Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

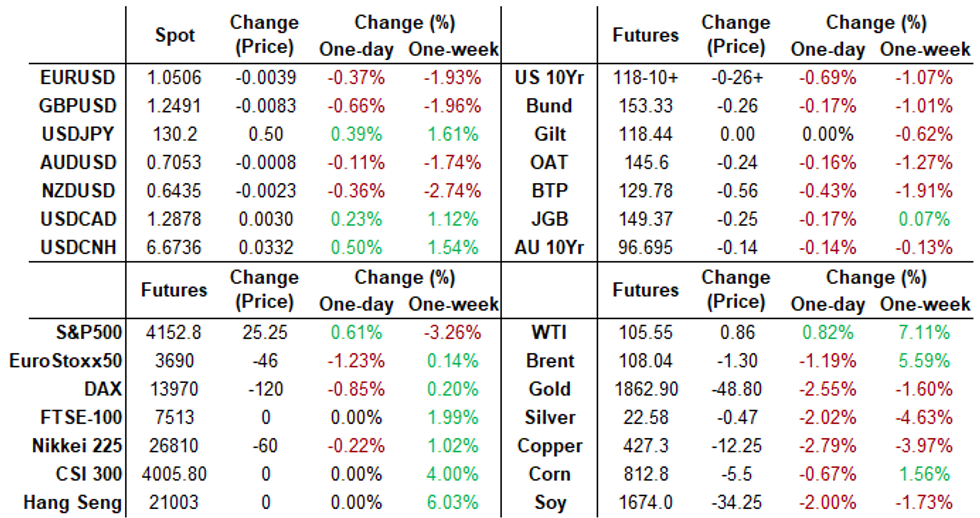

US TSYS: 10YY Breached 3% Briefly

London and Asia extended spring holiday weekend, exacerbated already thin markets Monday with accts sidelined ahead Wed's FOMC policy annc. TYM2 neared key resistance of 118-02.5 in the second half.

- Notably, 10YY breached of 3.0% to 3.0003% briefly - the highest level since Dec 2018), rebounded after the bell (TYM2 at 118-12.5) as did equities: SPX emini Jun'22 futures at 4145.0 +17.5 vs. 4056.25 second half low.

- May’s FOMC decision will be the most hawkish in recent memory, with a 50bp hike and the launch of balance sheet reduction. However, already aggressive market hike pricing limits the potential hawkish impact. Focus will be on the FOMC’s openness to 75bp hikes and/or moving above “neutral”, and any hint of asset sales.

- That said, lead quarterly Eurodollar futures finished near session highs (ESM2 at 98.105 +0.030, EDU2 +0.010 at 97.25).

- Tuesday data kicks off at 1000ET: Factory Orders (-0.5%, 1.2%); ex-trans (0.4%, --); Durable Goods Orders (0.8%, 0.8%); ex-trans (1.1%, 1.1%); Cap Goods Orders Nondef Ex Air (1.0%, 1.0%); ship (0.2%, --) and JOLTS Job Openings (11.266M, 11.200M).

SHORT TERM RATES

US DOLLAR LIBOR: No settlements Monday with London out for May Day holiday

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $76B

- Daily Overnight Bank Funding Rate: 0.32% volume: $244B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.28%, $915B

- Broad General Collateral Rate (BGCR): 0.30%, $354B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $333B

- (rate, volume levels reflect prior session)

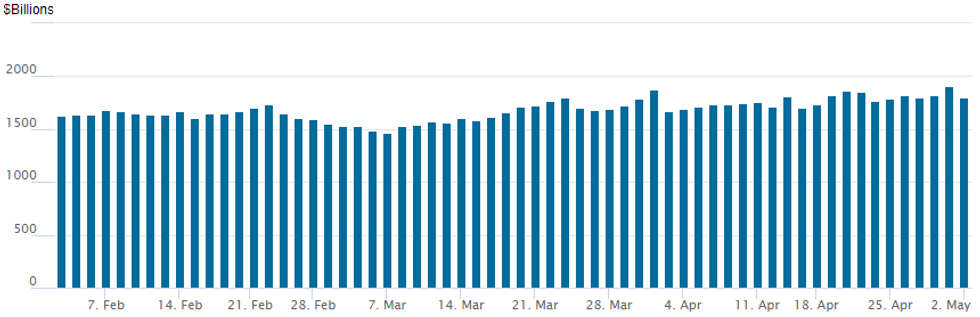

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs recedes to 1,796.302B w/ 84 counterparties from prior session's new all-time high of 1,906.802B (prior all-time high of $1,904.582B on Friday, December 31).

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

FI options trade turned mixed Monday, two-way positioning in calls and puts, outright and on spread as underlying FI futures traded broadly weaker (except for bid in Jun'22 and Sep'22 Eurodollar futures).- London and Asia extended spring holiday weekend exacerbated thin markets and sidelined accts ahead Wed's FOMC policy annc had TYM2 nearing key resistance of 118-02+ 0.618% Fibonacci projection of the Mar 7 - 28 - 31 price swing. Yield curves at/near session highs as bonds lead sell-off, 10YY breach of 3.0% to 3.0003% highest level since Dec 2018, albeit amid modest overall volumes (TYM2 <875k)..

- +10,000 short Jun 97.50 calls 1.5 vs. 96.42/0.05%

- +5,000 Red Sep'23 96.25/97.37 put over risk reversals, 31.0 vs. 96.45/0.70%

- -2,500 short Sep 96.00/96.25/96.75 put flys 2.75 over short Sep 95.75/96.00/96.50 put fly

- 3,800 Jul 97.00/97.25 put spds

- Overnight trade

- Blocks, 10,000 short Aug 97.37/97.62 call spds, 3.0 vs. 96.49/0.05%

- +28,300 FVN 116.5 calls, 4.5

- -28,000 FVM 116.5 calls, 1

- +6,000 FVM 115 calls, 8.5

- 6,500 FVM 111.5/112 put spds, 7

- -5,000 USM 132/134/136/138 put condors

- -10,000 FVM 110.5/111 2x1 put spds, 1.5-1

- 3,000 TYM 119.25/119.5 put spds

- Overnight trade

- 3,000 TYM 119/122 call spds

- 2,700 TYM 121 calls, 16

- 13,000 TYM 118 puts, 37-38

- Block, 10,000 FVM 112 puts, 27

- 3,700 FVM 111.75 puts, 20.5

FOREX: Greenback Maintains Upward Trajectory, Erases Friday’s Pullback

- The US dollar trades firmly in the green on Monday, with the USD Index (+0.76%) recouping the entirety of Friday’s pullback and narrowing the gap with most recent cycle highs, situated at 103.928.

- Price action during the second half of Monday trade has generally been a slow grind, with a UK market holiday keeping many traders on the sidelines ahead of key risk events later this week - most notably Wednesday’s FOMC meeting as well as Friday's Nonfarm Payrolls release.

- Strength in the greenback has been broad based, however, Scandinavian FX are the notable underperformers, ranking at the bottom of the G10 pile, closely followed by weakness in CHF, CNH and GBP.

- GBPUSD (-0.72%) has slipped back below the 1.2500 mark with last Friday’s gains considered technically corrective following last week’s overall acceleration of the downtrend. 1.2412, the Apr 28 low remains the bear trigger before 1.2375, a Fibonacci projection of the Mar 23 - Apr 13 - 14 price swing.

- AUDUSD relatively outperforms, retreating just 0.3%, however the pair remains in close proximity to the recent lows amid the downward momentum for global equity benchmarks. Last week’s price action resulted in a breach of 0.7095, the Feb 24 low, and reinforces bearish conditions. Nearest support is seen at 0.6968, the Jan 28 low ahead of the RBA announcement due overnight. The much firmer than expected Q122 CPI print in Australia may have tilted the scales towards a cash rate hike at tomorrow’s May meeting.

- Aside from the RBA, both Japan and China are out for local holidays which may impact local liquidity during the APAC session. Eurozone unemployment figures along with US JOLTS data headline the Tuesday calendar.

FX: Expiries for May03 NY cut 1000ET (Source DTCC)

- USD/JPY: Y127.00($860mln), Y129.75($550mln)

Late Equity Roundup: Bouncing Off Lows

Stocks reversed early gains, extended session lows into the FI close -- SPX eminis are bouncing back last few minutes: currently ESM2 down 9 points (-0.22%) at 4119.25 - after breach of major support earlier.

- ESM2 fell to 4056.25 low in late FI trade, breaching key support of 4094.25 (Feb 24 low and a major support).

- Earnings cycle resumes with several after the close: Expedia (EXPE), Williams Cos (WMB), Devon Energy (DVN), Diamondback Energy (FANG).

- SPX leading/lagging sectors: Communication Services (+1.36%), Energy (+0.65%) and Information Technology (+0.26) lead by semiconductor shares.

- Laggers: Real Estate shares (-3.58%) followed by Consumer Staples (-2.07%) and Utilities (-1.60%).

- Meanwhile, Dow Industrials currently trades -71.6 points (-0.22%) at 32911.64, Nasdaq -76.4 points (0.6%) at 12412.22.

- Dow Industrials Leaders/Laggers: Honeywell (+1.59 at 195.10), Microsoft (+1.84 at 195.35) and Chevron (+1.53 at 158.20). United health sank late (-13.30at 495.25) followed by American Express (-5.94 ayt 168.77 and Visa (-4.49 at 208.64).

- RES 4: 4631.00 High Mar 29 and key resistance

- RES 3: 4588.75 High Apr 5

- RES 2: 4509.00 High Apr 21 and a key short-term resistance

- RES 1: 4303.50/4355.50 High Apr 26/28 / Low Apr 18

- PRICE: 4119.0 @ 1525ET May 2

- SUP 1: 4110.75 Intraday low

- SUP 2: 4094.25 Low Feb 24 and a bear trigger

- SUP 3: 4063.24 1.618 proj of the Mar 29 - Apr 18 - 21 price swing

- SUP 4: 4029.25 High May 13 2021

S&P E-Minis remain in a downtrend. Friday’s sell-off has reinforced bearish conditions and confirmed a resumption of the bear cycle. Attention is on 4094.25, the Feb 24 low and a major support. A breach of this level would further strengthen bearish conditions. Moving average studies are in a bear mode once again, highlighting current bearish sentiment. Firm short-term resistance is at 4303.5.

COMMODITIES

- WTI Crude Oil (front-month) up $0.48 (0.46%) at $105.17

- Gold is down $33.85 (-1.78%) at $1863.00

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/05/2022 | 0430/1430 | *** |  | AU | RBA Rate Decision |

| 03/05/2022 | 0755/0955 | ** |  | DE | unemployment |

| 03/05/2022 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Manufacturing PMI (Final) |

| 03/05/2022 | 0900/1100 | ** |  | EU | PPI |

| 03/05/2022 | 0900/1100 | ** | | EU | unemployment |

| 03/05/2022 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 03/05/2022 | - | | EU | ECB Lagarde & Panetta in Eurogroup Meeting | |

| 03/05/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 03/05/2022 | 1300/1500 | | EU | ECB Lagarde High School Q&A | |

| 03/05/2022 | 1400/1000 | ** | | US | factory new orders |

| 03/05/2022 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 03/05/2022 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 03/05/2022 | 1515/1615 | | UK | BOE Mutton Panellist at Bankers Association | |

| 03/05/2022 | 1630/1230 |  | CA | BOC Sr Deputy Rogers speaks on operational independence |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.