Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

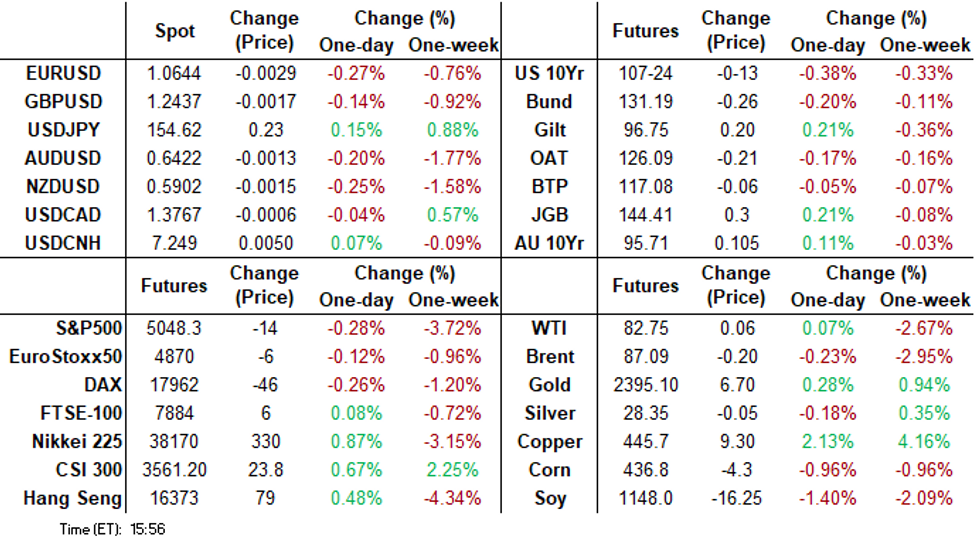

- Treasuries finish moderately lower Thursday, reacting negatively to normal policy comments from NY Fed Williams.

- New York Fed President Williams discussed the potential for a data driven rate hike in the future.

- The Fed can take its time and let well-positioned monetary policy work Williams added.

US TSYS Near Lows, Possibly Overreacting to NY Fed Williams

- Treasury futures are moderately weaker after the bell, near session lows as markets gradually price out dovish policy projections for the year. Treasuries reacted negatively to comments from NY Fed Williams on the potential for a data driven rate hike in the future. Markets may have overreacted while Williams simply stated the Fed can take its time and let well-positioned monetary policy work and let the economy continue to rebalance.

- On earlier data, moderate action followed slightly lower than expected weekly claims (212k vs. 215k est, prior up-revised to 212k from 211k) and continuing claims (1.812M vs. 1.818M est, prior down-revised to 1.810M from 1.817M), while Philadelphia Fed Business Outlook came out much higher than estimated (15.5 vs. 2.0 est).

- Rates see-sawed around session lows after drop in Existing Home Sales to 4.19M from 4.38M prior comes out more or less in line with expectations (4.2m) MoM -4.3% from 9.5% prior (-4.1% est), Leading index -0.3% vs -0.1% est (prior up-revised to 0.2% from 0.1%).

- Jun'24 10Y trading 107-24.5 last (-12.5) vs. 107-20.5 low, still inside initial technicals with support at 107-13.5 (Apr 16 low) vs r 108-25.5 resistance (Apr 12 high). 10Y yield 4.5977% +.0104, curves off lows: 2s10s +.491 -34.206.

- Look ahead: no economic data to report Friday while Chicago Fed Goolsbee will participate in a moderated Q&A at a SABEW conference (1030ET) ahead of the Fed blackout late Friday.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00338 to 5.31544 (-0.00385/wk)

- 3M -0.00200 to 5.32456 (-0.00300/wk)

- 6M -0.00176 to 5.29978 (-0.00359/wk)

- 12M -0.00642 to 5.20367 (+0.01739/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.731T

- Broad General Collateral Rate (BGCR): 5.30% (-0.01), volume: $701B

- Tri-Party General Collateral Rate (TGCR): 5.30% (-0.01), volume: $685B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $80B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $243B

FED Reverse Repo Operation

- RRP usage recedes to $433.006B vs. $440.508B yesterday. Compares to $327.066B on Monday -- the lowest level since mid-May 2021 as desks cited Federal tax deadline for the drop.

- Meanwhile, the latest number of counterparties recedes to 75 vs. 89 prior.

SOFR/TEASURY OPTION SUMMARY

Varied trade leaning towards downside positioning after better upside interest the last couple sessions. Of note: +40,000 SFRZ5 93.75/94.25/94.75 put fly, 4.0 net from 0906-0908ET. With the Red Dec SOFR futures contract trading at 95.66 - current policy pricing would need to reverse with the Fed shifting tighter policy heading into late 2025.

Underlying futures at near session lows while projected rate cut pricing continues to cool: May 2024 steady at -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 at -13.6% from -16.2% earlier w/ cumulative rate cut -4bp at 5.288%. July'24 cumulative at 11.6bp from -12.1bp earlier, Sep'24 cumulative -21.6bp from -24.1bp.

- SOFR Options:

- 5,000 SFRZ4 95.25/95.75 1x2 call spds 2.5

- over 5,000 SFRM4 94.81/94.93/95.06/95.25 call condors

- -5,000 SRH5 95.75/96.37 call spds 11 ref 95.235

- -5,000 SRU4 95.50 calls 6.5 vs. 94.87/0.16%

- +5,000 SRU4 94.25/94.37 put spds vs. 94.855/0.05%

- +4,000 SRQ4 94.56/94.68/94.87/95.00 put condors 6.25 ref 94.88

- +5,000 SRM4 95.00/95.25/95.50/95.75 call condors 0.5 ref 94.73

- -4,000 SRV4 95.12 straddles, 52.0 ref 95.06

- +5,000 SRU4 94.37 puts 2.0 ref 94.875

- Block, 5,000 SFRV4 94.25/94.37/94.50/94.62 put condors, 1.25

- 6,000 SFRZ4 94.62/95.00 2x1 put spds, 8.0 ref 95.08

- Block, 5,000 SFRH6 93.75/94.25/94.75 put flys, 3.5

- Block, 40,000 SFRZ5 93.75/94.25/94.75 put fly, 4.0 net from 0906-0908ET

- Block, 8,880 SFRZ4 94.43/94.68 put spds 2.0 over SFRV4 94.37/94.62 put spd ref 95.09

- 4,500 0QK4 95.75 calls, ref 95.465 total volume over 10.4k

- 4,400 SFRM4 94.87/94.93/95.00/95.06 call condors ref 94.735

- Block/screen +17,000 SFRV4/SFRZ4 94.62 put spds, 2.5-3.0

- 2,500 SFRV4/SFRX4 94.37/94.62 put spd spd

- 2,000 SFRK4 94.50/94.75 put spds ref 94.74 to -.735

- +4,500 0QM4 94.87/95.00/95.25 put flys, 4.5

- Treasury Options:

- 10,000 TYK4 109/109.75 1x2 call spds, 1 ref 107-22.5

- +10,000 TYM4 107.5 puts, 53 vs. 107-24/0.44%

- +5,000 TYM4 107 puts, 38

- 8,000 TYK4 109.25 puts vs. 16,000 TYM 107.5 puts

- -6,000 wk3 TY 108 calls, 9 vs. 107-31.5

- -10,000 TYK4 107.5/108.75 put over risk reversals 12 vs. 107-30

- -10,000 TYM4 108 put vs. TYK4 108.75 calls, 48 net combo vs. 108-01.5

- 4,000 TYK4 107 puts, 4 ref 108-07.5

- -15,000 TYM4 105 puts, 7

- 2,000 TYK4 109 calls, 8 ref 108-06.5

EGBs-GILTS CASH CLOSE: Pullback On Multiple Factors

Core FI largely reversed the prior session's gains Thursday, with multiple factors weighing increasingly on Bunds and Gilts as the session went on.

- After largely constructive trade in the European morning session, helped by softer oil/gas prices, stronger-than-expected US manufacturing survey data (Philly Fed) helped kick off global core FI weakness in the afternoon, aided by a bounce in energy prices and hawkish-leaning Fedspeak.

- While ECB speakers maintained broad consensus on a June rate cut, Austria's Holzmann broke from the Governing Council's recent rhetoric by noting that the ECB's rate cut cycle would be restrained if Federal Reserve easing proved limited.

- The German and UK curves leaned bear flatter, with Gilts outperforming Bunds.

- Periphery EGB spreads widened in mid-afternoon before later re-tightening, mirroring moves in equities.

- Early Friday sees UK retail sales data.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 4.2bps at 2.986%, 5-Yr is up 4.2bps at 2.517%, 10-Yr is up 3.7bps at 2.502%, and 30-Yr is up 3.3bps at 2.632%.

- UK: The 2-Yr yield is up 2.5bps at 4.488%, 5-Yr is up 0.7bps at 4.192%, 10-Yr is up 1.4bps at 4.275%, and 30-Yr is up 3bps at 4.724%.

- Italian BTP spread down 1.5bps at 143bps / Spanish down 2bps at 81.8bps

EGB Options: Tending Toward Upside Structures Thursday

Thursday's Europe rates/bond options flow included:

- DUK4 105.30/105.20ps, sold at 2 in 2.65k

- DUM4 105.70/106.00/106.20 broken c fly, bought for 3.5 in 5k

- ERU4 96.75/97.00/97.25c ladder, bought for 1.5 in 10k

- ERZ4 98.00/98.50cs, bought for 1.25 in 2k

- SFIM4 94.95/95.00/95.05c fly, bought for 0.75 in 6k

FOREX Yield Bounce Saves USD From Further Declines

- Currency markets traded rangebound Thursday, with the USD Index respecting the recent range and largely consolidating just below this week's cycle high at 106.517. The session started slowly, with the USD lower, before a bottoming-out of the US yield followed comments from Fed's Williams, who stressed that he sees no urgency in pressing the Fed toward cutting interest rates, and that policy is in a "good place".

- Fed rate cut pricing across 2024 approached a new pullback low through the NY crossover, with just 38bps of easing priced across the calendar year - enough to drag the USD out of negative territory, but stop short of any formative rally.

- USD/JPY mimicked the recovery in yields, but failed to make any material test on next resistance. While the technical trend condition in USD/JPY remains positive, the next phase of strength could be harder to come by without another major shift in Fed policy pricing, as positioning looks stretched and diplomatic blockers to potential intervention appear to peel away.

- CAD outperformed at the margins, fading the overbought condition present earlier in the week. An uptick in oil through the London close aided the recovery, however for now weakness in USD/CAD is deemed corrective. Support is seen at 1.3682 (Apr 12 low) whilst is resistance at 1.3846 (Apr 16 high) before 1.3855 (Nov 10, 2023 high).

- Focus for the Friday session turns to the National CPI release for March, UK retail sales, German PPI and speeches from BoE's Ramsden & Mann, ECB's Nagel and Fed's Goolsbee.

FX Expiries for Apr19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0485-00(E1.4bln), $1.0600(E650mln), $1.0635-45(E1.6bln), $1.0675-85(E691mln)

- USD/JPY: Y155.00($1.7bln)

- AUD/USD: $0.6400-20(A$2.0bln)

- USD/CAD: C$1.3700($1.7bln), C$1.3775($645mln), C$1.3885($979mln)

Late Equities Roundup: IT Shares Weighing, Earnings Resume Late

- Stocks have reversed first half gains and are trading mildly weaker, near late Thursday session lows. Currently, DJIA is down 21.21 points (-0.06%) at 37732.68, S&P E-Minis down 11.75 points (-0.34%) at 5050.5, Nasdaq down 87 points (-0.6%) at 15596.72.

- Laggers: Information Technology and Consumer Discretionary sector shares underperformed in late trade. Information Technology shares weighed by chip and software makers: NXP Semiconductors -3.97%, Autodesk -3.32%, ON Semiconductors -2.93%, Micron -2.91%. Auto makers traded weaker late: Tesla -3.31%, GM -0.68%, Ford -0.30%.

- Leading gainers: Interactive media and entertainment shares continued to buoy Communication Services in late trade: Paramount +2.22% Meta +1.52%, Comcast +1.18%. Meanwhile, Utilities recovered from first half weakness, outpacing Financials in late trade. Water and independent power providers lead gainers: American Water Works +1.22%, American Electric +1.03%, Pinnacle West +1.01%.

- Reminder, corporate earnings expected after the close: Netflix, PPG Industries and Western Alliance Bancorp. On tap early Friday: Fifth Third Bancorp, American Express, Procter & Gamble, Community West Bancorp, Schlumberger and Huntington Bancshares.

E-MINI S&P TECHS: (M4) Retracement Mode

- RES 4: 5400.00 Round number resistance

- RES 3: 5285.00/5333.50 High Apr 10 / 1 and the bull trigger

- RES 2: 5195.21 20-day EMA

- RES 1: 5150.82 50-day EMA

- PRICE: 5050.50 @ 1505 ET Apr 18

- SUP 1: 5038.50 Intraday low

- SUP 2: 5018.00 Low Feb 21

- SUP 3: 4994.25 Low Feb 13

- SUP 4: 4907.57 50.0% retracement of the Oct 27 ‘23 - Apr 1 bull leg

The short-term trend condition in S&P E-Minis is unchanged and remains bearish with price trading closer to this week’s lows. The contract has cleared support at the 50-day EMA, signalling scope for a continuation lower near-term. Sights are on 5018.00, the Feb 21 low, ahead of the 5000.00 handle. Firm resistance is seen at 5195.21, the 20-day EMA. A clear break of the average would signal a possible reversal.

COMMODITIES WTI Struggling for Direction

- WTI has oscillated between small gains and losses during Thursday’s session, as oil struggles for direction following yesterday's climbdown. Crude relinquished some of its geopolitical risk premium due to lower concerns for Middle East supply.

- Israel is unlikely to carry out a strike on Iran until after Passover, according to ABC citing a senior US official.

- WTI May 24 is currently broadly unchanged on the day at $82.7/bbl.

- A bull theme in WTI futures remains intact, although yesterday’s move lower signals the start of a short-term bearish corrective cycle.

- The contract has traded through the 20-day EMA and this signals scope for an extension towards the 50-day EMA, at $81.12. A clear break of the 50-day EMA would signal a stronger bearish theme. On the upside, key resistance and the bull trigger has been defined at $87.67, the Apr 12 high.

- Spot gold rose by 0.9% to $2,381/oz on Thursday, keeping it around 2% below its record high reached last Friday.

- The trend condition remains unchanged and the outlook is still bullish, with the next objective at $2452.5, a Fibonacci projection. Initial firm support is at $2293.4, the 20-day EMA.

- Copper also rose by another 2.1% today to $445.5/lb, its highest since early June 2022, helping the Chilean peso to outperform.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/04/2024 | 2330/0830 | *** |  | JP | CPI |

| 19/04/2024 | 0600/0700 | *** |  | UK | Retail Sales |

| 19/04/2024 | 0600/0800 | ** |  | DE | PPI |

| 19/04/2024 | 1415/1515 | | UK | BoE's Ramsden at Peterson Institute Conference | |

| 19/04/2024 | 1430/1030 |  | US | Chicago Fed's Austan Goolsbee | |

| 19/04/2024 | 1530/1130 | | US | New York Fed's Roberto Perli | |

| 19/04/2024 | 1630/1730 | | UK | BOE's Mann Panelist at Capital Flows Seminar | |

| 19/04/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.