Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

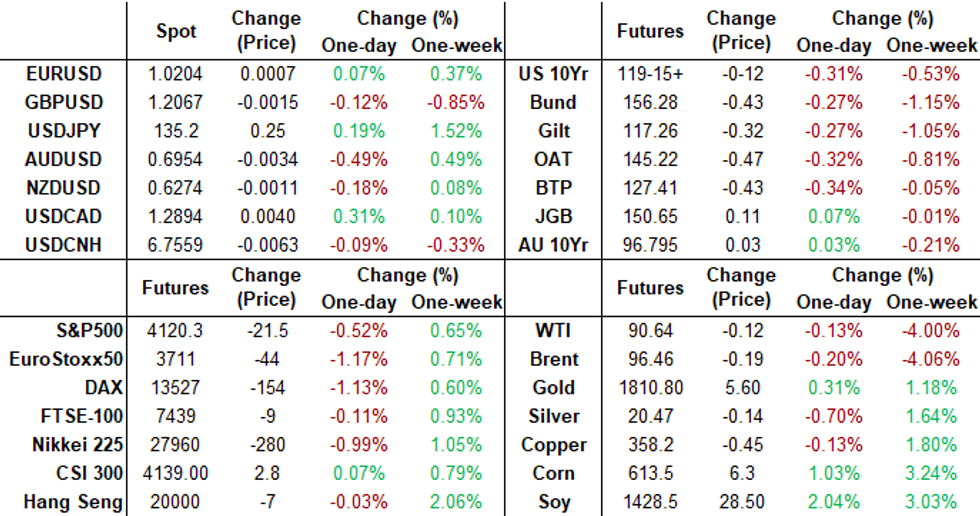

US TSYS: Tsys Hold Weaker/Narrow Range Ahead Wed's July CPI

Treasury futures hold modestly weaker after the bell, near middle of session range on light summer volumes (TYU2<815k) - thin participation ahead of Wednesday's key CPI data: 0.2% est, 1.3% prior; YoY 8.7% est, 9.1% prior. Yield curves mostly flatter after the bell, 2s10s nearly tapped -50.0, new 22 year low of -49.264.

- Morning data spurred buying in intermediates to long end:

- Nonfarm labour productivity was roughly as expected in the preliminary Q2 release, falling -4.6% Q/Q saar after -7.4% as output fell -2.1%

- With hourly compensation jumping 5.7% (but -4.4% in real terms), ULCs saw a smaller moderation than expected from 12.7% to 10.8% (cons 9.5%).

- Tsy Auction: Muted react after $42B 3Y note auction (91282CFE6) small stop-through: 3.202% high yield vs. 3.205% WI; 2.50x bid-to-cover vs. 2.43x last month.

- Indirect take-up climbed to 63.08% vs. 60.37% prior; direct bidder take-up at 17.28 vs. last month's 19.35%; primary dealer take-up 19.64% vs. 20.28%.

- Cross asset update: Stocks off modest lows (SPX eminis at 4126.75 -15.00); Spot Gold firmer +6.58 at 1795.54; Crude near steady (WTI +0.04 at 90.80).

- Currently, 2-Yr yield is up 7.9bps at 3.2841%, 5-Yr is up 7.4bps at 2.9797%, 10-Yr is up 4bps at 2.7974%, and 30-Yr is up 2.1bps at 3.0057%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00071 to 2.31800% (+0.00600/wk)

- 1M -0.00843 to 2.38014% (+0.01071/wk)

- 3M +0.00943 to 2.92100% (+0.05429/wk) * / **

- 6M -0.01843 to 3.55043% (+0.12486/wk)

- 12M -0.00385 to 3.99086% (+0.13100/wk)

- * Record Low 0.11413% on 9/12/21; ** New 24Y high: 2.91157% on 8/8/22

- Daily Effective Fed Funds Rate: 2.33% volume: $89B

- Daily Overnight Bank Funding Rate: 2.32% volume: $279B

- Secured Overnight Financing Rate (SOFR): 2.28%, $950B

- Broad General Collateral Rate (BGCR): 2.26%, $387B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $380B

- (rate, volume levels reflect prior session)

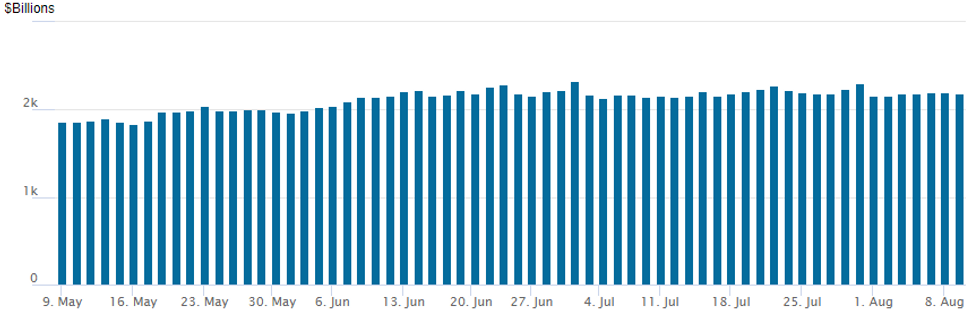

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,186.568B w/ 95 counterparties vs. $2,195.692B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Rate hike insurance buying via SOFR and Eurodollar puts continued Tuesday, supporting low-delta volatility vs. slightly lower at-the-money vol (lack of real vol on range in underlying) in the lead up to Wednesday's July CPI read (0.2% est, 1.3% prior); YoY (8.7% est, 9.1% prior).- Salient trade listed below includes buying of March and June expiry SOFR put flys, Dec Eurodollar put spreads and outright puts:

- Block, 3,000 SFRQ2 96.75/96.87 put spds 1.5 over 96.93 calls

- +7,500 SFRM3 95.00/95.50/96.00 put flys at 5.5 WITH

- +7,500 SFRZ3 95.00/95.50/96.00 put flys at 4.0

- another +22,500 SFRM3 95.00/95.50/96.00 put flys blocked at 5.5

- Block, 4,000 SFRH3 96.50/96.75 call spds, 9.5 vs. 96.365/0.08%

- +2,000 SFRZ2 96.18/96.31 2x1 put spds, 2 ref 96.42

- 9,700 SFRZ2 95.50/95.75 put spds

- +20,000 Dec 95.50 puts 10.0 vs. 96.035/0.25%

- -10,000 Mar/Jun 96.12/96.50 put spd strip, 40.5 ref 96.085/96.24

- 20,750 Dec 98.75/99.75 put spds

- 3,500 Dec 99.25/99.37 put spds

- 17,000 Green Dec 97.75/98.25 call spds

- 3,000 TYU 116/117 put spds

- 2,250 TYU 122/123 1x2 call spds

- 3,000 wk2 TY 119.5/119.75 put over risk reversals, 1

- 3,000 wk2 TY 119 puts, 19

- 13,300 TYU 120.5 calls, 32

- 2,500 TYU 119 puts, 36

EGBs-GILTS CASH CLOSE: Greece Underperforms Again

Gilts and Bunds weakened Tuesday, with the German curve bear steepening and the belly underperforming in the UK.

- No major data or ECB speakers Tuesday, with the most notable morning event being BoE's Ramsden telling Reuters that the BoE would sell Gilts even if it were to cut rates in future.

- Gilts briefly gained in late afternoon on a Bloomberg sources piece pointing to UK gov't plans for potential power cuts in January in a "reasonable worst-case scenario", but the move quickly faded and Gilts reversed to session lows.

- GGBs underperformed yet again, with a wiretap scandal continuing to pose political uncertainty.

- Otherwise very thin trading volumes, with all attention on Wednesday's US inflation report.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 5-Yr yield is up 1.9bps at 0.688%, 10-Yr is up 2.2bps at 0.921%, and 30-Yr is up 3.6bps at 1.154%.

- UK: The 2-Yr yield is up 2.9bps at 1.927%, 5-Yr is up 3.9bps at 1.82%, 10-Yr is up 1.9bps at 1.971%, and 30-Yr is down 0.7bps at 2.345%.

- Italian BTP spread down 0.5bps at 214bps / Greek up 10.1bps at 228.3bps

EGB Options: Schatz Unwind, Bund P/S Buying

Tuesday's Europe rates / bond options flow included:

- RXU2 155.5/153.5 1x2 put spread bought for 2 in 1k

- DUU2 110.70/110.90cs vs 110.00/109.80ps, sold the ps at 10 in 5k

FOREX: Initial Euro Strength Reverses, G10 Ranges Contained

- Currency markets traded in a subdued manner on Tuesday, with major pairs contained to narrow ranges ahead of the US inflation data tomorrow.

- There was some early Euro strength throughout the European session which saw EURUSD rise around 50 pips from 1.02 to a 1.0247 high and notably back above pre-NFP levels ~1.0230. The single currency bid helped the likes of EURAUD reverse a solid portion of the prior day’s retreat.

- This price action initially kept the USD index on the back foot for much of the session, however, a slow grind lower across major equity indices bolstered the greenback, with the DXY eventually turning positive nearing the APAC crossover. This led EURUSD back to levels just above the 1.0200 mark with the pair settling in the middle of its 1.0100-1.0300 range which it has respected for the past 16 trading days.

- AUDUSD (-0.49%) is the notable laggard, however, price action remains well within the bounds of Monday’s range. Very tentative price action in USDJPY, trading blows either side of the 135.00 mark and registering a significantly smaller 52-pip range on the day.

- The obvious potential catalyst for renewed currency volatility on Wednesday lies in the form of US inflation data at 1330BST/0830ET. Consensus shows headline CPI easing to +0.2% M/m from an unwind in energy prices, whilst core CPI is seen slowing from 0.7% to 0.5% M/m following three sizeable consecutive beats.

- There will also be Chinese CPI/PPI data released during the APAC session overnight.

FX: Expiries for Aug10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0100(E874mln), $1.0168-75(E1.7bln), $1.0210(E1.2bln), $1.0215-20(E752mln), $1.0400(E1.4bln)

- USD/JPY: Y133.90-05($1.4bln)

- GBP/USD: $1.2040-50(Gbp528mln), $1.2400(Gbp690mln)

- AUD/USD: $0.6985-00(A$794mln)

- USD/CAD: C$1.2900($1.1bln)

- USD/CNY: Cny6.7500($732mln)

Late Equity Roundup: Buffet Ups Occidental Holdings to 20%

Stock indexes held mildly weaker after the FI close, tech-stocks continued to underperform after Micron warning "expect significant sequential declines in revenue and margins”, consumer discretionary sector weaker due to durables and autos underperforming while energy share outperformed.

- Selling remained cautious ahead Wed's key CPI data (0.2% MoM est vs. 1.3% prior, 8.7% YoY vs. 9.1% prior). Currently, SPX eminis trades --18.0 (-0.43%) at 4124; DJIA -51.2 (-0.16%) at 32781.63; Nasdaq -144.2 (-1.1%) at 12500.63

- SPX leading/lagging sectors: Energy sector remains strong (+1.51%) lead by Occidental Petroleum (OXY) +3.9% after report Warren Buffet increased his holdings to 20%, Marathon (MPC) +2.98%, Valero Energy (VLO) +2.90%; Utilities (+1.1%) followed by Real Estate (+0.53%). Laggers: As noted Consumer Discretionary (-1.50%), Information Technology (-0.91%) followed by Communication Services (-0.66%) w/ media and entertainment lagging.

- Dow Industrials Leaders/Laggers: United Health (UNH) +4.29 at 540.89, McDonalds (MCD) +2.53 at 259.33, Travelers (TRV) +2.29 at 162.27, Chevron (CVX) +1.32 at 154.84. Laggers: Salesforce.com (CRM) -8.19 at 181.46, Home Depot (HD) -6.89 at 305.08, Nike (NKE) -4.00 at 110.00.

E-MINI S&P (U2): Consolidating

- RES 4: 4345.75 2.00 proj of the Jun 17 - 28 - Jul 14 price swing

- RES 3: 4306.50 High May 4

- RES 2: 4204.75 High May 31 and a key resistance

- RES 1: 4188.00 High Aug 8

- PRICE: 4130.50 @ 14:23 BST Aug 9

- SUP 1: 4003.69/3913.25 50-day EMA / Low Jul 26 and a key support

- SUP 2: 3820.25 Low Jul 18

- SUP 3: 3723.75 Low Jul 14

- SUP 4: 3639.00 Low Jun 17 and a bear trigger

S&P E-Minis are consolidating. Short-term trend conditions remain bullish though and the contract traded higher Monday. Continued gains would confirm a resumption of the current bull cycle and maintain the positive price sequence of higher highs and higher lows. The focus is on 4204.75 next, May 31 high and the next key resistance. On the downside, initial trend support is at 3913.25, the Jul 26 low. The 50-day EMA intersects at 4003.69.

COMMODITIES: Mixed Day For Crude As Gold Hits 6-Week High Ahead of US CPI

- Crude oil has had a mixed session to currently sit almost unchanged. Russia’s Transneft has confirmed the suspension of oil flows to the EU via the southern leg of the Druzhba pipeline (through Ukraine to Hungary, Slovakia & Czech Rep) with currently no effect on the northern leg (via Belarus to Poland and Germany).

- EIA short-term forecasts for the US to consume slightly less gasoline this year than previously thought (8.83mbpd vs 8.84) even if total demand will still top 2021 levels.

- WTI is +0.08% at $90.83 having touched a high of $92.65 but still not troubling resistance at $95.10 (20-day EMA). Last week’s bearish price action has reinforced a vulnerable theme, with support seen at $87.01 (Aug 5 low).

- By far the most active strikes in CLU2 contracts today have been $015/bbl and $106/bbl calls.

- Brent is +0.04% at $96.69, off an earlier high of $98.40 having come closer to testing the 20-day EMA at $99.92, moving further away from support at $92.78 (Aug 5 low).

- Gold is +0.3% at $1794.38 having earlier touched a six week high of $1800.46, fairly well despite rising Tsy yields ahead of tomorrow’s US CPI report. In doing so it clears both resistance at both $1795.0 (Aug 4/5 high) and trendline of $1797.1 (drawn from Mar 8 high), opening $1825.1 (Jun 30 high).

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/08/2022 | 0600/0800 | * |  | NO | CPI Norway |

| 10/08/2022 | 0600/0800 | *** |  | DE | HICP (f) |

| 10/08/2022 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 10/08/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 10/08/2022 | 1230/0830 | *** | | US | CPI |

| 10/08/2022 | 1400/1000 | ** | | US | Wholesale Trade |

| 10/08/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 10/08/2022 | 1500/1100 | | US | Chicago Fed's Charles Evans | |

| 10/08/2022 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 10/08/2022 | 1800/1400 | ** | | US | Treasury Budget |

| 10/08/2022 | 1800/1400 | | US | Minneapolis Fed's Neel Kashkari |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.