Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS: ISM Prices Paid Falls

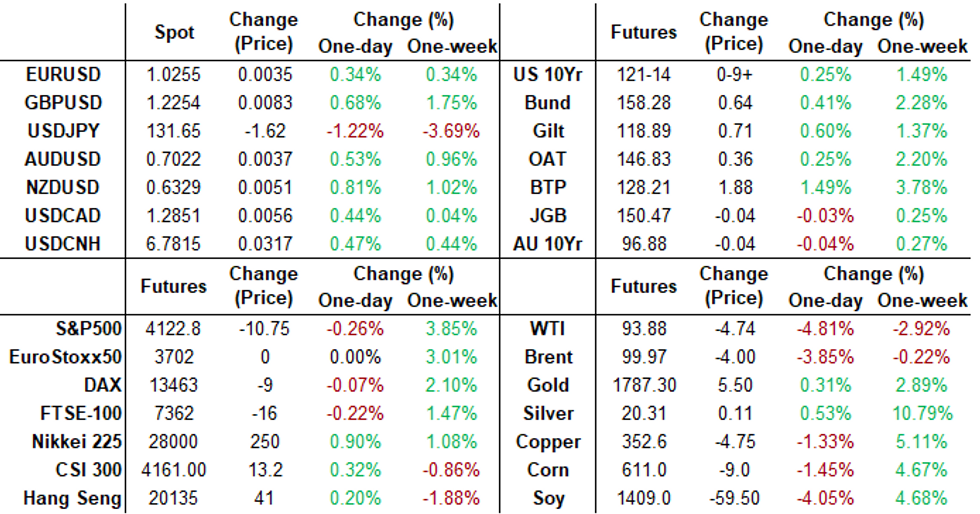

Tsys holding narrow range, near session highs for the last few hours, decent volumes (TYU >1.18M), curves flatter with short end underperforming: 2s10s -31.676 inverted low just off last week's 22Y low of -32.142.

- Data headwinds: The US ISM Manufacturing PMI edged down a modest 0.2pp to 52.8 in July, but stronger than the forecast of 52.0. Read is lowest since June 2020 and the second consecutive month of decline. Metric remains in expansive territory above the 50-point threshold.

- Substantial fall was seen in the prices paid index: -18.5 points to 60.0, the lowest since Aug'20. This is a much slower price growth. Volatility in commodity markets underscores this steep decline, with a significant 21.5% of respondents paying less in July (compared to June).

- Meanwhile, June construction spending declined -1.1% vs. +0.1% estimate, carry-over slowdown in economic data from last week a headwind for more aggressive Fed pricing at the Sep 21 FOMC.

- First-half block buys in 5s helped kick off the early bid, preceded duration neutral 5s30s flattener (-12,000 FVU 113-20 vs. +3,300 USU 144-10.)

- Limited data on tap for Tuesday: JOLTS Job Openings (10.994M est) and vehicle sales throughout the day. Larger focus on Friday's July employment data (+250k est vs. +372k prior).

- Cross assets: spot Gold +4.75 at 1770.69, Crude weaker: WTI -4.49 at 94.13, stocks mildly weaker ESU2 -10.50 at 4122.75.

- Currently, 2-Yr yield is up 1.6bps at 2.9005%, 5-Yr is down 1.7bps at 2.6592%, 10-Yr is down 5.4bps at 2.5947%, and 30-Yr is down 9.2bps at 2.9175%

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N -0.01000 to 2.31157% (+0.75700/wk)

- 1M +0.00457 to 2.36686% (+0.11000/wk)

- 3M +0.01385 to 2.80214% (+0.02200/wk) * / **

- 6M +0.04628 to 3.37614% (+0.00700/wk)

- 12M +0.03485 to 3.74214% (-0.10700/wk)

- * Record Low 0.11413% on 9/12/21; ** New 3.5Y high: 2.80586% on 7/27/22

- Daily Effective Fed Funds Rate: 2.32% volume: $86B

- Daily Overnight Bank Funding Rate: 2.31% volume: $240B

- Secured Overnight Financing Rate (SOFR): 2.27%, $949B

- Broad General Collateral Rate (BGCR): 2.25%, $374B

- Tri-Party General Collateral Rate (TGCR): 2.25%, $365B

- (rate, volume levels reflect prior session)

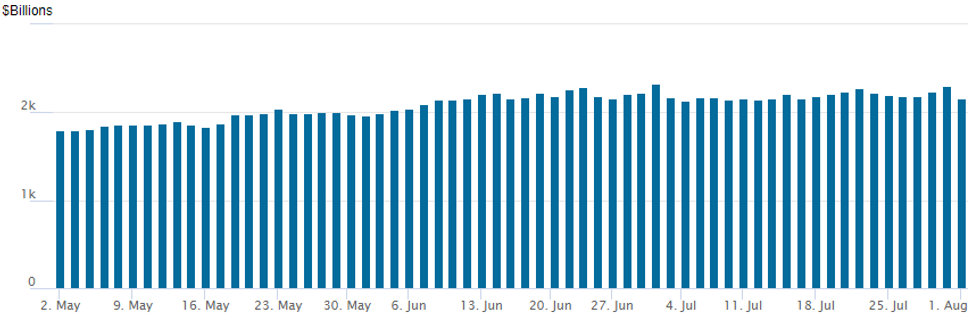

FED Reverse Repo Operation

NY Federal Reserve/MNI

New month underway, NY Fed reverse repo usage falls to $2,161.885B w/ 103 counterparties vs. $2,300.200B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

SOFR Options:- Block total 7,500 SFRF3 96.75/97.25 1x2 call spds, 0.0 w/

- total 7,500 SFRH3 96.75/97.25 1x2 call spds, 4.0

- Block, 4,000 SFRV2 96.25/96.50 put spds, 6.0

- Block, 5,000 SFRU2 96.50/96.75 put spds, 1.5

- Block, 10,000 SFRV2 96.37/96.50/96.62 put flys, 1.25

- Block +5,000 SFRV2 97.00/97.12/97.25 call flys, 1.0

- 5,000 Sep 99.50/99.75 put spds

- 18,500 Dec 97.12/97.25 call spds

- 2,000 short Sep 96.37/96.62 put spds

- 10,000 TYX 125.5 calls, 29

- 3,500 10Y short Aug

- 4,500 wk1 FV 112.5 puts, 02.5

FOREX: USD Index Extends Losing Streak, JPY Strength In Focus

- After a volatile open to the week, the greenback overall traded with a greater sense of calm over the US session as markets prepare themselves for Friday’s US Employment data. With this said, the USD index (-0.40%) looks set to post its fourth consecutive losing session, extending the dollar’s downward momentum seen throughout the second half of July.

- The largest moves have once again been in the Japanese Yen. Despite Friday’s bounce in USDJPY, the pair succumbed to further selling pressure on Monday, making fresh lows below the 132 handle. The move appears to be a continuation of dynamics that were in play towards the back end of last week, with participants exiting short JPY positions amid the recent trimming of hawkish Fed bets.

- Further weakness throughout the US session saw USDJPY narrow the gap with key support at 131.50, the Jun 16 low and despite the pair bouncing roughly 35 pips ahead of the APAC crossover, it remains down 1% on the day around 131.95.

- While losses for the greenback were fairly broad based, there were some notable divergences across G10, with the Canadian dollar particularly weak on Monday. CAD is down 0.45% and the weakness can be largely attributed to the pressure on crude prices with WTI futures falling 5%. In similar vein, the Chinese Yuan is weaker on Monday amid a softer than expected manufacturing PMI released out of China since Friday’s close and ongoing political tensions centred around a potential trip from the US speaker to Taiwan.

- On the other hand, NZD (+0.80%) outperforms and the kiwi may have been helped by AUD/NZD sales in response to the weak Chinese data. The Antipodean cross slid below the NZ$1.1100 mark, with activity in Australia limited by a New South Wales holiday.

- The focus on Tuesday will be on the RBA. The continued tightening of the labour market, level of inflation and expected acceleration in price pressures through year-end means that the RBA will likely lift its cash rate target by 50bp at its meeting on Tuesday.

- Later in the week, the Bank of England have a monetary policy decision on Thursday before Friday’s US employment data.

Expiries for Aug02 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9900(E1.0bln), $1.0000(E1.4bln), $1.0240-45(E556mln)

- EUR/GBP: Gbp0.8647-65(E1.2bln)

- EUR/JPY: Y135.85-00(E664mln)

- AUD/USD: $0.7160(A$641mln)

- USD/CAD: C$1.2890-00($647mln)

Late Equity Roundup: Consumer Staples Outpace Discretionary

Stocks trading mildly lower after the FI close, off early session lows on modest two-way flow after climbing to six week highs last Friday. Generally quiet summer trade with many accts sidelined ahead this Fri's July employment report.

- Currently, SPX eminis trade - 7.5 (-0.18%) at 4126.25; DJIA -4.07 (-0.01%) at 32843.01; Nasdaq -8 (0.1%) at 12399.24. Stocks gained with rates earlier on data headwinds for rate hikes: Substantial fall was seen in the ISM prices paid index, which plunged 18.5 points to 60.0, the lowest since August 2020; June construction spending declined -1.1% vs. +0.1% est.

- SPX leading/lagging sectors: Consumer Stales (+1.0%) lead by household and personal products, Consumer Discretionary (+0.49) as retailing outpaced autos (car sales reported through Tue' session). Laggers: Energy (-2.4%) as crude sells off (WTI -4.76 at 93.86), Financials (-1.18%), Materials (-1.08%).

- Dow Industrials Leaders/Laggers: Boeing (BA) +10.29 at 169.60, Home Depot (HD) +4.90 at 305.84, Proctor and Gamble (PG) +4.10 at 143.01. Laggers: United Health (UNH) -10.01 at 532.33, Chevron (CVX) -3.39 at 160.39, Microsoft (MSFT) -3.04 at 277.70.

- Earnings releases continue after session close: Avis Budget Grp (CAR) $11.165 est, Williams (WMB) $0.365 est, SBA Communications (SBAC) $2.561 est, Diamondback Energy (FANG) $6.624, Mosaic (MOS) $4.0 est.

E-MINI S&P (U2): Bull Cycle Extends

- RES 4: 4345.75 2.00 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 3: 4306.50 High May 4

- RES 2: 4204.75 High May 31 and a key resistance

- RES 1: 4147.25 High Aug 01

- PRICE: 4142.50 @ 16:54 BST Aug 1

- SUP 1: 3967.78/13.25 50-day EMA / Low Jul 26 and key S/T support

- SUP 2: 3820.25 Low Jul 18

- SUP 3: 3723.75/3639.00 Low Jul 14 / Low Jun 17 and a bear trigger

- SUP 4: 3578.27 0.618 proj of the Mar 29 - May 20 - 31 price swing

S&P E-Minis traded higher again Monday, reinforcing bullish conditions and maintaining the current price sequence of higher highs and higher lows. Potential is for a climb towards 4204.75, the May 31 high. On the downside, initial trend support has been defined at 3913.25, the Jul 26 low. A break would highlight a possible early bearish reversal signal.

COMMODITIES

- WTI Crude Oil (front-month) down $4.73 (-4.8%) at $93.99

- Gold is up $5.07 (0.29%) at $1770.98

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 02/08/2022 | 0130/1130 | * |  | AU | Building Approvals |

| 02/08/2022 | 0130/1130 | ** | | AU | Lending Finance Details |

| 02/08/2022 | 0430/1430 | *** | | AU | RBA Rate Decision |

| 02/08/2022 | 0600/0700 | * |  | UK | Nationwide House Price Index |

| 02/08/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 02/08/2022 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 02/08/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 02/08/2022 | 1400/1000 | | US | Chicago Fed's Charles Evans | |

| 02/08/2022 | 1400/1000 | ** | | US | housing vacancies |

| 02/08/2022 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 02/08/2022 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 02/08/2022 | 1700/1300 | | US | Cleveland Fed's Loretta Mester | |

| 02/08/2022 | 2245/1845 | | US | St. Louis Fed's James Bullard |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.