Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: Rates Off Highs Into Month End

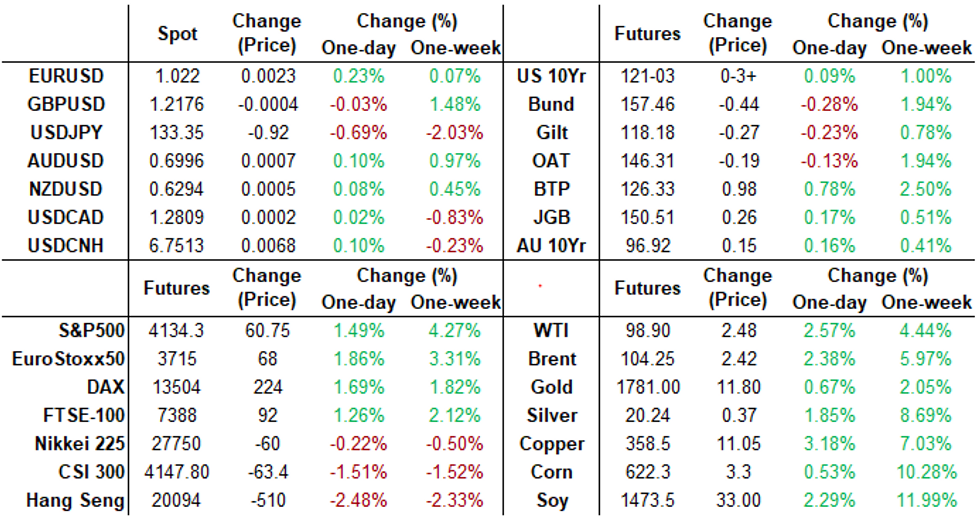

Tsys futures remain mixed by the bell, curves flatter with short end underperforming: 2s10s -4.966 at 24.198, 5s10s -2.275 at -4.803.

- Weaker data in-line w/ more moderate rate hikes later in the year: Little initial reaction after slight gain in June reading of Personal Income is +0.6% MoM vs. +0.5 est, PCE Deflator is +1.0% MoM vs. +0.9% est, and ECI +1.3% vs. +1.2% est. Rates and stocks moved higher after the Chicago Business BarometerTM, produced with MNI, slid further in July, extending June's decline. The indicator fell 3.9-points to 52.1, the lowest level since August 2020.

- Exogenous factors: Tsys had come under pressure in early London hours after higher than expected French, Italian and Spanish GDP economic data triggered selling in EGBs w/ brief pause after weaker than expected German GDP.

- Meanwhile, Fed speakers out of media blackout: Atlanta Fed Bostic broke the seal earlier, reiterating Chair Powell's talking point: we are not in a recession, but inflation needs to be addressed w/ "more work needs to be done on bringing demand and supply into balance".

- Next Monday data: S&P Global Mfg data (52.4 est), ISMs (mfg 52.0 est; prices paid 73.5 est), JOLTS job openings (10.994M).

- Current cross assets: spot Gold +5.35 at 1761.19, Crude firmer but off early highs WTI +2.18 at 98.60, stocks on high ESU2 +64.50 at 4138.00 -- highest level sine June 9..

- Currently, 2-Yr yield is up 4.1bps at 2.9027%, 5-Yr is up 1bps at 2.7079%, 10-Yr is down 1.1bps at 2.665%, and 30-Yr is down 1.7bps at 3.0057%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.01814 to 2.32157% (+0.75700/wk)

- 1M -0.01085 to 2.36229% (+0.11000/wk)

- 3M +0.00600 to 2.78829% (+0.02200/wk) * / **

- 6M -0.01085 to 3.32986% (+0.00700/wk)

- 12M -0.05485 to 3.70729% (-0.10700/wk)

- * Record Low 0.11413% on 9/12/21; ** New 3.5Y high: 2.80586% on 7/27/22

- Daily Effective Fed Funds Rate: 2.33% volume: $90B

- Daily Overnight Bank Funding Rate: 2.32% volume: $287B

- Secured Overnight Financing Rate (SOFR): 2.28%, $965B

- Broad General Collateral Rate (BGCR): 2.25%, $382B

- Tri-Party General Collateral Rate (TGCR): 2.25%, $372B

- (rate, volume levels reflect prior session)

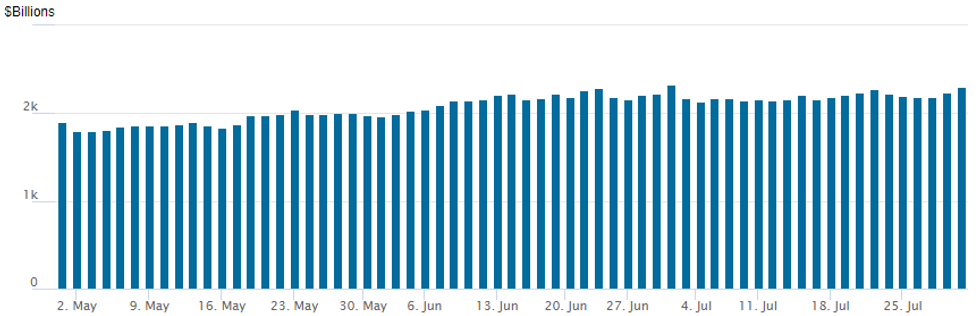

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,300.200B w/ 111 counterparties vs. $2,239.883B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Limited option volumes reported Friday, two-way trade as underlying futures climbed off late overnight lows.SOFR Options:

- Block, 2,000 SFRQ2 96.75/96.87 put spds, 1.75

- Block, 1,300 SFRQ2 96.81/96.87/96.93/97.06 call condors

- -4,500 Dec 97.37 straddles

- 1,250 Green Sep 96.87/97.00/97.12/97.25 put condors

- 1,500 Green Aug 97.12/97.37/97.62 call trees

- -2,000 short Dec 98.50 calls, 19.0

- -1,000 Aug 97.00/97.25/97.50 call flys, 4.25

- Block, 7,000 98.00/99.00 call spds, 2.0 ref 96.965

- 2,000 TYU 120.75 calls, 104 ref 120-23.5

- +4,000 USU 134/138 put spds, 25

- +10,000 wk1 FV 112.5/113 put spds, 6-6.5

- 7,000 wk5 TY 120.25 puts, 6

EGB/Gilts - Govies recover from their lows

EGBs and Bund have recovered from the session lows, as EU desks start to likely cover as we head towards the later part of the session.

- Month End could also be at play, but more would be expected towards 16.15BST.

- Most notable extensions are in the UK, a huge +0.20yr, while EU and the US sees smaller/average extensions.

- A decent turn around for the BTP, and good continuation following this morning's headline:

- "Meloni Would Stick To EU Budget Rules If She Becomes PM-Officials"

- Italy is now 12.8bps tighter against the German 10yr, and all peripheral are tighter, besides Greece that sits 2.3bps wider.

- Looking ahead, attention turns to the BoE and US NFP next week.

Notable data for next week:

- Manufacturing PMIs (mostly final readings for core), US ISM/Price paid (Mon), Swiss CPI, Turkey CPI, Global Services PMIs (mostly final for core), US ISM Services Index (Wed), German, French, Italian IP, Canadian Employment, US NFP (Fri).

FOREX: Significant FX Volatility, Greenback Pares Gains Into Month-End

- G10 currencies remained highly volatile on Friday and despite a closing snapshot indicating no sizeable daily adjustments, most majors exhibited significant intra-day ranges to finish the week.

- USDJPY looks set to post 2% losses for the week and is the weakest pair on Friday (-0.75%). However, multiple whipsaws were experienced throughout the volatile trading day. In an extension of yesterday’s weakness and as a product of the softer US growth data and lower yields, USDJPY initially traded down as much as 1.3% overnight, printing a six-week low at 132.51 as Europe sat down.

- However, strong reversals across the currency space amid possible profit taking, combined with potential month-end dynamics, led to a sharp reversal higher. Some slightly firmer US data exacerbated the greenback relief rally, prompting USDJPY to print a 134.59 high, over 200 pips off the lows and closely matching the overnight highs.

- The broad dollar strength saw similar moves across the FX space, although the rally lost steam and once again reversed course approaching the month-end WMR fix. The USD index fell back into negative territory and looks set to extend its losing streak to three consecutive sessions.

- Similarly, GBPUSD saw initial support amid the early greenback weakness, reaching a one-month high of 1.2239. However, the rally met stiff resistance with weaker domestic data fuelling the turnaround. Despite the resulting 180-pip move to the downside, GBP had a notable bounce ahead of the month-end fix, rising over 100 pips to trade close to unchanged at 1.2170 approaching the close. Technically, initial firm support to watch lies at 1.1890, the Jul 21 low. A break of which would signal a resumption of bearish activity.

- US ISM Manufacturing PMI highlights Monday’s data docket, however, markets will remain more concerned over Friday’s release of non-farm payrolls following the Fed’s increased importance on the upcoming data. There will be central Bank decisions from both the RBA and the BOE.

FX: Expiries for Aug01 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0100-25(E1.2bln), $1.0200-10(E692mln), $1.0250(E550mln), $1.0300(E842mln)

- GBP/USD: $1.2125(Gbp587mln)

Late Equity Roundup, Extending Gains

Stocks continue to extend session highs heading into the FI close, SPX futures at the highest level since June 9, lead by Energy and Consumer Discretionary sectors.

- Currently, SPX eminis trade +55.75 (1.37%) at 4129; DJIA +276.07 (0.85%) at 32804.9; Nasdaq +210.5 (1.7%) at 12372.85. Midmorning support for stocks and rates: MNI's Chicago Business BarometerTM indicator fell 3.9-points to 52.1, the lowest level since August 2020, as rate hike expectations in the latter half of the continue to ease.

- SPX leading/lagging sectors:Energy sector outperforming (+4.41%) lead by Chevron (CVX) +8.58%, Exxon (XOM) +4.39% (both beat earnings ests this morning: CVX $5.82 vs. $4.965 est, XOM $4.14 vs. $3.975 est.

- Consumer Discretionary (+4.23%) lead by internet/direct marketing shares and auto manufacturers: Amazon +11.76% despite missing earnings est of $0.15 at $0.10, Ford (F) +4.18%, outpacing Tesla (TSLA) +3.93%. Laggers: Consumer Staples (-0.78%), Health Care (-0.63%), Real Estate (+0.28%) and Communication Services (+0.40%)

- Dow Industrials Leaders/Laggers:Caterpillar (CAT) +10.72 at 198.56, Apple (AAPL) +5.43 at 162.77. Laggers: Proctor and Gamble (PG) -7.98 at 140.08, Intel (INTC) -3.40 at 36.31.

E-MINI S&P (U2): Bulls Still In The Driver's Seat

- RES 4: 4345.75 2.00 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 3: 4306.50 High May 4

- RES 2: 4204.75 High May 31 and a key resistance

- RES 1: 4145.75 High Jun 9

- PRICE: 4135.00 @ 1500 BST Jul 29

- SUP 1: 3913.25 Low Jul 26 and key near-term support

- SUP 2: 3820.25 Low Jul 18

- SUP 3: 3723.75/3639.00 Low Jul 14 / Low Jun 17 and a bear trigger

- SUP 4: 3578.27 0.618 proj of the Mar 29 - May 20 - 31 price swing

S&P E-Minis traded higher Thursday, marking an extension of Wednesday's climb that resulted in a breach of 4016.25, the Jul 22 high. The break higher confirms a resumption of the current bull cycle and signals potential for a climb towards 4145.75, the Jun 9 high. The next key resistance is at 4204.75, the May 31 high. Initial support has been defined at 3913.25, the Jul 26 low. A break would highlight a possible early bearish reversal signal.

COMMODITIES

- WTI Crude Oil (front-month) up $2.49 (2.58%) at $98.93

- Gold is up $8.62 (0.49%) at $1764.46

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 31/07/2022 | 0130/0930 | *** |  | CN | CFLP Manufacturing PMI |

| 31/07/2022 | 0130/0930 | ** | | CN | CFLP Non-Manufacturing PMI |

| 01/08/2022 | 2300/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

| 01/08/2022 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 01/08/2022 | 0145/0945 | ** | | CN | IHS Markit Final China Manufacturing PMI |

| 01/08/2022 | 0600/0800 | ** |  | DE | retail sales |

| 01/08/2022 | 0715/0915 | ** |  | ES | IHS Markit Manufacturing PMI (f) |

| 01/08/2022 | 0745/0945 | ** |  | IT | IHS Markit Manufacturing PMI (f) |

| 01/08/2022 | 0750/0950 | ** |  | FR | IHS Markit Manufacturing PMI (f) |

| 01/08/2022 | 0755/0955 | ** | | DE | IHS Markit Manufacturing PMI (f) |

| 01/08/2022 | 0800/1000 | ** |  | EU | IHS Markit Manufacturing PMI (f) |

| 01/08/2022 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Manufacturing PMI (Final) |

| 01/08/2022 | 0900/1100 | ** | | EU | Unemployment |

| 01/08/2022 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (final) |

| 01/08/2022 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 01/08/2022 | 1400/1000 | * | | US | Construction Spending |

| 01/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 01/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 01/08/2022 | 1900/1500 | | US | Treasury Marketable Borrowing Estimates |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.