Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

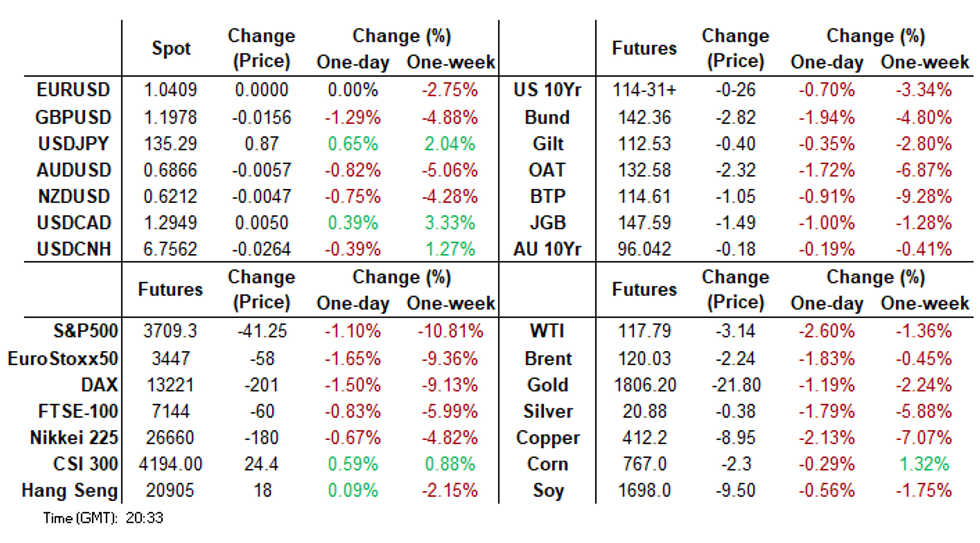

- US TSYS Sell-Off Extends As Speculation Builds Around 75bp Fed Hike

- GBP Continues Downward Trajectory, Breaching Psychological 1.20 Mark

- Japanese Yen Extends Drop, Weakest In 24 Years

US TSYS SUMMARY: Sell-Off Continues As Speculation Builds Around 75bp Hike

Following some temporary respite earlier in the day, USTs continued selling-off in the later part of the session as expectations build ahead of tomorrow's FOMC meeting, with markets now largely pricing in a 75bp hike.

- UST yields are now up 8-14bp and are now trading at the highs of the day. the belly of the curve is underperforming while TYU2 is plumbing new lows.

- Real yields have pushed higher with the 5-year reaching the highest level since March 2020.

- The dollar continues to make broad gains with the DXY trading up to 105.53 - the highest level since 2002.

- Headline PPI data was broadly in line with expectations and continue to point towards persistent elevated inflationary pressure.

MNI Fed Preview: June 2022 - UPDATE: Justifying 75

We've published an update of our June FOMC preview (emailed to subscribers and available on our website), including tentative predictions for the updated dot plot / Statement, and updates by sell-side analyst expectations:

- With 90+% probability of a 75bp hike now priced into rate futures, the Fed is likely to deliver just that on Wednesday.

- The Statement will incorporate stronger hawkish language in order to justify the surprise acceleration in the hike pace.

- June’s Dot Plot will become much more hawkish vs March’s and vs what was expected prior to a 75bp hike becoming consensus. But the outlined rate path will probably fall short of current market pricing.

NatWest: 75bp Hikes In June and July

NatWest now sees 75bp hikes in both June and July (with Powell set to signal Wednesday that the latter is "on the table").

- "In our view, given the Fed’s blackout period, Powell decided a WSJ article was the only option ahead of tomorrow’s meeting to prepare markets that 75 is now on the table. We agree that Powell would prefer not to be “forced” by markets, but, at this point, we feel Powell and the rest of the FOMC would rather try to attempt to get inflation better under control than worry about criticism that he is being led by markets."

- NatWest is eyeing hikes at the remaining meetings this year beyond July, but is waiting to see the updated Dot Plot and the projection of the terminal rate.

Scotia: If Fed Hikes 75, Their One-Meeting Fwd Guidance Becomes Useless

Scotiabank now sees a 75bp Fed hike this week, though excoriates the FOMC's communication on the matter.

- "The case for accelerating the size of hikes outweighs the case against", though "if they do indeed hike by 75bps tomorrow, then even their one-meeting ahead forward guidance will become utterly useless."

- On the Fed's new optics problem now that it's signaled 75bp via the press: "It would no longer surprise markets given that it’s fully priced and so the fear of sparking market turmoil has already come and gone. By corollary, not going 75bps would risk awkward optics around easing financial conditions with inflation ripping and after a jobs beat unless they really hit forward guidance much harder than is already priced which is tough to see given we have 3½ – 3¾% priced for year-end now. In other words, if they pass on 75 and don’t go to 3¾% by year-end then headlines on dovish market reactions relative to what’s priced would be super awkward optics for them".

BOE: Summary of Analyst Views

- All 21 analyst previews that we have read look for a 25bp hike this week and a further 25bp hike in August.

- Views on the vote breakdown are more nuanced.

- Out of 14 analysts, half expect to see a 6-3 vote with three members voting for a 50bp hike.

- 3 analysts look for a 2-6-1 vote split (50/25/unch).

- The remaining analysts are split between 3-5-1, 2-5-2, 0-9-0 and 0-7-2/0-8-1.

- No one expects any QT announcement this week, and analysts largely steered clear of reiterating their views in this month’s set of previews.

- Only 2 analysts still see cuts in their base case: Citi (50bp in 2023), Deutsche Bank (starting Q4-23).

- Bank Rate at end 2022 (out of 21 analysts): The majority of analysts expect Bank Rate to end 2022 in a 1.50%-2.00% range.

- 2 analysts look for 2.25% (10%)

- 5 analysts for 2.00% (24%)

- 6 analysts for 1.75% (29%)

- 8 analysts look for 1.50% (38%)

- JP Morgan look for 2.75% (5%)

- 3 analysts expect 2.50% (16%)

- 4 analysts expect 2.25% (21%)

- 5 analysts expect 2.00% (26%)

- 2 analysts expect 1.75% (11%)

- 3 analysts expect 1.50% (16%)

- Citi expect 1.00% (5%)

EGB/Gilt - German 10yr Yield edges towards 1.70%

- Another busy session for EGBs and Bund, with Yields still trading near their peaks.

- More notable price action has been in the longer end, with the German 30yr breaching 1.8%, highest since 2014.

- German 10yr Yield is still edging towards 1.70%, now at 1.671% at the time of typing.

- 1.70% would equate to 144.12 in futures.

- Peripheral spreads are mixed, Italy trades 3.3bps tighter today, while Greece is 8.5bps wider.

- Bund underperforms Gilt and Treasuries, as investors price a more aggressive rate path from the ECB.

- Early heavy European supply was also a factor on delta hedging for EGBs versus the Gilt.

- The fall in the Pound has also kept the Gilt underpinned.

- Gilt/Bund spread has tightened 9.6bps, and eye the 2022 low at 79.03, now at 79.6bps.

- Below the latter, opens to the 2021 low at 75.69.

- Looking ahead, all the attention turns to the Fed tomorrow.

FOREX: GBPUSD Falls Below 1.20 As Greenback Maintains Upward Trajectory

- GBP was the clear outlier on Tuesday, sinking around 1.35% to its lowest level against the US Dollar since March 2020. Weakness was even more pronounced in the cross with EURGBP extending to 13-month highs just below the 0.8700 mark.

- Cable’s move lower this week confirms a resumption of the primary downtrend and the next technical support point resides at 1.1934, the high on Mar 20, 2020. In similar vein, EURGBP has cleared resistance at 0.8619, the May 12 high and an important short-term bull trigger. The immediate focus is on 0.8701, the May 7 2021 high and 0.8721, the Apr 26 high.

- Euro weakness was contained by the appreciation against GBP on Tuesday, however, a brief pop to 1.0485 in EURUSD was well sold into with the pair gravitating back to around the 1.0400 handle as we approach the APAC crossover.

- With US yields at recent highs and equity benchmarks consolidating at the lows, the USD Index (+0.40%) looks set to post a fifth consecutive winning session. US May PPI came in basically in line with expectations, but a touch on the soft side for core readings and downward revisions to April – having very little impact on the greenback.

- Overall, the greenback strength was broad based with not only the likes of AUD, NZD and CAD retreating but also weakness filtering through to CHF and JPY. USDJPY is making fresh 24-year highs above 1.3520 as of writing.

- The Chinese Yuan bucked the trend with USDCNH seen 0.42% lower on Tuesday.

- Wednesday will bring April data for euro area IP and goods trade and the final estimates of French inflation in May. On the US docket, May retail sales and June Empire Manufacturing are notable data points before the June FOMC decision/SEP and subsequent press conference with Chair Powell.

- Central bank decisions from both the SNB and BOE are also due on Thursday.

FX OPTIONS: Expiries for Jun15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500-11(E817mln)

- USD/JPY: Y131.50($550mln), Y134.00($593mln)

- GBP/USD: $1.2180-90(Gbp827mln)

- EUR/GBP: Gbp0.8515-20(E551mln), Gbp0.8600-20(E523mln)

- AUD/USD: $0.7050(A$651mln)

- USD/CNY: Cny6.6500($1.3bln)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/06/2022 | 0200/1000 | *** |  | CN | Fixed-Asset Investment |

| 15/06/2022 | 0200/1000 | *** | | CN | Retail Sales |

| 15/06/2022 | 0200/1000 | *** | | CN | Industrial Output |

| 15/06/2022 | 0200/1000 | ** | | CN | Surveyed Unemployment Rate |

| 15/06/2022 | 0645/0845 | *** |  | FR | HICP (f) |

| 15/06/2022 | 0900/1100 | ** |  | EU | industrial production |

| 15/06/2022 | 0900/1100 | * | | EU | Trade Balance |

| 15/06/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 15/06/2022 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 15/06/2022 | 1230/0830 | *** | | US | Retail Sales |

| 15/06/2022 | 1230/0830 | ** | | US | Import/Export Price Index |

| 15/06/2022 | 1230/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/06/2022 | 1300/0900 | * | | CA | Home Sales – CREA (Canadian real estate association) |

| 15/06/2022 | 1315/1515 | | EU | ECB Panetta Intro Statement on Digital Euro at ECON | |

| 15/06/2022 | 1400/1000 | * | | US | Business Inventories |

| 15/06/2022 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 15/06/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 15/06/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 15/06/2022 | 1620/1820 | | EU | ECB Lagarde in conversation with Jose Vinals at LSE | |

| 15/06/2022 | 1800/1400 | *** | | US | FOMC Statement |

| 15/06/2022 | 2000/1600 | ** | | US | TICS |

| 16/06/2022 | 2245/1045 | *** |  | NZ | GDP |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok