Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Back Where We Started

Tsys currently trading firmer, are well off first half highs after the bell. Rate support evaporated after the $33B 10Y note auction reopen tailed, the high yield of 2.960% vs. 2.937% WI -- actually matched the high yield for the $34B 1Y bill sale earlier in the session. Rates pared gains/extended session lows while yield curves finished flatter but well off lows as accts square up ahead Wed's CPI MoM (1.0%, 1.1%); YoY (8.6%, 8.8%).- Early rate bid: US rates took cues from German Bunds in early London trade, rallied on weak ZEW current Conditions -45.8. Tsy futures traded back to last week's pre-FOMC minutes levels: 30YY falling to 3.0833% in the first half.

- Large Block buys in 2s (37.5k) and 5s (15.1k) earlier. Pre-auction short sets ahead US Tsy $33B 10Y Note auction re-open (91282CEP2) at 1300ET.

- Earlier comments from Richmond Fed's Barkin ('24 voter) appears to see increased difficulty at managing a soft-landing in the economy when updating remarks from a Jun 21 speech called the Recession Question.

- Reminder: Earnings season kicks off this week, with financials and banks the early focus. Just over 5% of the S&P 500 by market cap are due to report, with the releases in focus including JP Morgan, Morgan Stanley, BNY Mellon, BlackRock, Citigroup, State Street, UnitedHealth and Wells Fargo.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00443 to 1.56829% (+0.00772/wk)

- 1M +0.00700 to 1.97143% (+0.07172/wk)

- 3M +0.02786 to 2.48300% (+0.06000/wk) * / **

- 6M -0.00600 to 3.06443% (+.01600/wk)

- 12M -0.03529 to 3.68671% (+0.04185/wk)

- * Record Low 0.11413% on 9/12/21; ** New 3Y high: 2.48300% on 7/12/22

- Daily Effective Fed Funds Rate: 1.58% volume: $93B

- Daily Overnight Bank Funding Rate: 1.57% volume: $269B

- Secured Overnight Financing Rate (SOFR): 1.53%, $930B

- Broad General Collateral Rate (BGCR): 1.51%, $359B

- Tri-Party General Collateral Rate (TGCR): 1.51%, $353B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,146.132B w/ 96 counterparties vs. $2,164.266B prior session. Record high stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Second consecutive session of limited option volume Tuesday, flow mildly bullish with put unwinds and call buys with underlying futures trading higher, 30YY falling to 3.0833% low before climbing back to 3.1240% after the bell.- Highlight Eurodollar trade includes put skew sale with 5,000 Dec 96.00 puts 6.0 over 96.25/96.75 call spreads. Midcurve call buyer paid 40.5 for 5,000 Green Dec 97.25 calls vs. 97.185/0.45%.

- Limited SOFR trade had paper buying 7,000 SFRZ2 96.50/97.00/98.00 broken call flys.

- 7,000 SFRZ2 96.50/97.00/98.00 broken call flys

- +5,000 Green Dec 97.25 calls, 40.5 vs. 97.185/0.45%

- seller Dec 96.25 straddles 72.5 vs. 73.0 settle

- 7,000 short Jul 96.43/96.56 put spds

- -5,000 Dec 96.00 puts 6.0 over 96.25/96.75 call spds

- Block, 5,000 Oct 96.00/96.25 put spds, 10.5

- +8,500 wk3 TY 116.75/117.75 put spds, 12 vs. 118-17.5/0.10%

- -7,500 TYQ 118/120 put over risk reversals, 1 net ref 118-31.5

- -5,000 USU 130 puts, 20

- 2,500 wk3 TY 118.75/119.75 1x2 call spds, 11

- Block, 10,000 FVU 113 calls, 50.5

- Block, total 15,000 FVU 111.75 puts, 49.5-51 vs. TUU 104-29.75/0.50%

- 5,000 TYU 117.5 puts, 60

- 6,300 FVQ 112.75 calls, 20

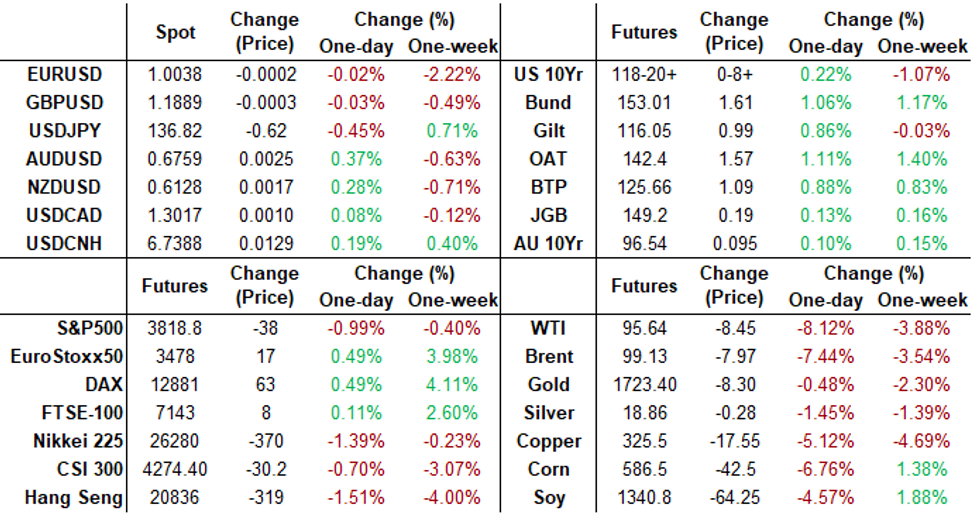

EGBs-GILTS CASH CLOSE: Recession Drumbeat Continues

Tuesday saw another strong rally across the UK and German curves as the euro touched parity with the US dollar.

- Most of the session's rally took place over the morning, punctuated by a miss in the German ZEW data, with falling commodity prices helping moderate inflation expectations as well.

- There was a bit of retracement higher in yields in the afternoon as traders began eyeing Wednesday's key US inflation report.

- In contrast to bull steepening moves in prior sessions, outperformance Tuesday was further along the curve (German Buxl yields fell 13+bp, UK 10Y down 10+).

- Periphery spreads widened but ended well off session's widest levels.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 8.7bps at 0.355%, 5-Yr is down 9.2bps at 0.773%, 10-Yr is down 11.4bps at 1.132%, and 30-Yr is down 13.1bps at 1.406%.

- UK: The 2-Yr yield is down 8.8bps at 1.792%, 5-Yr is down 10bps at 1.756%, 10-Yr is down 10.3bps at 2.075%, and 30-Yr is down 3.2bps at 2.57%.

- Italian BTP spread up 1.6bps at 198.2bps / Spanish up 0.6bps at 109.5bps

EGB Options: Euribor Vol Selling And More August Bund Structures

Tuesday's Europe bond/rate options flow included:

- RXQ2 151/153cs, sold at 100 in 4.5k

- RXU2 151.00/150.50/140.00p ladder, bought for -0.5 in 3.4k

- RXQ2 150/147 put spread bought for 36.5 in 2k

- RXQ2 155 call sold at 76 in 2k

- RXQ2 156.50 call sold at 40 in 5k (closing)

- 0RN2 98.50^, sold at 23 and 22 in 1.5k

- 2RZ2 99.00/99.75cs, bought for 18 in 6k

- SFIZ2 96.80/97.10/97.60/97.90c condor, bought for 9.5 in 3k

FOREX: EURUSD Parity Holds As Early Greenback Strength Reverses

- Having started the Tuesday session as the best performer, the dollar was knocked off its perch by fierce defence of parity in EUR/USD, which marked not just a key psychological level but also the base of the bear channel drawn off the February highs.

- Currency futures markets showed considerable spikes in activity that coincided with the EUR/USD approach to 1.00 - suggesting sizeable defence of the level and helped a recovery back above 1.0050 ahead of the London close.

- As a result, the USD became one of the weakest currencies of the session into the close, partially reversing the week's 1.00% rally in the USD Index.

- Meanwhile, an extension of the downleg in commodity prices worked against oil-tied FX, with NOK underperformance persisting and putting the currency at new multi-year lows against the USD. The NOK weakness posted since Monday continues to put the currency below the Norges Bank's projections outlined at the June policy meeting - adding more pressure to the board to tighten policy and contain any imported inflationary pressures.

- USD weakness was further reflected in the USD/JPY pullback to Y136.50, however the outlook remains bullish following the break of key resistance at 137.00 earlier in the week. This confirmed the resumption of the primary uptrend and highlights that corrections remain shallow, reinforcing underlying bullish conditions.

- Final German CPI data crosses Wednesday, as well as UK industrial and manufacturing production data and the US CPI reading for June. Markets expect core CPI Y/Y to decelerate to 5.7% from the 6.0% posted in May. The Bank of Canada also decide on rates, with analysts expecting a 75bps rate rise to 2.25%. The full MNI Preview can be found here: https://marketnews.com/mni-boc-preview-jul-22-eyei...

Expiries for Jul13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0195-00(E1.0bln)

- GBP/USD: $1.2035(Gbp1.2bln)

- USD/JPY: Y134.40-55($1.1bln), Y136.00($830mln)

- EUR/JPY: Y137.00(E936mln), Y138.00(E641mln), Y139.00(E823mln)

- NZD/USD: $0.6180(N$794mln)

- USD/CAD: C$1.3000($1.6bln)

- USD/CNY: Cny6.7500($615mln)

Late Equity Roundup: Late Reversal

Stocks softening up after the FI close, extending session lows but still off overnight levels, all in all a narrow range ahead Wed's CPI. SPX eminis currently trading -34.5 (-0.89%) at 3821.75; DJIA -175.29 (-0.56%) at 30998.31; Nasdaq -120.2 (-1.1%) at 11251.54.

- SPX leading/lagging sectors: Materials (+0.08%), Consumer Staples (+0.01%) followed by Industrials (-0.08%) and Financials (-0.17%). Laggers: Energy sector continued to underperform (-2.53%) with the drop in crude prices on the day (WTI -8.50 at 95.59) with Hess, Occidental Petro, Valero, Diamondback shares broadly weaker. Information Tech (-1.32%) followed by Health Care (-1.32%)

- Dow Industrials Leaders/Laggers: Boeing (BA) +11.82 at 148.81, Apple (AAPL) +2.16 at 147.03, Goldman Sachs (GS) +1.94 at 295.12. Laggers: Microsoft (MSFT) -9.28 at 255.23, Salesforce.com (CRM) -6.82 at 167.54, followed by Chevron (CVX) -2.50 at 139.01

- Reminder: Earnings season kicks off this week, with financials and banks the early focus. Just over 5% of the S&P 500 by market cap are due to report, with the releases in focus including JP Morgan, Morgan Stanley, BNY Mellon, BlackRock, Citigroup, State Street, UnitedHealth and Wells Fargo.

E-MINI S&P (U2): Key Resistance Still Intact

- RES 4: 4308.50 High Apr 28

- RES 3: 4204.75 High May 31 and a key resistance

- RES 2: 3980.07 50-day EMA

- RES 1: 3950.00 High Jun 27

- PRICE: 3849.00 @ 14:19 BST Jul 12

- SUP 1: 3735.00/3639.00 Low Jun 23 / 17 and the bear trigger

- SUP 2: 3578.27 0.618 proj of the Mar 29 - May 20 - 31 price swing

- SUP 3: 3500.00 Round number support

- SUP 4: 3384.75 0.764 proj of the Mar 29 - May 20 - 31 price swing

S&P E-Minis traded higher last week and price remains above recent lows. The outlook is unchanged and bearish, following the reversal from 3950.00, the Jun 28 high. The next support lies at 3735.00, the Jun 23 low. A breach of this level would expose key support at 3639.00, the Jun 17 low. On the upside, clearance of resistance at 3950.00 is required to reinstate a bullish theme. This would open the 50-day EMA, currently at 3980.07.

COMMODITIES: Oil Tumbles On Demand Fears

- Crude oil has tumbled today, with what started out overnight as weakness on Chinese demand fears amidst Shanghai mass Covid testing before the US coming in drove a much sharper decline on demand fears.

- WTI falls slightly more than Brent, possibly on US domestic oil production seen increasing at a slower pace than initially forecast pace through 2023, with EIA projecting 12.77mbpd vs an initial 12.97mbpd from an estimated 11.11mbpd this year.

- Tight supply and low inventories supported refined product cracks despite the fall in crude.

- WTI is -7.5% at $96.23 as it closes in on the bear trigger at $95.10 (Jul 6 low), clearance of which could open $93.45 (Apr 25 low) and beyond. Sliding prices have seen the most active strikes in the Aug;22 contract at $95/bbl and $90/bbl puts.

- Brent is -6.8% at $99.89, also closing in on the bear trigger at $98.50 (Jul 6/7 low).

- Gold is -0.44% at $1726.38 on a volatile session around a southbound trend despite a rolling over in UDS strength. It is close to testing support at $1721.7 (Sep 29, 2021 low) clearance of which could open $1706.8 (1.618 proj of the Mar 8-29-Apr18 price swing).

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/07/2022 | 0600/0700 | *** |  | UK | Index of Production |

| 13/07/2022 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 13/07/2022 | 0600/0700 | ** | | UK | Trade Balance |

| 13/07/2022 | 0600/0700 | ** | | UK | Index of Services |

| 13/07/2022 | 0600/0700 | ** | | UK | UK Monthly GDP |

| 13/07/2022 | 0600/0800 | *** |  | DE | HICP (f) |

| 13/07/2022 | 0645/0845 | *** |  | FR | HICP (f) |

| 13/07/2022 | 0900/1100 | ** |  | EU | industrial production |

| 13/07/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 13/07/2022 | - | *** |  | CN | Trade |

| 13/07/2022 | 1230/0830 | *** | | US | CPI |

| 13/07/2022 | 1400/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 13/07/2022 | 1400/1000 | | CA | BOC Monetary Policy Report | |

| 13/07/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 13/07/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 13/07/2022 | 1500/1100 | | CA | BOC press conference | |

| 13/07/2022 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 13/07/2022 | 1800/1400 | ** | | US | Treasury Budget |

| 13/07/2022 | 1800/1400 | | US | Federal Reserve Beige Book |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.