Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

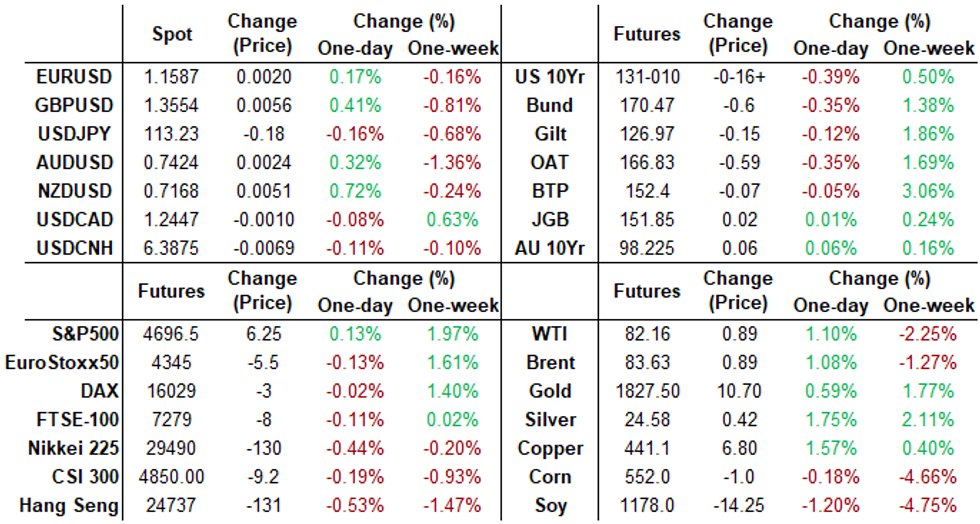

US TSYS: 30Y Inflation-Linked Yld -0.508% Record Low

Tsys revisit second half lows in after hours trade, moderate overall volumes (TYZ1 just over 1.0M futures), yield curves mixed/longer spds flatter (5s30s -6.72 at 76.04), 30Y Inflation-linked yld -0.508% record low.- No data Monday but multiple Fed speakers echoing hawkish tones: Clarida Says Fed On Track To Raise Rates By End Of 2022; Harker Prepared To Hike Before Taper Ends If Prices Surge; BULLARD: THIS IS `ONE OF THE HOTTEST LABOR MARKETS' WE'VE SEEN ... has TWO RATE HIKES PENCILLED IN FOR 2022, Bbg.

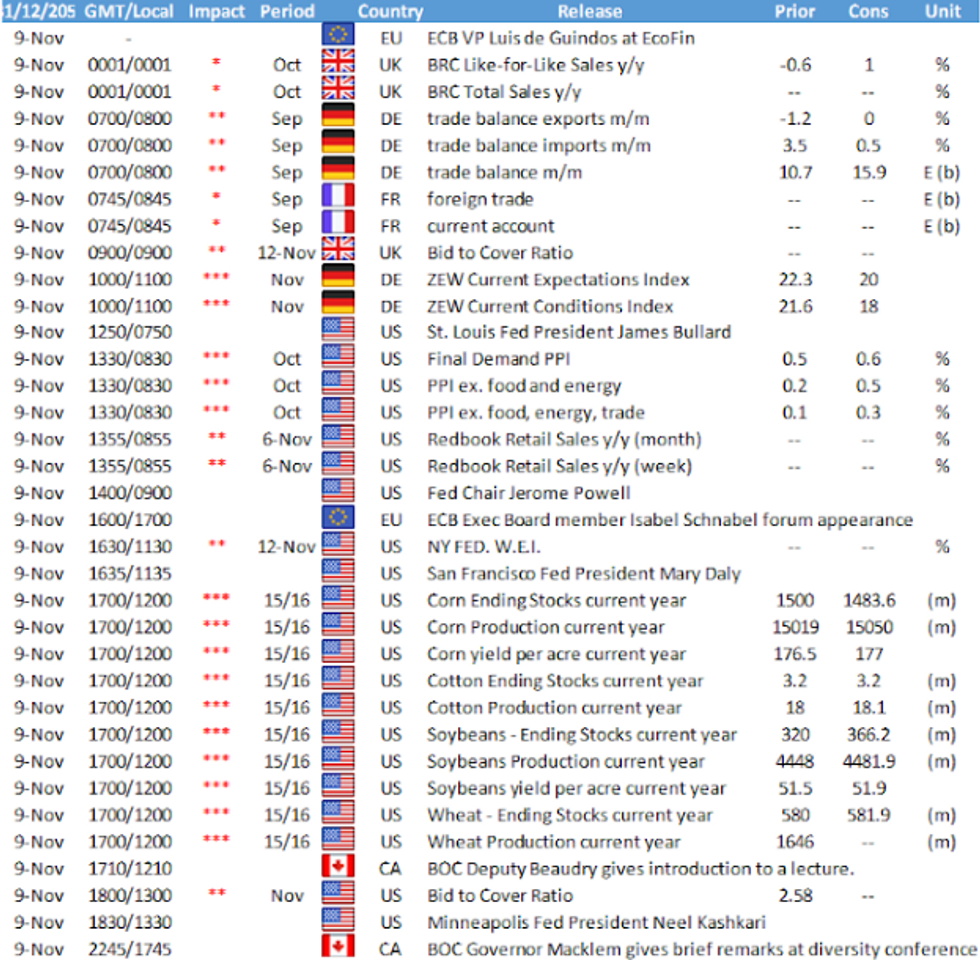

- For a little variety: Fed Regulation Chief Quarles announced his resign at year-end. Chairman Powell again Tuesday; data focus on PPI Final Demand MoM (0.5%, 0.6% est); YoY (8.6%, 8.6% est)

- Early long end bid evaporated quickly, futures see-sawed to session lows early second half. Tsy futures held near lows after $56B 3Y note sale (91282CDH1) tailed (0.750% high yield vs. 0.642% WI; 2.33x bid-to-cover vs. 2.44x 5-auction avg) but bounced off lows following Block buy 7.5k FVZ 122-04.

- Sources also report bank portfolio buying 10s-30s after real$ sold 30s earlier, foreign real$ bought 3s earlier. Deal-tied selling earlier starting to unwind as swappable corporate issuance launched, $5.5B Westpac 5Pt lions share of Mon's $12.55B total corporate issuance. Large 12k Eurodollar Green-pack Block buys.

- The 2-Yr yield is up 4.6bps at 0.4466%, 5-Yr is up 6.1bps at 1.1169%, 10-Yr is up 4.2bps at 1.4932%, and 30-Yr is down 0.1bps at 1.8857%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.00763 at 0.06500% (+0.00050 total last wk)

- 1 Month +0.00250 to 0.09113% (+0.00213 total last wk)

- 3 Month +0.00288 to 0.14563% (+0.01050 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00188 to 0.21900% (+0.01988 total last wk)

- 1 Year -0.00462 to 0.35288% (-0.00363 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $79B

- Daily Overnight Bank Funding Rate: 0.07% volume: $283B

- Secured Overnight Financing Rate (SOFR): 0.05%, $875B

- Broad General Collateral Rate (BGCR): 0.05%, $354B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $331B

- (rate, volume levels reflect prior session)

- Tsy 22.5Y-30Y, $1.999B accepted vs. $3.768B submission

- Next scheduled purchases

- Tue 11/09 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Wed 11/10 1010-1030ET: Tsy 7Y-10Y, appr $3.225B

- Thu 11/11 Veterans Day holiday, no purchase operation

- Fri 11/12 1500ET: Update NY Fed Operational Purchase Schedule

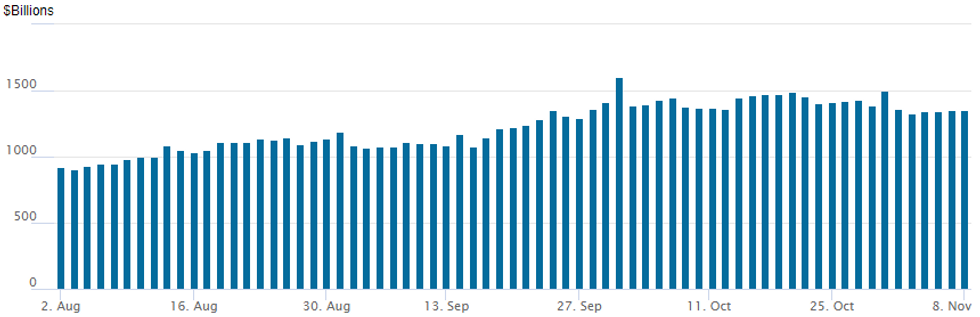

FED Reverse Repo Operation

NY Fed Reserve/MNI

NY Fed reverse repo usage creeps higher: $1,354.382B from 75 counterparties vs. $1,354.059B on Friday. Record high remains at $1,604.881B from Thursday, September 30.

EURODOLLAR/TREASURY OPTIONS SUMMARY

Eurodollar Options:- Block, 10,000 Green Jan 97.87/98.25 put spds, 5.0 at 1213:02ET

- +4,000 Green Nov 98.37/98.50 2x1 put spds

- +5,000 short Jan 98.25 puts, 1.5

- +5,000 Green Dec 98.50/Blue Dec 98.25/98.50 put spd spd, steepener 4.5 (3EZ1 put spd bought over)

- +10,000 Jun 98.43/98.56/98.68 put flys, 1.75

- Overnight trade

- 13,800 Sep 97.00 puts, 1.0

- 3,250 Blue Dec 98.50 calls

- 25,000 Dec 99.75/99.81 put spds

- 15,000 Green Dec 99.12/99.37 call spds

- 10,000 Green Dec 99.12 calls, 1.0

- Block, +8,600 short Dec 99.18/99.93 put spds 2.0 over Blue Dec 98.00/98.25 put spds

- 5,000 short Dec 99.12 puts, 6.0

- 15,000 FVZ 121/121.5 2x1 put spds, 1 net/1-leg over

- 5,000 TYZ 133.25 calls 5

- -3,500 TYZ 133 calls, 6

- 10,500 FVF 120/121.25 put spds

- +2,000 TYZ 130.5/131.25 2x1 put spds, 2.0

- Overnight trade

- 13,000 TYZ 130.5/131.25 put spds 1 over TYZ 132.5 calls

- 12,000 TYZ 129.5 puts, 3-4

- 3,500 TYZ 133.5 calls, 4-5

EGBs-GILTS CASH CLOSE: Short-End Rally Pauses For Breath

UK and German short-end yields ticked higher after a strong rally late last week following the BoE meeting. Long end yields fell, though, with 30Ys outperforming in a flattening curve move.

- Periphery spreads modestly tightened (Italy and Greece 10Y in ~2bp vs Bunds).

- Definitely the least active session in a few days in terms of both volumes and tradeable events, amid a quiet day for data and supply.

- Nothing new from ECB's Lane who reiterated his dovish stance.

- The schedule picks up a bit Tuesday with German ZEW data and German / Dutch bond sales, as well as appearances by BOE's Broadbent and ECB's Lagarde, among others.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at -0.722%, 5-Yr is up 2.2bps at -0.557%, 10-Yr is up 3.5bps at -0.245%, and 30-Yr is up 4.8bps at 0.115%.

- UK: The 2-Yr yield is up 0.9bps at 0.417%, 5-Yr is up 0.3bps at 0.568%, 10-Yr is up 1bps at 0.855%, and 30-Yr is down 1.3bps at 1.003%.

- Italian BTP spread down 1.9bps at 113.8bps / Greek down 2.3bps at 134.6bps

Taking Advantage Of Rally To Position For Downside

Monday's Europe bond / rate options flow included:

- RXZ1 168.5p, bought for 10 in 1k

- RXZ1 169.5/171.5cs 1x2, trades 74.5 in 4k

- RXZ1 169/168ps, bought for 9 in 3kRXZ1 168.5p, bought for 10 in 1k

- 2RZ1 100/99.75ps vs 100.25c, bought the ps for half in 1.5k

- 2RH2 99.75/99.62ps vs 100.37c, bought the ps for -0.5 (receive), in 2k

- ERZ2 100.25/100.15ps, sold at 2.5 in 10k3RZ1 99.75p, bought for 2 in 1.25k

- 0LZ1 98.25p, bought for half in 4.1k

FOREX: Greenback Edges Lower As Kiwi Outperforms

- The greenback extended on some late Friday weakness, with the dollar index retreating roughly 0.3% to start the week.

- Gains for major currencies were broad based against the US dollar with just CHF and SEK also showing weakness.

- NZDUSD led the G10 charge, rising 0.7% and back above 0.7150. Notable resistance comes in at 0.7219, multiple highs throughout October. GBPUSD also traded with a positive tone after rising back above 1.3500 and ranking second on the G10 Monday leaderboard.

- USDJPY continued to edge lower towards the 113 handle, a level the pair has not closed beneath since October 8, also representing the October 12 low. Despite primary trend conditions remaining bullish, a break of this support zone would signal scope for a deeper pullback and open 112.08, Sep 30 high.

- The Euro also strengthened and worth noting EURCHF extending a bounce from the 1.0534 Friday lows to just shy of the 1.06 handle as New York sat down on Monday. Recent commentary had been focusing on the 1.0505 level that provided crucial support following the onset of the pandemic in early 2020, garnering increased attention among market participants.

- Dollar weakness filtered through to some emerging market FX with notable strength in both the South African Rand and the Chilean Peso, both rising 1%.

- German ZEW sentiment data will be the focus of the European data calendar on Tuesday before US PPI headlines the US docket.

FOREX: Expiries for Nov09 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1550(E1.3bln)

- USD/JPY: Y113.70($2.0bln)

- EUR/GBP: Gbp0.8500(E593mln)

- USD/CAD: C$1.2400-05($700mln), C$1.2460($1.1bln)

EQUITIES: E-mini S&P Oscillates Below Last Week's Highs

- Stock markets were mixed Monday, sitting just below the alltime highs posted at the end of last week. The e-mini S&P oscillated below Friday's 4711.75 print, which remains the first upside target ahead of projection levels layered above at 4717.00 as well as 4746.68.

- Oil & gas names - particularly services firms - are trading solidly, helping the sector top the S&P 500 in early Monday trade. Energy firms are firmer as WTI and Brent crude shrug off early pressure to add over 0.5% apiece.

- Moves comes despite the US Energy Secretary Granholm telling US press that an announcement could come this week from Biden himself in an effort to confront soaring energy costs.

- Granholm added that the President is looking into other tools, having made informal approaches to OPEC in recent months to up supply. The lack of major response in markets may reflect an expectation that US action will fall short in a market that remains focused on the OPEC+ production outlook.

- Utilities were at the other end of the table, with consumer staples and discretionary firms also trading poorly.

COMMODITIES: WTI Shrugs Off Warning of Possible POTUS Action

- The US Energy Secretary Granholm spoke to MSNBC early Monday, flagging a possible announcement from the President later this week on still stubbornly high energy prices. The comments stopped short on specifics, but markets assume the White House could still lean on a supply boost from the Strategic Petroleum Reserve, with informal approaches to OPEC+ seemingly falling on deaf ears.

- The comments did little to dent prices, with WTI crude futures holding north of the $81/bbl level throughout, as Asian demand for ever-increasing OSPs for Saudi crude signal solid demand in an already tight market.

- Key resistance and the bull trigger is $85.41, Oct 25 high. A break through here would re-engage the recent bullish theme, while the 50-day EMA at $77.33 is seen as a key S/T support and a clear break would suggest scope for a deeper pullback.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok