Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI SECURITY: White House: We Will Support Ukraine For As Long As It Takes

- MNI US: Gaetz Indicates He Will Trigger 'Motion To Vacate The Chair' Later This Week

- FED POWELL SAYS FED SEEKING SUSTAINED PERIOD OF GOOD LABOR MARKET, Bbg

- US PRES BIDEN PLANS CALL WITH ALLIES TO REASSURE SUPPORT FOR UKRAINE, Bbg

- DIMON: THE CONSUMER STILL IN GOOD SHAPE, STILL SPENDING MONEY

Key Links:MNI BRIEF: Barr Says Fed Could Continue QT While Cutting Rates / MNI INTERVIEW: ISM Manufacturing Seen Topping 50 By Year End / MNI: Fed's Barr Says Can 'Proceed Carefully' On Rates / MNI BRIEF: Fed Gov Bowman Sees Need For Further Rate Increases / MNI BRIEF: BOE Forecasts Over Estimate Tightening Impact- Mann

US Tsys Back Near Midday Lows, Mixed Data, Shutdown Averted

- Tsy futures remain weaker, near midday lows after attempting to rebound in the second half. Dec'23 10Y futures are at 107-11 (-23) vs. 107-07 low, 10YY at 4.6785% (+.1074) vs. 4.7014% high. Curves remain steeper: 3M10Y +9.262 at -79.260, 2Y10Y +4.686 at -42.976.

- No delay in economic data this week after Congress passed a stopgap funding bill Saturday evening that will keep Federal agencies open through November 17, 2023.

- Tsys extended lows after S&P Global US Manufacturing PMI comes out higher than expected (49.8 vs. 48.9 est). Fast two way trade was noted after ISM data.

- Treasury futures extend early session lows (TYZ3 107-12.5) then rebound mixed ISM manufacturing came out higher than expected (49.0 vs. 47.8 est). ISM Prices Paid lower than expected (43.8 vs. 48.8 est), Employment higher: (51.2 vs. 48.5 prior) and New Orders (49.2 vs. 46.8 prior). in contrast, Construction Spending was in line with expectations at 0.5%.

- Cross asset summary: Greenback remains strong (DXY +.731 at 106.905), Gold remains weak (-18.77 at 1829.86), crude weaker too (WTI -2.16 at 88.64). Stocks mixed, Nasdaq outperforming: up 21.43 points (0.3%) at 13240.75, DJIA down 201.42 points (-0.6%) at 33310.09, S&P E-Mini Future down 24.75 points (-0.57%) at 4302.

- Limited data release Tuesday, focus on ADP early Wednesday ahead Fri's September Jobs data.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00509 to 5.32408 (+0.00148/wk)

- 3M -0.00735 to 5.38815 (-0.00417/wk)

- 6M -0.01467 to 5.45260 (-0.01228/wk)

- 12M -0.03258 to 5.43368 (-0.01937/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $86B

- Daily Overnight Bank Funding Rate: 5.32% volume: $174B

- Secured Overnight Financing Rate (SOFR): 5.31%, $1.537T

- Broad General Collateral Rate (BGCR): 5.30%, $510B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $496B

- (rate, volume levels reflect prior session)

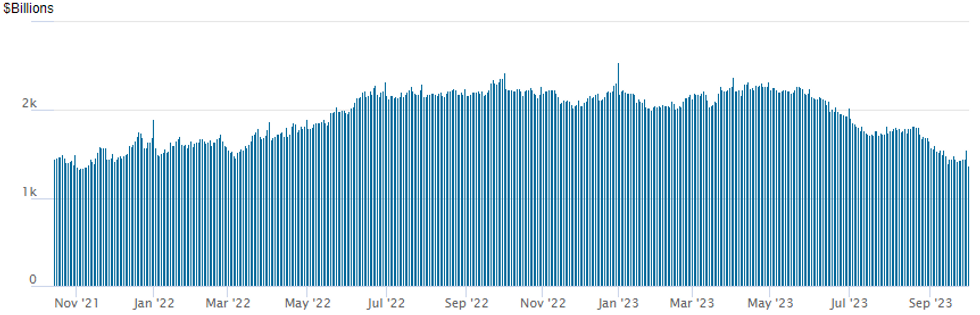

FED REVERSE REPO OPERATION: Falls Back To Early Nov'21 Lows

NY Federal Reserve/MNI

After Friday's month-end surge to $1,557.569B, Repo operation usage falls to $1,365.739B - lowest since early November 2021 w/99 counterparties. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

Better low delta call and call structures traded overnight, particularly in year end SOFR options, accounts fading the weaker underlying and pick-up in rate hike est's. Rate hike projections into early 2024 are bouncing off Friday lows: November at 30.5% vs. 18.6% w/ implied rate change of +7.6bp to 5.405%, December cumulative of 12.6bp at 5.455%, January 2024 12.9bp at 5.458%. Fed terminal at 5.46% in Feb'24.

SOFR Options:

3,000 SFRZ3 94.68/94.75/94.81 call flys ref 94.515

Block, 5,000 SFRZ 94.62/94.68/94.75/94.81 call condors, 1.5 ref 94.52

2,500 SFRH4/SFRM4 93.62 put spds

+2,000 SFRH4 95.25/96.25 call spds, 5.5

+7,000 SFRX3 94.18/94.37/94.43 broken put trees, 0.75 ref 94.52

5,000 SFRF4 94.12/94.37 put spds ref 94.585

Block/screen 10,000 SFRZ3 94.62/94.75/94.87/95.00 call condors

16,000 SFRZ3 94.50/94.56/94.62/94.68 call condors

over 6,000 SFRZ3 94.68/94.75/94.81 call flys ref 94.52

over +27,000 SFRZ3 94.62/94.68/94.75/94.81 call condors (+30k Fri at 1.5)

2,000 0QX3 95.50/95.75/96.00 call flys ref 95.355

Treasury Options:

6,000 TYX3 104.5/106 put spds 16 ref 107-12.5

-17,000 TYX3 109.5 calls, 14 ref 107-15.5

+8,000 TYZ3 105.5 puts, 40, over 16k total from 35 low

over 9,000 TYX3 109.5 calls, 16

over +8,300 TYZ3 105.5 puts, 35

over 6,200 TYX3 105.5 puts, 16

-9,000 FVX3 105/105.25 put spds, 8 ref 105-02.25

over 8,100 FVX 106 calls, 14.5 last

FOREX: Yields, USD Move in Lockstep as Uptrend Resumes

- Markets traded on a steadier footing early Monday, with the worst case scenario of a US government shutdown avoided - helped stabilise equity markets on both sides of the pond. This steadier outlook didn't last through US hours, however, as an underlying USD bidtone followed US bond markets in lockstep. The US 10y yield inched higher still to show above last week's 4.6861% to once again touch levels not seen since late 2007.

- The better-than-expected Manufacturing ISM also proved to be a positive factor for US yields, with the tip in the employment subindex back above 50.0 also factoring in a stronger jobs market ahead of this Friday's nonfarm payrolls release.

- The greenback was the strongest performing currency in G10 Monday, with JPY and CHF also trading well. The NOK and SEK accompanied AUD lower.

- The RBA is likely to leave rates at 4.10% again at its Tuesday meeting, as the economy is developing broadly as the bank expects. Decisions are highly data and outlook dependent and while there have been some upside surprises there haven’t been any developments that would shift the Board from its on hold stance. The tightening bias will probably be retained to keep the central bank’s options open going forward and the accompanying statement may again be little changed.

- Speakers due on Tuesday include Fed's Mester and Bostic, as well as ECB's Simkus, Lane and Villeroy.

FX Expiries for Oct03 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0495(E1.0bln), $1.0810(E1.9bln)

- USD/JPY: Y146.70($762mln), Y147.50($1.3bln), Y149.80-00($1.3bln)

- GBP/USD: $1.2100(Gbp555mln)

- USD/CAD: C$1.3600($1.2bln), C$1.3675($543mln), C$1.3900($1.0bln)

Late Equity Roundup: Communication Services and IT Outperform

- Stocks back near moderate session lows after attempting to rebound in the second half, Nasdaq outperforming: 7 points (0.1%) at 13228.43, DJIA down 201.42 points (-0.6%) at 33310.09, S&P E-Mini Future down 24.75 points (-0.57%) at 4302.

- Leaders: Communication Services and Information Technology continued to outperform, media and entertainment share buoyed the former: Live Nation +2.5%, Google +1.65%, Meta +1.25%. Meanwhile, hardware and storage providers supported the IT sector, outpacing semiconductor stocks in the second half: Arista Networks +1.75%, Apple +1%, Cisco +.6%.

- Laggers: Utilities, Energy and Materials sectors underperformed, independent power and electricity providers weighing on the former: NextEra -11.5%, PG&E -5.9%, AES -7%. Oil and gas providers weighed on the Energy sector as crude fell Monday (WTI -2.24 at 88.55): Marathon Oil -4.65%, APA Corp -4.4%, Occidental Petroleum -4.4%. Meanwhile, metal and mining shares weighed on Materials with gold trading weaker (-17.77 at 1830.86): Newmont -4.4%, Freeport-McMoran -2.8%.

- Technicals: A bear cycle in S&P E-minis remains in play and the contract is trading closer to its recent lows. The recent break of support at 4397.75, the Aug 18 low, reinforced bearish conditions and signals scope for a continuation lower. Sights are on 4242.15, a Fibonacci retracement point. Initial firm resistance is 4467.07, the 50-day EMA. Ahead of the 50-day average is resistance at 4399.00, the Sep 22 high, and 4425.05, the 20-day EMA.

E-MINI S&P TECHS: (Z3) Resistance Remains Intact

- RES 4: 4566.00 High Sep 15 and a key resistance

- RES 3: 4514.50 High Sep 18

- RES 2: 4425.05/4467.07 20- and 50-day EMA values

- RES 1: 4399.00 High Sep 22

- PRICE: 4302.00 @ 1500 ET Oct 2

- SUP 1: 4277.00 Low Sep 27 and the bear trigger

- SUP 2: 4259.00 Low May 31

- SUP 3: 4242.15 1.236 proj of the Jul 27 - Aug 18 - Sep 1 price swing

- SUP 4: 4194.75 Low May 24

A bear cycle in S&P E-minis remains in play and the contract is trading closer to its recent lows. The recent break of support at 4397.75, the Aug 18 low, reinforced bearish conditions and signals scope for a continuation lower. Sights are on 4242.15, a Fibonacci retracement point. Initial firm resistance is 4467.07, the 50-day EMA. Ahead of the 50-day average is resistance at 4399.00, the Sep 22 high, and 4425.05, the 20-day EMA.

COMMODITIES

- WTI Crude Oil (front-month) down $2.14 (-2.36%) at $88.66

- Gold is down $18.69 (-1.01%) at $1830.33

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/10/2023 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 02/10/2023 | 2330/1930 |  | US | Cleveland Fed's Loretta Mester | |

| 03/10/2023 | 0030/1130 | * |  | AU | Building Approvals |

| 03/10/2023 | 0030/1130 | ** | | AU | Lending Finance Details |

| 03/10/2023 | 0330/1430 | *** | | AU | RBA Rate Decision |

| 03/10/2023 | 0610/0810 |  | EU | ECB's Lane speaks at Annual Economics Conference | |

| 03/10/2023 | 0630/0830 | *** |  | CH | CPI |

| 03/10/2023 | 0700/0300 | * |  | TR | Turkey CPI |

| 03/10/2023 | 0835/1035 | | EU | ECB's Lane participates in panel at Annual Economics Conference | |

| 03/10/2023 | 1145/0745 |  | CA | BOC Deputy Nicolas Vincent speech in Montreal | |

| 03/10/2023 | 1200/0800 | | US | Atlanta Fed's Raphael Bostic | |

| 03/10/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 03/10/2023 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 03/10/2023 | 1400/1000 | ** | | US | JOLTS jobs opening level |

| 03/10/2023 | 1400/1000 | ** | | US | JOLTS quits Rate |

| 03/10/2023 | - | *** | | US | Domestic-Made Vehicle Sales |

| 03/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 03/10/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.