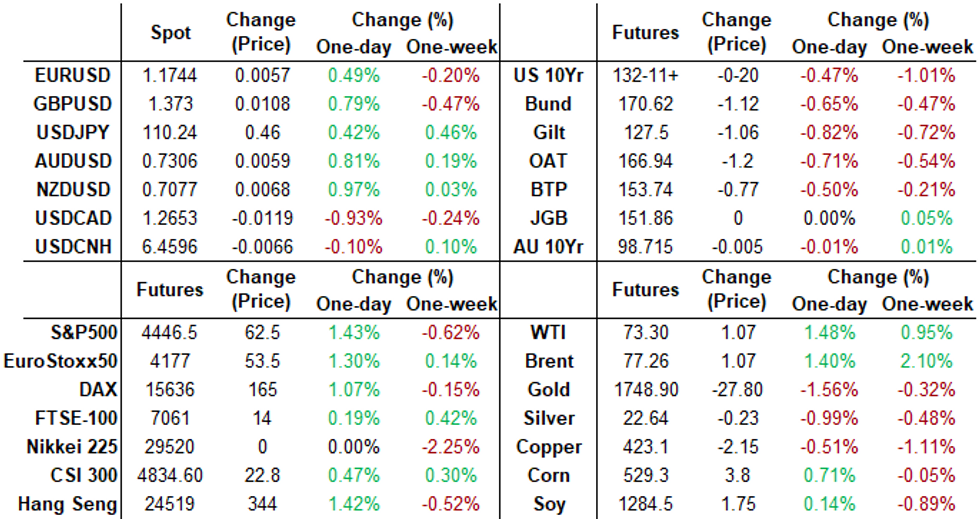

Risk appetite improved Thursday, rates holding narrow range near lows since late morning while equities surged -- Dow surged over 600.0 at one point while eminis traded +60.0 at 4444.0 after the FI close, US$ index DXY -.418 at 93.044.

- Brief risk-off move ahead the NY open as China's Evergrande continued to roil markets. Early risk-on tone scaled back slightly after headlines that Chinese officials told "local governments to prepare for downfall" (DJ) of real-estate developer.

- Quickly discounted, risk-on tone gained momentum into midday as participants ruminated over timing and speed of tapering as precursor to lift-off. Main takeaway from Fed Chair Powell's presser: reinforcement that taper very likely annc in Nov barring a poor Sep jobs report (mark your calendar for Fri October 8 ). Re: Sep payrolls report, Powell actually said he's looking for a "reasonably good one" and later a "decent" one, and NOT a "knockout, great, super strong employment report".

- Little react to weekly claims, +16K to 351K; continuing claims +0.131M to 2.845M

- Bonds more than reversed post FOMC gains, yield curves bear steepening -- while 5s30s held below 100bp, front end curves surged: 2s10s +8.5 at 114.7 -- near last Fri's high print -- that married up with strength in financials / banks today.

- Decent overall volumes as yields climbed, two-way deal-tied hedging on $10B corp supply, some option hedging ahead Fri's Oct Tsy expiration.

- The 2-Yr yield is up 2bps at 0.2567%, 5-Yr is up 7.8bps at 0.9286%, 10-Yr is up 10.6bps at 1.4061%, and 30-Yr is up 11.3bps at 1.9207%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00062 at 0.07188% (+0.00113/wk)

- 1 Month +0.00275 to 0.08600% (+0.00250/wk)

- 3 Month +0.00300 to 0.13225% (+0.00838/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00050 to 0.15500% (+0.00275/wk)

- 1 Year +0.00375 to 0.22900% (+0.00463/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $71B

- Daily Overnight Bank Funding Rate: 0.07% volume: $265B

- Secured Overnight Financing Rate (SOFR): 0.05%, $879B

- Broad General Collateral Rate (BGCR): 0.05%, $375B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $349B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5, $1.401B accepted vs. $4.334B submission

- Next scheduled purchase

- Fri 9/24 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

FED Reverse Repo Operation, Fifth Consecutive Record High

NY Fed reverse repo usage surged to new record high of 1,352.483B from 77 counter-parties vs. Wednesday's record $1,283.281B.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- -4,000 short Mar 99.37 straddles, 25.5

