Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- US Tsy 10Y Yield taps 3.5158%, highest level since April 2011

- France FM: Window Closing For Iran To Revive Nuclear Deal

- Democrats are seeking an additional USD$12 billion for Ukraine

- 7.5 MAG. EARTHQUAKE 46 KM SSE OF LA PLACITA DE MORELOS MEXICO, bbg

- TSUNAMI POSSIBLE AFTER EARTHQUAKE OF 7.5 STRIKES NEAR THE COAST OF MICHOACAN MEXICO- U.S. TSUNAMI WARNING SYSTEM- Reuters

US TSYS: Relative Calm Ahead Flood of Central Bank Policy Annc's

Tsys holding mostly weaker after the bell (Dec Ultra-Bond outperforming), Inside session range after Tsy yields tapped multi-year highs: 2s at 3.9655% high; 5s at 3.7124%; 10s at 3.5158% high; 30Y at 3.5679%).

- Relative calm before a flood of central bank rate anncs lead by the FOMC (Wed) and BoE (Thu), followed by Riksbank, Canada, China on Tue; Boj, SNB, Norges on Thu. Light volumes (TYZ2 <850k w/ Japan out for one day holiday (Respect for the aged) and London banks closed for the Queen's funeral.

- No obvious headline or block driver as futures bounced off morning lows, long end outperforming as curves extended inversion (2s10s currently -4.008 at -46.407 vs. -48.142 low; 5s30s -6.037 at -18.340 vs. -19.977 low).

- Plausible driver: carry-over curve flattening/steepener unwinds from deep pocket accts firm up opinion on forward policy/recession chances ahead Wednesday's FOMC (includes Summary of Economic Projections, Fed Chairman Powell news conf 30 minutes after the 1400ET annc); 75bp hike widely anticipated, option trades seeing unwind of 100bps hike bets, while debate over 50-75bps moves in Nov and Dec meetings continues.

- Current cross-asset levels: Stocks gaining late - modest relief rally as bets on 100bp hike this Wed receded, SPX extending session highs w/ESZ2 at 3916.25 (+26.25), Crude mildly higher - well off lows (WTI +0.30 at 85.41 vs. 82.15 low), Gold weaker (1673.21 -1.85).

- The 2-Yr yield is up 7.7bps at 3.9443%, 5-Yr is up 5.7bps at 3.6876%, 10-Yr is up 3.5bps at 3.4846%, and 30-Yr is down 1bps at 3.5032%.

SHORT TERM RATES

US DOLLAR LIBOR: No new settles Monday due to London bank closure for Queen's funeral. Last Friday's sets' and total change on the week:

- O/N -0.00543 to 2.31557% (+0.00100 total last wk)

- 1M +0.02043 to 3.01386% (+0.24072 total last wk)

- 3M +0.03815 to 3.56529% (+0.31986 total last wk) * / **

- 6M +0.06029 to 4.12329% (+0.31215 total last wk)

- 12M +0.05071 to 4.67214% (+0.48314 total last wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 3.56529% on 9/16/22

- Daily Effective Fed Funds Rate: 2.33% volume: $96B

- Daily Overnight Bank Funding Rate: 2.32% volume: $294B

- Secured Overnight Financing Rate (SOFR): 2.27%, $952B

- Broad General Collateral Rate (BGCR): 2.26%, $392B

- Tri-Party General Collateral Rate (TGCR): 2.26%, $376B

- (rate, volume levels reflect prior session)

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usages climbs to $2,217.542B w/ 101 counterparties vs. $2,186.833B prior session. Record high still stands at $2,329.743B from Thursday June 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Mostly puts on modest volume Monday appeared consolidative with accounts unwinding some rate hike insurance positions ahead Wednesday's FOMC policy annc., some light call trade reported as specs looked to fade chances of more aggressive rate hikes in November or December. Wed's FOMC (includes Summary of Economic Projections, Fed Chairman Powell news conf 30 minutes after the 1400ET annc).- SOFR Options:

- Block, 8,000 SFRF3 94.75/95.00 put spds, 3.75 ref 95.56-.565

- Block, 2,500 SFRU3 94.50/95.00/95.50 put flys, 6.5 net/wings over

- Block, +5,000 SFRZ2 95.00/95.37/95.50 broken put trees, 1.5 net ref 95.725

- -10,000 SFRZ3 96.00/96.25 put spds, 13

- 2,000 short Aug 95.50/95.75 put spds vs. 96.75/96.87 call spds

- 4,500 SFRF3 95.00/95.25 put spds ref 95.62

- Eurodollar Options:

- 2,100 Oct 95.56/95.68 call spds ref 95.42

- 1,500 Nov 95.50/95.75 2x1 put spds

- 2,000 Dec 94.75/95.00 put spds ref 95.43

- Treasury Options:

- Block, 10,000 113.5/114.25 put spds, 17

- 10,000 FVX 112 calls, 4.5 ref 108-29.75

- 5,000 FVX 108.5 puts, 37.5 ref 109-00

- 2,300 TYV 114/114.5 put spds, 15

- 7,100 TYV 115.5 calls, 9 ref 114-11.5

- 5,000 USZ 122-126 put spds, ref 130-17

- 6,000 FVZ 110.5 calls 30-30.5 ref 108-30.75 to -31

- 15,600 TYX 112 puts, 24-26 ref 114-13.5 to -10.5

- 3,800 FVX 108 puts, 24.5

- 10,000 TYX 112.5 puts, 30

- 3,000 TYX 111/113 put spds

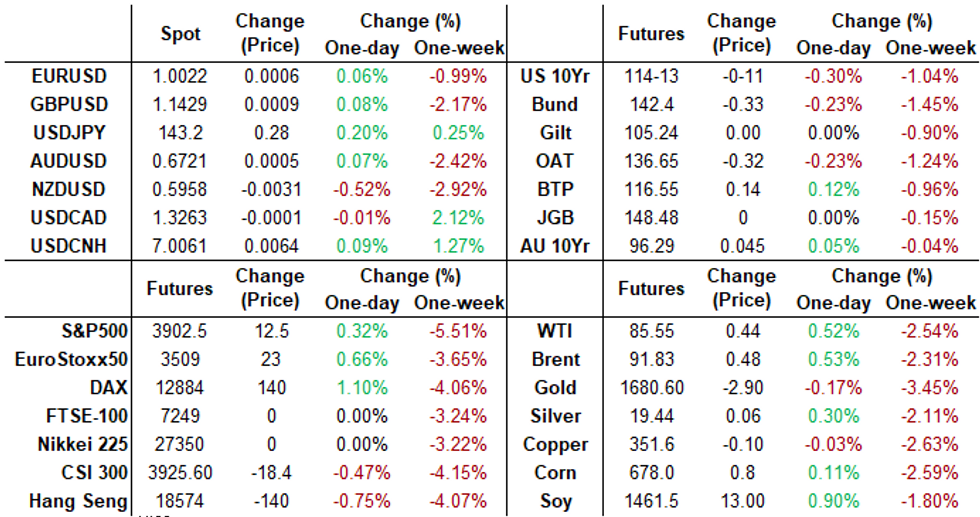

FOREX: Risk Recovery Sees Greenback Pare Earlier Gains

- The greenback had started the week as the best performing G10 currency as risk sentiment soured from the open and equities extended below last week’s lows. However, Monday’s session turned out to be a tale of two halves, with a solid bounce in both equities and oil prices weighing on the greenback throughout the US session, culminating in the USD index trading close to unchanged from Friday’s close.

- With no direct headlines driving the price action, markets may have overextended given the holidays in the UK and Japan, with potential profit taking dynamics coming into play ahead of the FOMC decision on Wednesday.

- NZDUSD has underperformed, following momentum selling below the psychological 0.60 handle. The pair continues to print fresh cycle lows (0.5930), the worst levels since May 2020.

- Additionally, USDCAD extended on last week’s strength which resulted in a break of key resistance and the bull trigger. This confirmed a resumption of the broader uptrend and saw the pair get as high as 1.3344 on Monday. Despite this bullish price action, the pair has had the most significant turnaround, closing the gap with the overnight lows at 1.3250 and narrowing in on the initial recent breakout level at 1.3224, the Jul 14 high.

- Japan returns on Tuesday and National Core CPI data is on the docket. Following this markets will receive the latest RBA Monetary Policy Meeting Minutes. Canadian August CPI highlights Tuesday’s North American session with US building permits a minor data point. Potential comments from ECB’s Lagarde due to speak at an event hosted by the Frankfurt Society for Trade, Industry, and Science.

- Focus then turns firmly to a slew of DM and EM central bank decisions/projections, headlined by the Federal Reserve on Wednesday.

FX: Expiries for Sep20 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9800(E1.5bln), $1.0000(E654mln), $1.0050(E546mln), $1.0100(E632mln)

- GBP/USD: $1.1425(Gbp647mln)

- EUR/JPY: Y138.00(E626mln)

- AUD/USD: $0.6719-25(A$580mln)

Late Equity Roundup: Late Bid, Materials, Industrials Gaining

Stock indexes gaining in late FI trade, looking to test midmorning highs w/ Materials and Industrial sectors outperforming. Currently, SPX eminis trade +6.75 (0.17%) at 3896.25; DJIA +40.31 (0.13%) at 30859.88; Nasdaq +31.7 (0.3%) at 11478.42.

- SPX leading/lagging sectors: Rebounding from Fri's lows, Materials (+0.97%) and Industrials (+0.67%) sectors outperformed, the latter lead by transportation shares w/ airlines outpacing air freight and logistics, road and rail. Laggers: As noted, Health Care underperforming (-1.31%) w/ pharmaceutical names weighing: Moderna (MRNA) -9.13%; Real Estate (-0.89%) and Communication Services (-0.20%) follow.

- Dow Industrials Leaders/Laggers: Home Depot (HD) +2.38 at 278.35, Apple (AAPL) +2.21 at 152.91, Nike (NKE) +2.08 at 106.20. Laggers: Amgen (AMGN) -2.36 at 228.78, JNJ -2.35 at 165.25 and Merck (MRK) -1.62 at 86.0.

E-MINI S&P (Z2): Bearish Outlook

- RES 4: 4345.75 High Aug 16 and a bull trigger

- RES 3: 4313.50 High Aug 18

- RES 2: 4234.25 High Aug 26

- RES 1: 4027.08/4175.00/47 20-day EMA / High Sep 13

- PRICE: 3864.50 @ 14:39 BST Sep 19

- SUP 1: 3846.25 Intraday low

- SUP 2: 3819.54 76.4% retracement of the Jun 17 Aug 16 bull leg

- SUP 3: 3741.75 Low Jul 14

- SUP 4: 3657.00 Low Jun 17 and a major support

S&P E-Minis remains soft and the contract has traded lower today, extending the reversal from last Tuesday’s high of 4175.00. Price has recently cleared key short-term support at 3900.00, the Sep 7 low. This confirms a resumption of the bear cycle that started mid-August and paves the way for a move towards 3819.54, a Fibonacci retracement. Key short-term resistance has been defined at 4175.00, the Sep 13 high.

COMMODITIES

- WTI Crude Oil (front-month) up $0.54 (0.63%) at $85.65

- Gold is down $2.27 (-0.14%) at $1672.78

Tuesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/09/2022 | 2330/0830 |  | JP | Natl CPI | |

| 20/09/2022 | 0115/0915 |  | CN | PBoC Rate Decision | |

| 20/09/2022 | 0600/0800 | ** |  | DE | PPI |

| 20/09/2022 | 0730/0930 | ** |  | SE | Riksbank Interest Rate |

| 20/09/2022 | 0800/1000 | ** |  | EU | EZ Current Acc |

| 20/09/2022 | 1230/0830 | *** |  | CA | CPI |

| 20/09/2022 | 1230/0830 | *** |  | US | Housing Starts |

| 20/09/2022 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 20/09/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 20/09/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 20/09/2022 | 1700/1900 | | EU | ECB Lagarde Lecture in Frankfurt | |

| 20/09/2022 | 1930/1530 | | CA | BOC Deputy Beaudry speech "Pandemic macroeconomics: What we’ve learned, and what may lie ahead." |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.