Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- FED SWAPS PRICE IN PEAK POLICY RATE OF 4.85% IN MARCH 2023, Bbg

- US: Treasury Dept To Host Meeting Of Countries Imposing Sanctions On Russia

- US: NSC Kirby: OPEC Nations "Coerced" Intro Oil Production Cut By Saudi Arabia

- UK OFFICIALS ARE WORKING ON A U-TURN FOR TRUSS'S TAX-CUT PLAN - Quickly Denied

- PM Truss can make assurances that there will be no further U-turns on her economic plan

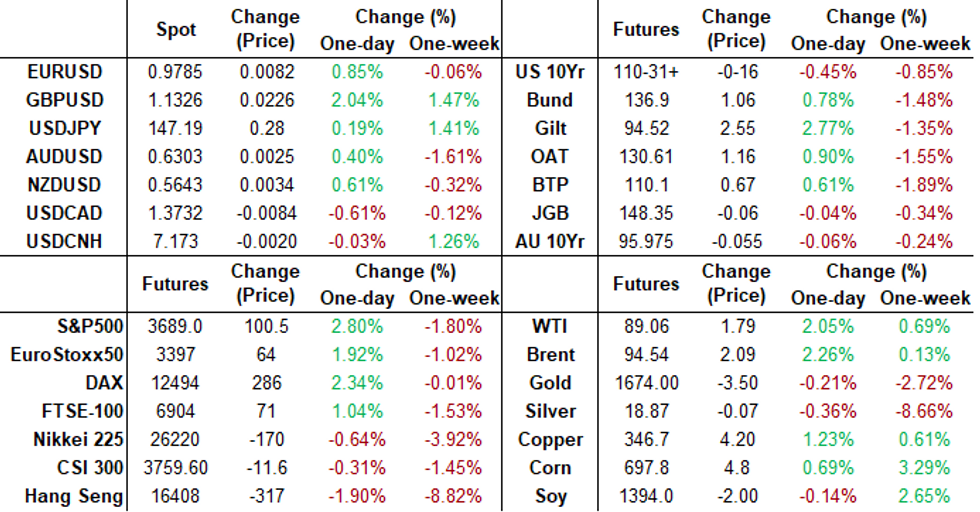

US TSYS: Unexpected Risk Appetite Return After Jump in CPI

Volatile day for rates and equity markets, Tsys weaker again after bonds actually traded higher in late trade -- an unexpected rally in both rates AND equities (SPX tapped 3697.25 high vs. 3503.25 post-data low) after this morning's bounce in CPI inflation measure.- Largely ignoring weekly claims (+9K to 228K; continuing claims +0.003M to 1.368M) Tsys gapped lower following jump in CPI (8.2%, core 6.6%), yield curve bear flattening as prospect of 75bp hike in Nov a lock weighed heavily on the front end.

- Contributing to the rally that coincided w/BOE buy-op, large 10Y Block buy: +14,278 TYZ2 110-21, large buy through 110-16.5 post-time offer at 0957:35ET, 110-24 last (--23.5); appr DV01 $940k.

- Otherwise there did not appear to be any specific headline driver for the surge in risk appetite after the morning data - but more a confluence of acceptable triggers for risk takers: chatter from some traders that CPI seen as peak inflation.

- Another desk pointed out the NY Fed Underlying Inflation Gauge (UIG) was not as stark as the CPI: The UIG "full data set" measure for September is currently estimated at 4.4%, a 0.1 percentage point decrease from the current estimate of the previous month. The "prices-only" measure for September is currently estimated at 6.0%, unchanged from the current estimate for the previous month.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00286 to 3.06171% (-0.01486/wk)

- 1M +0.07343 to 3.41214% (+0.09857/wk)

- 3M +0.06828 to 4.07914% (+0.17357/wk) * / **

- 6M +0.04857 to 4.53857% (+0.15386/wk)

- 12M +0.03829 to 5.10600% (+0.10971/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.07914% on 10/13/22

- Daily Effective Fed Funds Rate: 3.08% volume: $110B

- Daily Overnight Bank Funding Rate: 3.07% volume: $287B

- Secured Overnight Financing Rate (SOFR): 3.04%, $972B

- Broad General Collateral Rate (BGCR): 3.00%, $390B

- Tri-Party General Collateral Rate (TGCR): 3.00%, $371B

- (rate, volume levels reflect prior session)

