Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Strong Private Employ Gain A Precursor to Fri's NFP?

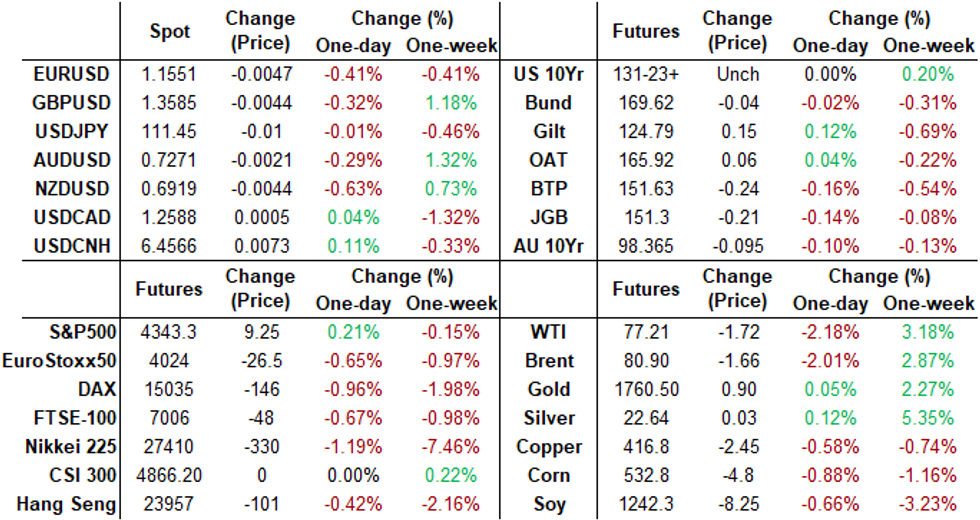

Rates trade mixed after the bell, bonds outperforming for much of the session as yield curves scaled back steepening off multi-yr lows over last couple wks (5s30s -2.8 to 109.1). In-turn, equities reversed modest losses to mildly higher after Tsys closed, a surge in global gas prices traded lower, Gold posted modest gains.- Better than expected Sep ADP job gain of +568k vs. +430k est (Aug down revision by 34k to +340k) spurred additional selling in intermediates to long end. Of note is +466K in services jobs highlighted by +226K figure for Leisure and Hospitality (highest since June), suggests Jul-Aug lull is reversing and perhaps further evidence that the Delta Covid variant is not having a particularly significant lasting impact on hiring.

- However, small business employment growth of just +63K suggests very little traction there, with all of the heavy lifting done by large businesses: +390K was the highest since June 2020.

- No market reaction to late headlines re: extending debt limit. Sen Rep Leader McConnell: WILL ALLOW EMERGENCY DEBT LIMIT EXTENSION INTO DEC .. with the caveat "BIPARTISAN TALKS POSSIBLE IF DEMOCRATS STOP SPENDING" Bbg.

- Futures levels see-sawed higher amid fast$, prop acct buying after initial program selling. Decent pick-up in US$ debt issuance from supra-sovereigns including United Arab Emirates pushed high-grade supply over $12B (>$38B since Mon).

- The 2-Yr yield is up 1bps at 0.2935%, 5-Yr is up 0.8bps at 0.9813%, 10-Yr is down 0.5bps at 1.5206%, and 30-Yr is down 2.1bps at 2.0746%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00287 at 0.07275% (-0.00162/wk)

- 1 Month +0.00138 to 0.08713% (+0.01188/wk)

- 3 Month +0.00000 to 0.12400% (-0.00913/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.00100 to 0.15613% (-0.00088/wk)

- 1 Year +0.00425 to 0.24113% (+0.00625/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $74B

- Daily Overnight Bank Funding Rate: 0.07% volume: $263B

- Secured Overnight Financing Rate (SOFR): 0.05%, $916B

- Broad General Collateral Rate (BGCR): 0.05%, $369B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $344B

- (rate, volume levels reflect prior session)

- Tsy 10Y-22.5Y, $1.401B accepted vs. $3.838B submission

- Next scheduled purchases

- Thu 10/07 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Fri 10/08 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

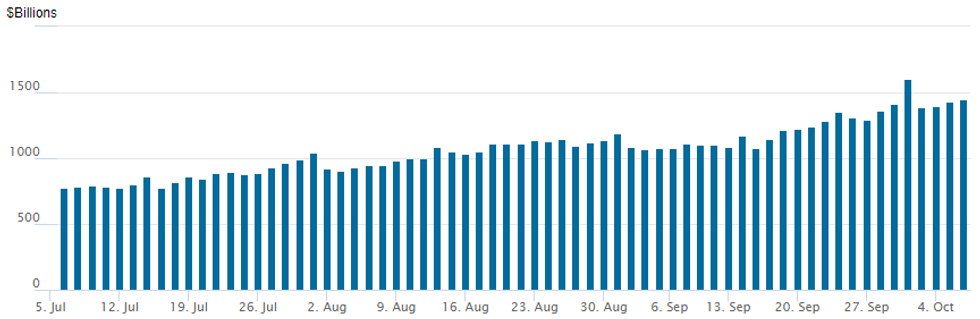

FED Reverse Repo Operation, Climb Continues

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $1,451.175B from 83 counterparties vs. Tuesday's $1.431.180B. Compares to Thursday, September 30 record high of $1,604.881B.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- 20,000 Green Oct/Green Nov 98.56/98.75 put spd spds

- 4,000 short Nov/short Dec 99.50 straddle spds

- +2,000 short Nov 99.37/99.50 put spds, 3.0 vs. 99.51/0.30%

- +2,500 Red Dec 99.12/99.37 put spds, 5.0

- +2,000 Green Dec 98.50 puts 0.5 over Gold Dec 97.62 puts

- +5,000 short Oct 99.37 puts, 0.5 vs. 99.475/0.10%

- Overnight trade

- 5,000 short Dec 99.25 puts, 1.0

- 5,000 Blue Oct 98.25 puts, 1.0

- 8,000 Green Dec 98.50/98.68 put spds

- 4,000 Green Dec 98.81/99.00 put spds

- +5,000 Green Nov 99.00/99.12/99.25 call flys, 1.5 vs. 98.865/0.05%

- Block, +10,000 Green Oct 99.12/Green Dec 99.25 call strip, 2.0 vs. 98.88/0.10%

- +1,500 TYZ 131 puts, 36

- Overnight trade

- 4,000 TYX 131.5/134.5 strangles

- 10,000 TYZ 129.5 puts, 16

- 4,000 USX 156 puts, 25

- Block, +11,250 TYX 130 puts, 6

- Block, +5,000 USX 157.5 puts, 49

EGBs-GILTS CASH CLOSE: Energy Drives Reversal

Wednesday saw a proverbial "story of two sessions" play out in European FI, with sharp weakness at the open giving way to a significant rally by the afternoon.

- The price action largely centred around energy market dynamics: natgas prices soared to records early, weighing on equities and bonds, but soothing comments on supply by Russia's Putin led gas prices lower and equities/bonds to bounce.

- Just as they underperformed on the energy price spike, Gilts outperformed on the reversal.

- Periphery spreads widened, with Greece underperforming.

- Supply came from the UK (GBP2.5bln Gilt) Germany (E4bln Bobl), Slovakia (E1bln via syndication).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.2bps at -0.694%, 5-Yr is up 0.4bps at -0.549%, 10-Yr is up 0.6bps at -0.182%, and 30-Yr is up 0.9bps at 0.301%.

- UK: The 2-Yr yield is up 1.7bps at 0.47%, 5-Yr is up 0.8bps at 0.691%, 10-Yr is down 1.3bps at 1.071%, and 30-Yr is down 2.1bps at 1.428%.

- Italian BTP spread up 2.6bps at 107.4bps / Spanish up 0.5bps at 65.2bps

EGB Options: No Shortage Of Rates Structures

Wednesday's Europe rates / bond options flow included:

- RXZ1 171/169.5ps, sold at 87 in 7k (likely closing)

- 0RH2 + 0RM2 100.375/100.50 1x2 call spread strip bought for 7.5 in 7k

- 0LZ1 99.12/99.00/98.87p ladder sold at 1 in 20k

- 3LX1 98.75/98.625 ps bought for 3.5 in 10k (ref 98.835, 16 del)

- SFIZ2 99.60/70/80/90 call condor, bought for 1.5 in 2k

- SFIH2 99.60/99.70/99.75 call ladder vs 57 d06 bought for 1.5 on 4k

FOREX: Haven Currencies Gain as Stocks Test Recent Lows

- Haven FX outperformed Wednesday, with JPY, USD and CHF among the session's best performers. Currencies took the lead from equities as US futures indices rolled off the late Tuesday high to narrow in on the recent lows.

- NOK reversed early strength as energy prices performed an about-face. Strength across WTI and Brent crude futures initially propped up the currency, but a larger build than expected in crude stockpiles saw the NOK reverse course to be the weakest among G10 FX.

- AUD/NZD extended the rally off the mid-September low on the RBNZ rate decision, with NZD holding the session's underperformance throughout as the RBNZ failed to commit to an extended tightening cycle. AUD/NZD strengthened to touch 1.0518 - new multi-month highs - before fading.

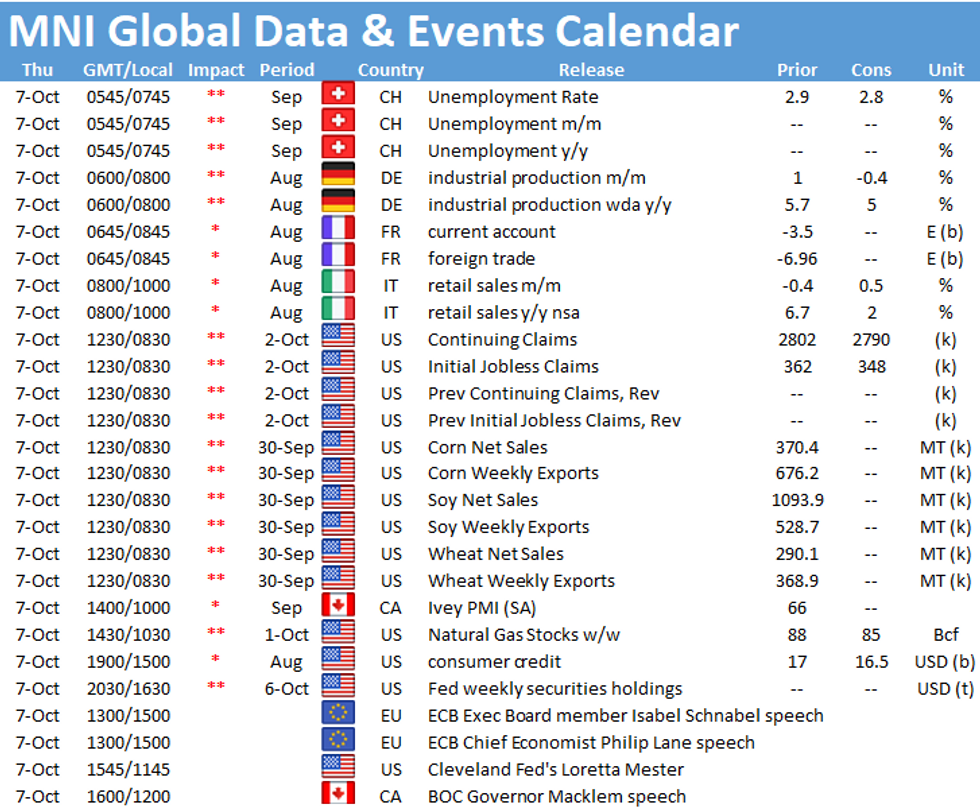

- Focus turns to German industrial production and weekly US jobless claims, while a number of ECB speakers are also due. There are seven different ECB speeches due, as well as appearances from Fed's Mester and PBoC governor Yi Gang.

FOREX: Expiries for Oct07 NY cut 1000ET (Source DTCC)

- USD/JPY: Y111.00($835mln), Y111.50($707mln)

PIPELINE: $3B Macquarie 4Pt Launched

Pushes total issuance for Wednesday to $12.25B

- Date $MM Issuer (Priced *, Launch #)

- 10/06 $4B #United Arab Emirates $1B 10Y +70, $1B 20Y +105, $2B 40Y Formosa 3.25%

- 10/06 $3B #Macquarie Group $850M 4NC3 +67, $400M 4NC3 FRN/SOFR +71, $500M 6.5NC5.5 +95, $1.25B 11.25NC10.25 +135

- 10/06 $3B #Pepsico 10Y +47, 20Y +62, 30Y +72 (for comparison, Pepsico issued $6.5B on March 17 '21: $1.5B 5Y +160, $500M 7Y +180, $1.5B 10Y +180, $750M 20Y +190, $1.5B 30Y +200, $750M 40Y +230)

- 10/06 $1B *Ontario WNG 10Y +31

- 10/06 $750B #CCDJ (Quebec) 5Y +17

- 10/06 $500M *Korea 10Y +25

EQUITIES: Stocks Re-Target Recent Lows

- Equity markets across Wall Street head into the Wednesday close in negative territory, with relatively uniform losses of between 0.5-0.8%. While no new multi-month lows were printed, headline indices remain in close proximity to the October lows, a break below which could re-trigger bearish pressure.

- Energy and materials names led the S&P 500 into the red, with a reversal in oil & gas prices largely responsible. Nonetheless all sectors traded lower, with healthcare and financials also putting in a poor show.

- The immediate bear trigger for the e-mini S&P is 4260.00, the Oct 1 low. A break would pave the way for weakness toward 4214.50, the Jul 19 low. 4095.00 would mark 10% from the recent highs, and official correction.

- European headline indices underperformed their US counterparts, with Spain's IBEX-35 dropping 1.7% while the EuroStoxx50 dropped 1.3%.

COMMODITIES: European NatGas Plummets as Market Bets on Putin's Support

- In early European hours, prices for UK and EU-bound Natural Gas futures shot higher, with benchmark contracts adding to recent gains, extending the YTD gains to as much as 500%.

- This price action partially reversed course following comments from Russian President Putin, who criticized the European approach to commodities and stated his country's willingness to help stabilize prices. This quickly saw UK- and EU-bound prices fall, with UK day-ahead gas turning a 25% gain into a 15% loss.

- Oil markets were similarly eventful, with early strength being erased into the close following a far larger-than-expected build in crude inventories (+2.4mln bbls vs. Exp. +796k) compounded by a similarly sizeable build in gasoline stockpiles (+3.3mln bbls vs. Exp. -69k). WTI crude futures $79.78/bbl before fading back below $78/bbl.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok