Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- SECURITY: US Applies Fresh Sanctions On Iran, Prospect Of Nuclear Deal Remote

- FED'S EVANS: POLICYMAKERS see 125 BPS OF RATE HIKES OVER NEXT TWO MEETINGS, Rtrs

- BOC: MORE RATE HIKES NEEDED, TOO SOON FOR BALANCED STANCE

- UK-FRANCE: Truss And Macron Agree To UK-France Summit In 2023

- NEC Director Brian Deese: WH Looking At Additional SPR Releases

US TSYS: Liquidity Challenged Ahead Sep NFP

Tsy futures weaker but off midmorning lows after the close where 10YY tapped 3.8418% high, 30YY 3.8140% high, before paring move into midday, initial impetus tied to sympathy move with sell-off in EGBs, particularly longer Gilts apparently as mkt expresses dissatisfaction with poorly researched/planned buy scheme introduced last week.

- Off-sides positioning hampered by low liquidity ahead Friday's September NFP (+250k est vs. +315k prior; wide dealer range from +200k low to JPM high at +389k)

- Sell-stops triggered on the way down while couple Dec'22 10Y future block sales (over 11k total) contributed to higher yields as did hawkish tones from Fed speakers (MN Fed Kashkari: high bar to change Fed's current path of higher rates to combat inflation).

- The 2-Yr yield is up 8.7bps at 4.235%, 5-Yr is up 8bps at 4.0462%, 10-Yr is up 6.3bps at 3.8155%, and 30-Yr is up 3.6bps at 3.7896%.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00228 to 3.05871% (-0.00643/wk)

- 1M +0.10215 to 3.30029% (+0.15758/wk)

- 3M +0.04171 to 3.82571% (+0.07100/wk) * / **

- 6M +0.02386 to 4.30757% (+0.07557/wk)

- 12M +0.05971 to 4.88471% (+0.10414/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 3.75471% on 9/30/22

- Daily Effective Fed Funds Rate: 3.08% volume: $104B

- Daily Overnight Bank Funding Rate: 3.07% volume: $281B

- Secured Overnight Financing Rate (SOFR): 3.04%, $992B

- Broad General Collateral Rate (BGCR): 3.00%, $397B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $366B

- (rate, volume levels reflect prior session)

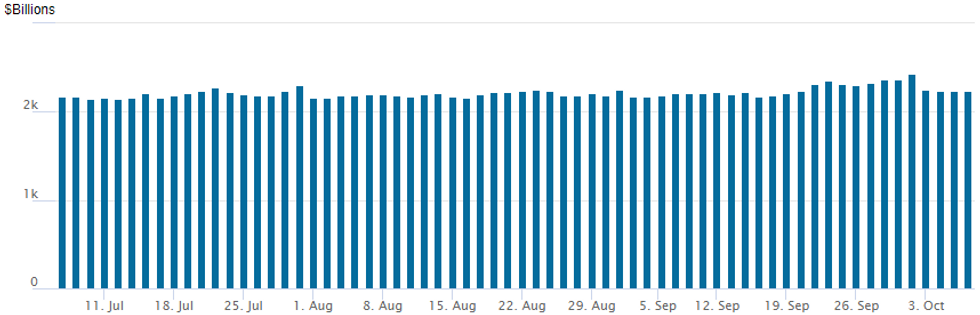

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbed to $2,232.801B w/ 101 counterparties vs. $2,230.799B in the prior session. Recent record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Much better put and put spread buying Thursday, focus on hedging tighter policy and effect on underlying futures. Salient trade, ongoing Green Dec'24 SOFR 93.50/94.00/94.50 put flys at 2.5 - adds to appr +33k late last week, same price. Green Dec SOFR futures currently trade 96.345. Other highlight trade in current session:- SOFR Options:

- Block, 2,500 SFRZ4 93.50/94.00/94.50 put flys, 2.5

- Block, 2,500 SFRM4 99.50/100 1x2 call spds

- Block, +10,000 SFRX2 95.25/95.62/95.75 put trees, 6.0

- Block, +5,000 short Mar SOFR 98.50/99.00 call spds, 1.0

- 4,100 SFRV2 96.12 calls, .75

- Eurodollar Options:

- 4,500 Mar 94.50/94.75/95.00 put trees vs. Mar 95.25/95.62/96.00 call trees

- Treasury Options:

- 2,271 TYX 112.5/114/115.5 call flys

- 2,500 FVZ 107.5 straddles

- +3,000 TYZ2 116 calls, 24 ref 112-05

- 5,000 FVX2 108/108.25/108.75 broken put flys, 16.5

- -5,000 FVX 105.75/106.75 put spds, 12

- Block, +10,000 FVZ2 106/107.25 put spds put spds, 27.5

- Block, 7,500 TYX2 109.5/111.5 put spds, 28 ref 112-12.5

- 2,500 TYZ2 112.5 puts, 138

- Block, 7,500 TYX2 109/112 put spds, 38 ref 112-11.5

- Block, 7,500 TYZ2 110/111.5 put spds, 54 ref 112-10.5

- Block, 3,750 FVZ2 107.25 puts, 50.5 ref 107-24.25

EGB Options: Massive Schatz Call Buying Features Thursday

Thursday's Europe rates / bond options flow included:

- DUZ2 109 calls bought from 5.5-6.5 in 50k

- DUZ2 109.00/110.00 call spread bought for 5.5 in 15k

- DUZ2 108/109/110 call fly bought for 9 in 2k

- RXX2 131/129ps, sold at 4.5 in 4k

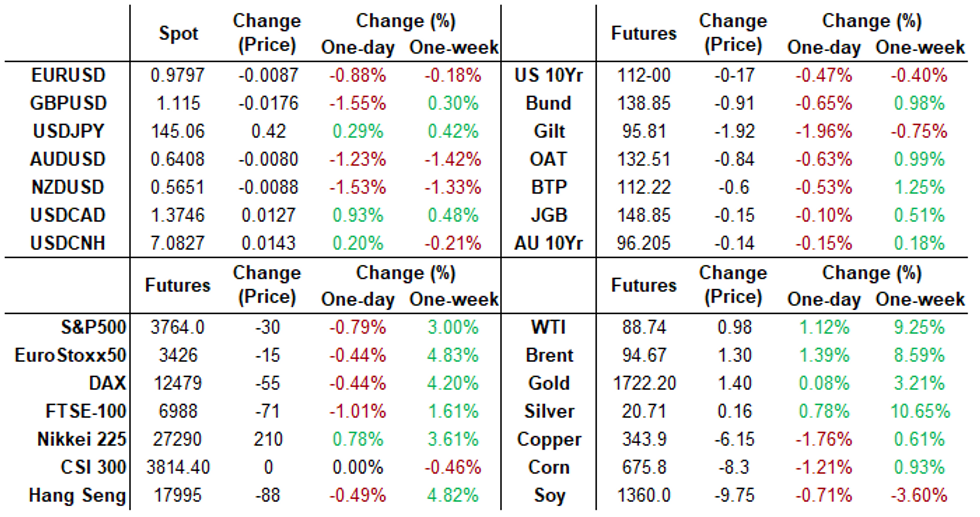

FOREX: Greenback Extends Recovery, DXY Rises 0.95% Ahead Of NFP

- Renewed greenback strength gathered momentum throughout Thursday’s trading session, with the USD index (+0.85%) extending its recovery, rising through yesterday’s high and then above Fibonacci resistance at 111.86.

- The broad dollar strength has seen the Euro dip back below $0.98 and the weakness in equities has heavily weighed on the likes of AUD and NZD, both down roughly 1.5%.

- GBPUSD (-1.55%) is the poorest performer, briefly printing at 1.1114, nearly 400 pips from Wednesday’s peak. Initial firm support is seen at 1.1025, the Sep 30 low.

- Rising at a much slower pace (potentially amid lingering MOF concerns) is USDJPY, however the pair is now inching above Y145, narrowing the gap with the post intervention highs at 145.30. The primary uptrend remains intact and sights are on the bull trigger at 145.90, Sep 22 high.

- Weakness in equities is underpinning the greenback approaching the APAC crossover. The week’s early optimism for major indices has been dissipating as markets await Friday’s US employment report for further signals on the health of the US economy/Fed policy.

- Consensus sees NFP growth moderating to 260k in Sept after the 315k from August’s ‘goldilocks’ report. Canadian jobs data will be released in conjunction with the US data.

FX Expiries for Oct07 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9730-38(E1.1bln), $0.9750(E695mln), $0.9775(E506mln), $0.9800(E1.6bln), $0.9845-55(E1.8bln), $0.9900-02(E1.8bln), $0.9915-25(E1.8bln), $0.9941-55(E1.2bln), $1.0100(E2.0bln)

- GBP/USD: $1.0923(Gbp668mln), $1.1300(Gbp544mln), $1.1400(Gbp572mln)

- EUR/GBP: Gbp0.8690-00(E1.1bln)

- USD/CAD: C$1.3885-00($1.1bln)

- USD/CNY: Cny6.80($2.4bln), Cny7.09($600mln)

Late Equity Roundup, Under Pressure

Stock indexes trading weaker into the close, near second half lows, Real Estate, Utilities underperforming. Currently, SPX eminis trade -31 points (-0.82%) at 3763; DJIA -317.17 (-1.05%) at 29955.5; Nasdaq -56.4 (-0.5%) at 11092.63.

- SPX leading/lagging sectors: Energy sector shares outperforming (+1.82%), equipment and servicer makers outpacing oil/gas names. Communication Services (-0.64%) and Information Technology (-0.79%) next up, semiconductors outpacing hardware makers, software and services. Laggers: As noted Real Estate (-3.28%) and Utilities (-3.23%) underperforming, specialized, health care and industrial REITS weighing on the former.

- Dow Industrials Leaders/Laggers: Chevron (CVX) +2.73 at 161.26, Home Depot (HD) +0.91 at 290.76, Caterpillar (CAT) +0.79 at 179.17. Laggers: United Health (UNH) -6.63 at 520.44, Goldman Sachs (GS) -4.65 at 304.35, McDonalds (MCD) -4.40 at 234.69.

COMMODITIES: Oil Continues To Edge Out Gains With OPEC+ Fallout

- Crude oil ekes out further, more modest gains after yesterday’s OPEC+ decision to cut output by 2mbpd starting in Nov, despite the US continuing to voice opposition, latest from WH econ adviser Deese with it “unnecessary and unwarranted” and the WH still considering the SPR among other options.

- WTI is +0.9% at $88.56 and moves closer to $89.99 (Sep 6 high) having cleared the 50-day EMA.

- Price gains are more limited for front contracts, potentially on the chance of additional SPR release, whilst most active strikes in CLX2 today have been $80/bbl puts.

- Brent is +1.2% at $94.46 and moves closer to $95.54 (Sep 5 high) having cleared the 50-day EMA.

- Gold is -0.16% at $1713.48, in a relatively narrow despite emerging USD strength on through the session. Resistance remains at $1729.5 (Oct 4 high) with support at $1695.2 (former trendline resistance).

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/10/2022 | 2301/0001 | ** |  | UK | IHS Markit/REC Jobs Report |

| 07/10/2022 | 0545/0745 | ** |  | CH | Unemployment |

| 07/10/2022 | 0600/0800 | ** |  | DE | Industrial Production |

| 07/10/2022 | 0600/0800 | ** | | DE | Retail Sales |

| 07/10/2022 | 0600/0800 | ** | | DE | Import/Export Prices |

| 07/10/2022 | 0600/0800 | ** |  | NO | Norway GDP |

| 07/10/2022 | 0645/0845 | * |  | FR | Current Account |

| 07/10/2022 | 0645/0845 | * | | FR | Foreign Trade |

| 07/10/2022 | 0800/1000 |  | EU | ECB Consumer Expectations Survey Results - August | |

| 07/10/2022 | 0800/1000 | * |  | IT | Retail Sales |

| 07/10/2022 | 1025/1125 | | UK | BOE Ramsden Speech at Securities Industry Conference | |

| 07/10/2022 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 07/10/2022 | 1230/0830 | *** |  | US | Employment Report |

| 07/10/2022 | 1400/1000 | | US | New York Fed's John Williams | |

| 07/10/2022 | 1500/1100 | | US | Minneapolis Fed's Neel Kashkari | |

| 07/10/2022 | 1900/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.