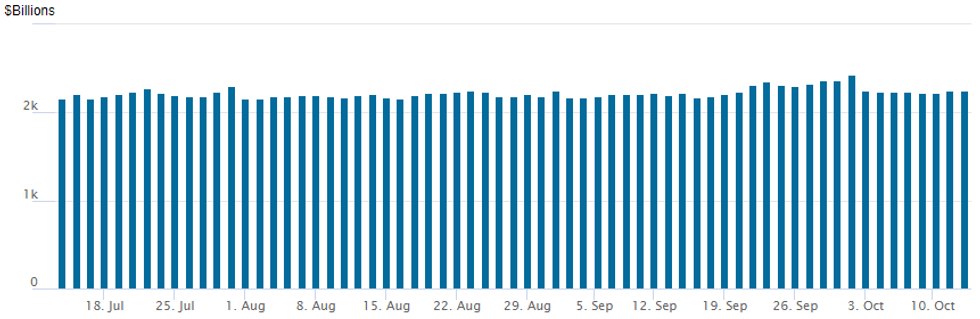

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,244.102B w/ 102 counterparties vs. $2,247.206B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

- SOFR Options:

- Block, 20,000 SFRX2 95.50/95.62/95.75 put trees, 5.75

- Block, 10,000 SFRH3 94.75/95.00/95.25 put flys, 3.5

- Block, 4,000 SFRF3 94.50/94.75 put spds, 5.0 ref 95.175

- Block, 10,000 SFRM3 95.25/95.50 put spds, 14.5 vs. 95.16

- Block, total 10,000 SFRH3 94.87/95.00 put spds 2.5 over 95.87/96.12 call spds

- Block, 5,000 SFRZ3 94.50/95.00/95.50 put flys, 6.5 net vs. 95.43/0.05%

- Block, 2,000 SFRU3 96.25/96.50 put spds

- Block, 3,000 SFRU3 96.25/96.75 put spds

- 2,600 SFRZ2 95.37/95.62/95.87 put flys

- 5,000 SFRV2 95.43/95.50 put spds

- 2,000 2QZ2 95.50/96.00 put spds

- 5,000 SFRZ2 95.31/95.56 2x1 put spds

- 6,500 SFRV2 95.31/95.37/95.43 put flys

- 2,000 short Nov 95.25/95.37/95.50 put flys

- 4,000 SFRZ2 95.31 puts

- Eurodollar Options:

- 2,000 Jun 95.00/95.87 put spds

- 1,300 Dec 94.81/95.00/95.25 broken put flys

- Treasury Options:

- 8,500 TUZ 104 calls, 2.5

- over 7,000 TYZ 109 puts on wide range, mostly 53-57

- Block, 10,000 FVZ2 106.25 puts, 55 ref 106-15

- Block, -20,000 FVZ105.75/106.75 put spds, 29 ref 106-08.25

- -15,000 TYX2 108 puts, 9 ref 110-07

- 3,000 TYX2 108 puts

- 2,500 TYZ 116/117/119/126 (yes, 126) call condors

- 3,000 TYX2 113 calls, 12 ref 111-09 to -10.5

- Block, total 10,000 TYX 110 puts, 17-20, more on screen

EGBs-GILTS CASH CLOSE: UK Politics Drive Rally (In Spite Of US CPI)

In another session of large moves, the biggest driver Wednesday was UK politics, eclipsing the impact of another above-expected US CPI print.

- Gilt yields fell to session lows around midday on multiple reports the UK Gov't was set to "U-turn" on its fiscal package (30Y down 72bp from the Weds high at one point). Bunds followed along.

- But EGBs/Gilts sold off sharply (Bunds underperforming Gilts) after US Sept CPI data came in hot.

- Core FI recovered slightly after a large uptake in the BoE inflation-linked Gilt purchase op (the nominal long-dated op saw lighter takeup, no reac).

- Yields finished closer to session lows than highs with flattening in both the German and UK curves. Bonds didn't share in a large rally in global equities / dollar weakness toward the end of the cash session, which had little obvious catalyst.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 8.8bps at 1.915%, 5-Yr is up 2.5bps at 2.076%, 10-Yr is down 3.3bps at 2.281%, and 30-Yr is down 6.2bps at 2.294%.

- UK: The 2-Yr yield is down 21.3bps at 3.804%, 5-Yr is down 22.9bps at 4.244%, 10-Yr is down 23.7bps at 4.199%, and 30-Yr is down 27bps at 4.548%.

- Italian BTP spread down 3.1bps at 239.2bps / Greek down 7bps at 260.2bps

EGB Options: More Bund Downside Pre-US CPI Thursday

Thursday's Europe rates / bond options flow included:

- RXX2 133/132ps, bought for 13 in 1k

- RXX2 132.00/130.00/129.00 broken put fly, bought for 8 in 4k.

- RXX2 141.5/143.5cs, bought for 7.5 and 8 in 5k

- RXX2 139/143 cs bought for 31 in 15k (ref 136.05, 16 del)

- DUZ2 106.9/106.8/106.6p ladder 1x0.5x0.75, sold at flat in 7.5k

- IKZ2 110/107ps vs 115.50/117cs, sold the ps at 51 in 10k

FOREX: Dollar Slips Further With Surging Equities and Sliding Real Yields

- BBDXY is pushed to fresh session lows on a combination of surging equities, with the two moving in inverted lockstep since US CPI.

- US real yields are adding downward pressure to the dollar again after having less impact earlier in the session, with the 10Y stepping back closer to where it was before CPI at 1.57% (-2.3bps on the day) in a significant reversal from highs of 1.74% forty five minutes after the data.

Late Equity Roundup: Posting Highs, Peak Inflation?

Well off post-CPI lows, stock indexes continue to make unexpected gains w/ Energy and Financial sector shares outperforming amid chatter the data was indicative of peak inflation. Currently, SPX eminis trade +90.5 (2.52%) at 3679.25 (vs. 3503.25 low); DJIA +840.65 (2.88%) at 30051.89; Nasdaq +209 (2%) at 10626.26.

- Rebound in stocks as well as Tsys kicked off after better than expected Linker take-up on this morning's first BoE buy-op (Gilt take-up underwhelming). US$ index meanwhile, gapped lower: DXY -1.173 to 112.147 low.

- SPX leading/lagging sectors: Energy (+4.10%) followed by Financials (+3.97%) and Materials (+2.86%). Laggers: Consumer Discretionary (+0.71%) with autos and retailing underperforming, Consumer Staples (+1.47% and Real Estate (+1.84%) sectors following.

- Dow Industrials Leaders/Laggers: Goldman Sachs (GS) adds to yesterday's gains +10.94 at 306.25, McDonalds (MCD) +10.51 at 247.57, United Health (UNH) +9.33 at 509.29. Laggers: Walmart (WMT) +0.38 at 131.55, Nike (NKE) +0.49 at 89.0, Verizon (VZ) +0.56 at 36.24.

COMMODITIES: Oil Brushes Off CPI Beat, Inventory Build

- Crude oil has seen a mixed session, first falling on rampant US CPI as yields spiked before bouncing for solid session gains after a reasonable retracement in yields and the dollar subsequently weakening.

- The increase comes despite a much larger than expected build in US crude inventories in EIA data (9.9mln vs 1.4mln expected).

- Biden says he'll address gasoline prices next week.

- WTI is +2.1% at $89.13 off a low of $85.56 that cleared the 20-day EMA of $86.25 and next open $84.94 (50% retrace of Sep 26 – Oct 10 rally) before the sharp reversal that leaves it closer to prior resistance at $91.35 (Aug 11 high).

- Brent is +2.3% at $94.59 off a low of $91.08 that remained above the 20-day EMA of $90.59 (50% retrace of the same swing) that remains support.

- Gold is -0.35% at $1667.43 having cleared support at $1659.7 (Oct 3 low) before bouncing, opening the bear trigger of $1615.0 (Sep 28 low).

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/10/2022 | 0130/0930 | *** |  | CN | CPI |

| 14/10/2022 | 0130/0930 | *** | | CN | Producer Price Index |

| 14/10/2022 | 0600/0800 | * |  | DE | Wholesale Prices |

| 14/10/2022 | 0645/0845 | *** |  | FR | HICP (f) |

| 14/10/2022 | 0700/0900 | *** |  | ES | HICP (f) |

| 14/10/2022 | 0900/1100 | * |  | EU | Trade Balance |

| 14/10/2022 | - | | EU | ECB Lagarde & Panetta IMF/World Bank Annual Meetings | |

| 14/10/2022 | - | *** | | CN | Trade |

| 14/10/2022 | 1230/0830 | *** |  | US | Retail Sales |

| 14/10/2022 | 1230/0830 | ** | | US | Import/Export Price Index |

| 14/10/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 14/10/2022 | 1300/0900 | * |  | CA | CREA Existing Home Sales |

| 14/10/2022 | 1400/1000 | * | | US | Business Inventories |

| 14/10/2022 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 14/10/2022 | 1400/1000 | | US | Kansas City Fed's Esther George | |

| 14/10/2022 | 1430/1030 | | US | Fed Governor Lisa Cook | |

| 14/10/2022 | 1615/1215 | | US | Fed Governor Christopher Waller |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.