- +10,000 Dec 99.68 puts, 0.75

- -5,000 Green Mar 98.12/98.25 put spds, 1.5

- +5,000 Green Oct 98.75/98.88 2x1 put spds, 1.5

- -7,500 Blue Oct 98.50 puts, 10.5-11.0

- 3,000 Jun 99.81/99.87 1x2 call spds

- -2,500 Red Mar 98.50/99.12 2x1 put spds, 2.5

- +20,000 Nov 99.75 puts, 0.75

- +5,000 Dec 99.62/99.75 put spds, 0.5

- +25,000 Blue Dec 97.87/98.12/98.37 put flys, 4.5

- -3,000 Blue Dec 98.37 puts, 12.5

- +5,000 Red Dec 99.25/99.37/99.62 put trees, 2.25

- +2,500 Red Dec 99.00/99.25/99.50 put flys, 3.5

- +10,000 Green Mar 98.25/98.50/98.75 put flys, 4.0

- -20,000 short Mar 98.75/99.00/99.50/99.75 call condors, 17.5

- Update +45,500 TYX 132.5 puts 28-40

- 2,000 TYV 132/132.25/132.5/132.75 put condors, 8

- 3,000 TYV 132.75 puts, 6

- 2,500 USV 165 calls, 5

- -20,000 wk2 TY 131 puts, 6-3

- -3,000 TYX 131/132 2x1 put spds, 4

- -4,000 TYZ 129 puts, 7

- +2,500 FVZ 122 puts, 10.5

- +2,000 FVX 123 straddles, 45 vs. 123-04/0.10%

FOREX: Risk On Provides Boost To Cross/JPY, Greenback Under Pressure

- Buoyant market sentiment provided a tailwind for risk-tied currencies on Thursday, with the Japanese Yen seeing steady selling pressure throughout the session.

- This led to significant moves in yen crosses, with particular strength seen in AUDJPY, CADJPY and NZDJPY, all rising just shy of 1.5%.

- Despite the higher US yields, the recovery in equities worked against the US dollar, with broad dollar indices retreating around 0.5%.

- Some hawkish repricing in UK money markets following the Bank of England also supported GBPUSD, rising 1% from the early lows hovering 20 pips below the week's highs and the 20-day EMA circa 1.3760.

- Today's gains leave a key support at 1.3602 unchallenged, Aug 20 low. Furthermore, it also means triangle support at 1.3633 remains intact despite being probed yesterday and today.

- In similar fashion, the Norwegian krone rallied over 1% against the greenback with an upbeat central bank meeting as well as oil prices providing a beneficial backdrop for NOK.

- In the EM space, a surprise rate cut worked against the Turkish Lira. USDTRY (+1.3%) matched record levels just above 8.80, last seen in June earlier this year.

- German IFO data headlines the EU session on Friday before Fed Chair Powell, Gov Bowman and VC Clarida are due to deliver remarks at an online event.

FOREX: Expiries for Sep24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1650(E664mln), $1.1675(E663mln), $1.1700(E1.3bln), $1.1765-85(E879mln)

- AUD/USD: $0.7275(A$685mln)

- USD/CAD: C$1.2585-00($1.2bln), C$1.2620-40($1.0bln), C$1.2650-55($1.2bln), C$1.2680-00($1.3bln), C$1.2800($1.6bln)

PIPELINE: $8B Debt Issuance to Price, $3B Egypt 3Pt Leads

- Date $MM Issuer (Priced *, Launch #)

- 09/23 $3B #Arab Rep of Egypt $1.125B 6Y 5.8%, $1.125B 12Y 7.3%, $750M 30Y 8.75%

- 09/23 $1.8B #American Tower $600M 5Y +63, $700M 10Y +95, $500M 30Y +115

- 09/23 $1.5B #Nordea Bank 5Y +60

- 09/23 $1B #Bank of Ireland 6NC5 +110

- 09/23 $700M *CCB HK 5Y +65a

- 09/23 $/E Benchmark Altice France investor calls

- 09/23 $Benchmark Credit Bank of Moscow NC5.5 AT1 investor calls

EQUITIES: S&P500 Closes Gap With Friday Close

- Wall Street traded higher for a second session, with the S&P 500 closing the gap with the Friday close to trade back above the 50-dma. A solid contribution from the energy sector boosts the headline index, thanks to a late rally in oil prices. Financials also rallied well for a second session, as a steeper front-end of the US yield curve supported banks.

- For the e-mini S&P, Friday's highs at 4482.50 mark the next upside target ahead of 4489.14 - the 76.4% Fib for the downtick from the alltime high printed on Sep 3.

- Continued progress for stock markets continues to work against the recent spike in the VIX, which ebbed back below 20 points on Thursday.

- Stocks across Europe finished positively, with most indices finishing with gains of 1% or so. The UK's FTSE-100 was the underperformer, finishing just below water thanks to weakness in Prudential, GlaxoSmithKline and Unilever shares.

COMMODITIES: WTI Narrows in on Cycle High

- Oil markets resumed their incline headed into the Thursday close, with the USD's post-Fed pullback working in favour of energy products. This put the November WTI crude future north on track for the highest close of the year and within range of the 2021 high at $73.58/bbl.

- Markets continue to position for tight winter supply, with Goldman Sachs joining the likes of Bank of America forecasting a double digit USD rise in oil prices should temperatures dip below their winter average this year.

- This keeps the bullish sentiment intact following last week's gains. Tuesday's price pattern was a bullish doji candle, reinforcing current bull trend conditions. Last week's gains resulted in a break of the bear channel top drawn off the Jul 6 high. The move higher strengthens a bullish theme and signals scope for further short-term gains. A rally north of $73.58 opens $74.08 and $75.00.

- Gold prices traded under pressure throughout US hours, with the spot price dropping briefly back below $1750/bbl as equity markets globally extended their recovery from the lows printed earlier in the week.

- A resumption of weakness would open the key support at $1690.6 further out, Aug 9 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok