Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- BOJ TO DISCUSS YCC TWEAK TO ALLOW RATES OVER 0.5%: NIKKEI

- EIGHT BIGGEST US BANKS FACE A 19% BOOST IN CAPITAL REQUIREMENTS, Bbg

- WHITE HOUSE: GDP DATA SHOWS ECONOMY EXPANDED AT HEALTHY CLIP, Bbg

- LAGARDE: FUNDING HAS BECOME MORE EXPENSIVE FOR BANKS, Bbg

cropfilter_vintageloyaltyshopping_cartdelete

US TSYS: Late Session Focus on BOJ Rate Decision Tonight

- Treasury futures are extending session lows, curves bear steepening with the short end resisting the post-auction sell-off. While the 7Y note sale tailed 1.5bp, Treasury futures experienced a knee-jerk sell-off to new session lows after Nikkei report elevated yield curve control discussion by the BOJ at tonight's policy meeting (2200ET).

- "The Bank of Japan will discuss tweaking its yield curve control policy at a policy board meeting Friday to let long-term interest rates rise beyond its cap of 0.5% by a certain degree, Nikkei has learned, in what would be a shift toward a more flexible policy approach."

- Treasury 10Y futures have fallen to 110-30.5 low (-1-06), yield hitting 4.0142% high (July 10 levels), well through 1.0% 10-dma envelope support, and just above 110-28 (76.4% retracement of the Jul 7 - 18 rally). A breach of 110-28 puts focus on key support of 110-05 (Low Jul 6 and the bear trigger).

- Curves have bear steepened on the move, 3M10Y currently +16.191 at -142.759 (compared to -173.5 low on July 18), 2s10s +5.816 at -93.079.

- Reminder: heavy slate of corporate earning remain after today's close, include: Intel, Olin Corp, Weyerhaeuser, KLA, Roku, Juniper Networks, Mettler-Toledo, Mohawk Ind, US Steel Corp.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00128 to 5.31865 (+.02066/wk)

- 3M +0.00353 to 5.36912 (+.01791/wk)

- 6M +0.00757 to 5.45283 (+.02440/wk)

- 12M +0.00466 to 5.40252 (+.04102/wk)

- Daily Effective Fed Funds Rate: 5.08% volume: $98B

- Daily Overnight Bank Funding Rate: 5.07% volume: $265B

- Secured Overnight Financing Rate (SOFR): 5.06%, $1.452T

- Broad General Collateral Rate (BGCR): 5.04%, $589B

- Tri-Party General Collateral Rate (TGCR): 5.04%, $582B

- (rate, volume levels reflect prior session)

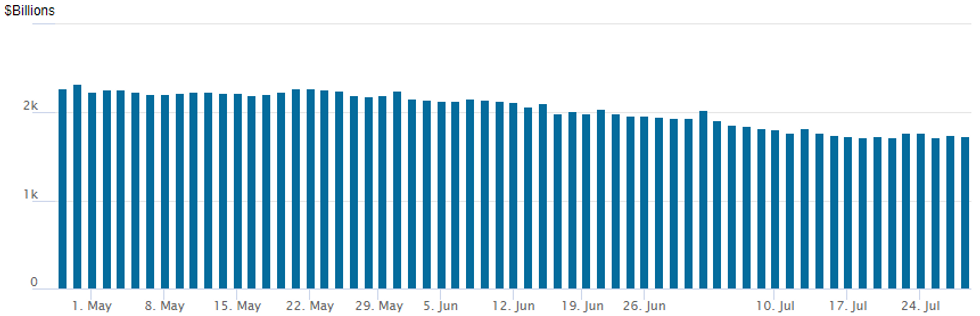

FED Reverse Repo Operation

NY Federal Reserve/MNI

The latest operation recedes to $1,735.783B, w/103 counterparties, compared to $1,749.733B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

US SOFR/TREASURY OPTION SUMMARY

Better downside put trade continued to drive SOFR and Treasury option volumes Thursday, underlying futures broadly lower/near lows after late market chatter the BOJ will discuss yield curve control at tonight's policy meeting. Curves bear steepened, however, as projected rate moves through year end move closer to no change after Goldilocks nature of strong data w/ cooling recession expectations.

- SOFR Options:

- Update, +20,000 SFRZ3 93.50/94.25 put spds 2.75-3.0 vs. 94.595/0.13%

- Block, -5,000 SFRZ3 94.87/95.12/95.25/95.50 put condors, 1.0 vs. 94.57/0.10%

- +5,000 SFRH4 94.12/94.37/94.62/94.87 put condors, 10.0

- 5,500 SFRH4 94.00/94.25/94.37/94.62 put condors ref 94.835 to -.825

- Block, 5,000 SFRZ3 94.75/95.25 call spds 5.0 w/ SFRZ3 94.25/94.75 put spds 24.0, 29.0 total iron fly vs. 94.60/0.26%

- +3,000 2QV3 96.00 puts, 9.0 vs. 96.52/0.22%

- 5,000 SFRZ4 94.00 puts, 8.0

- Block/screen -20,000 SFRU3 94.50 puts, 2.5

- 2,000 OQV3 95.37/95.62/95.87 put trees

- 5,000 OQU3 95.50/95.75/96.00 call flys, ref 95.63

- Block, 8,000 SFRU3 94.37/94.50 put spds, 2.25 vs. 94.575/0.20%

- Block/screen, 10,500 SFRZ4 93.50/94.25/95.00 put flys, 10.5 net ref 95.97 to -.975

- 2,000 SFRU3 94.12 puts, 0.5 ref 94.575

- Treasury Options:

- over 8,300 FVU3 108.25 calls, 11 ref 106-25

- 2,500 TUU3 103 puts, 131.5

- 2,000 USU3 122 puts, 27

- 5,000 TYU3 108/110 put spds ref 111-23.5

- 6,200 wk4 TY 112/112.5/113 call flys, 4.0 ref 111-24.5

- 8,300 TYU3 110 puts, 14 ref 112-03 to -03.5

- 3,100 TYU3 108.25 puts, 4

- over 3,000 FVU3 108 calls, 20.5 last

- over 3,700 TYU3 109.5 puts, 10 last

- over 4,300 TYU3 110.5 puts, 21 last

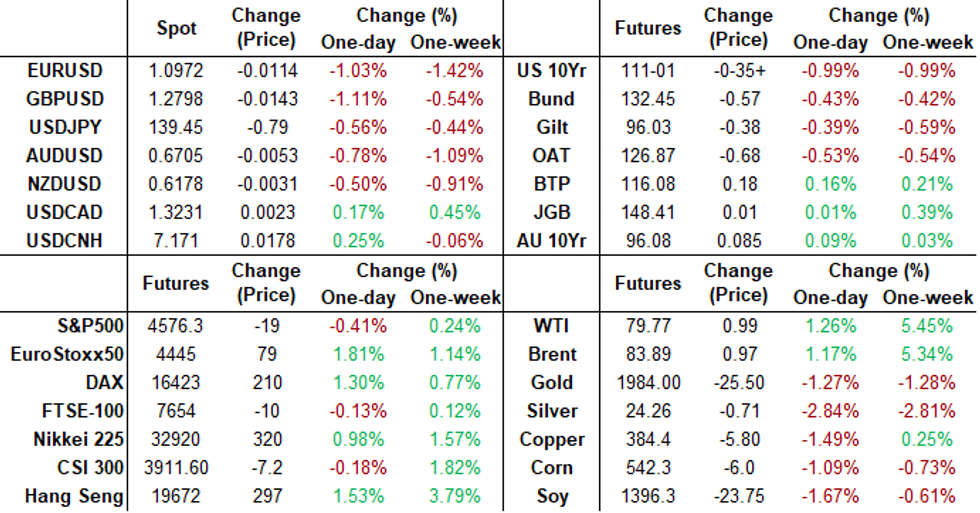

FOREX: USD Index Boosted By Strong US GDP, Late JPY Surge Before BOJ Decision

- Stronger than expected GDP data on Thursday provided a strong boost to the greenback with the USD index showing gains of around 0.85% as we approach the APAC crossover. A more cautious ECB also weighed on the Euro, which has prompted EURUSD to shed around 170 pips and significantly reverse an early morning rally.

- Second quarter data from the US showed the economy grew 2.4% Q/q, well ahead of the 1.8% estimate. Combined with a lower GDP price index, the soft landing theory gained traction which initially provided a firm bid for both the US dollar and major equity indices.

- The USD bid has prevailed and while sitting slightly off session highs, the DXY has resumed its recovery and approaches the June lows around the 102 mark.

- The greenback shift is most notable against EUR, GBP and CHF which have all declined around 1%. USD gains had been entirely broad based before a late report from the Nikkei regarding the Bank of Japan prompted a punchy surge for the Japanese Yen.

- USDJPY fell aggressively from around 141.00 to 139.21 lows following reports that the Bank of Japan will discuss tweaking its yield curve control policy at a policy board meeting Friday. This would apparently allow “long-term interest rates to rise beyond its cap of 0.5% by a certain degree”, Nikkei is said to have learned.

- While the piece only mentions potential discussions and shows no attribution, the substantial JPY bounce places Friday’s BOJ meeting/decision at the top of the event risk agenda. 139.11, the July 20 low and 138.77 the July 19 low are the immediate reference points on the downside for USDJPY before key support at 137.25.

- As well as the BOJ, European preliminary CPI data is due Friday, as well as US Core PCE, US Employment Cost index and Canadian GDP.

FX Expiries for Jul28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1000(E844mln), $1.1050(E2.0bln), $1.1075(E966mln), $1.1100(E876mln), $1.1120-30(E560mln), $1.1190(E1.4bln)

- USD/JPY: Y140.25($1.0bln)

- AUD/USD: $0.6850(A550mln)

- USD/CAD: C$1.3235-50($553mln), C$1.3280($826mln)

Late Equities Roundup: Off Early Highs

- Stocks trading modestly higher for the most part, off early session highs, with Dow stocks underperforming in the second half. Currently, DJIA shares are down 47.3 points (-0.13%) at 35476.25, S&P E-Mini Future up 0.25 points (0.01%) at 4596, Nasdaq up 56.3 points (0.4%) at 14185.6.

- Leading gainers: Communication Services, Information Technology and Consumer Discretionary sectors outperformed in the second half. Communication Services led by strong gains in Comcast +6%, Meta +5.45% (earnings and forward guidance beat expectations), Charter Communication +2.38%. Chip stocks buoyed IT sector: Lam Research +10.3%, Applied Materials +7.2%, KLA Corp +7.0%.

- Laggers: Utilities, Real Estate and Financials underperformed. Financial services stocks lagged banks and insurance companies Thursday: S&P Global -7.25%, Fiserv Inc -2.86%, Ameriprise -2.0%. Early Bbg headline: EIGHT BIGGEST US BANKS FACE A 19% BOOST IN CAPITAL REQUIREMENTS, did little to dampen shares of Citi +1.92%, Fifth Third +0.56%, KeyCorp +0.5%.

- Technicals: The E-mini S&P contract remains in a bull mode condition and is trading higher today. Attention is on the top of the bull channel drawn from the March 13 low - the top intersects at 4632.89 today and it has been pierced. A clear channel breakout would strengthen bullish conditions and open 4639.69, a Fibonacci projection. A corrective pullback, if seen, would initially target the 20-day EMA at 4522.44 and a key short-term support.

E-MINI S&P TECHS: (U3) Tests Channel Resistance

- RES 4: 4709.55 3.0% 10-dma envelope

- RES 3: 4670.25 2.00 proj of the Jun 26 - 20 - Jul 7 price swing

- RES 2: 4639.79 1.764 proj of the Jun 26 - 20 - Jul 7 price swing

- RES 1: 46334.50 Intraday high

- PRICE: 4592.00 @ 14:10 ET Jul 27

- SUP 1: 4522.44 20-day EMA

- SUP 2: 4470.00 Low Jul 12

- SUP 3: 4419.34 50-day EMA

- SUP 4: 4386.29 Bull channel base drawn from the Mar 13 low

The E-mini S&P contract remains in a bull mode condition and is trading higher today. Attention is on the top of the bull channel drawn from the March 13 low - the top intersects at 4632.89 today and it has been pierced. A clear channel breakout would strengthen bullish conditions and open 4639.69, a Fibonacci projection. A corrective pullback, if seen, would initially target the 20-day EMA at 4522.44 and a key short-term support.

COMMODITIES: Oil Grinds Towards Key Resistance, Gold Slumps On USD Strength

- Crude and oil product markets extended gains today to new 3-month highs after solid US Q2 GDP data and despite an added USD headwind from a dovish ECB.

- The Brent second month implied volatility has fallen to the lowest since September 2021 after a steady decline in the last couple of months. Crude price swings have eased as futures have seen a steady rally during July due to OPEC supply cuts and potential China stimulus measures while US and China demand growth concerns continue to weigh.

- Oil may rise in H2 with a decline in crude in storage over the next few months according to International Energy Forum.

- WTI is +1.3% at $79.83 off an earlier high of $80.57 moving closer to key resistance at $81.44 (Apr 12 high).

- Brent is +1.2% at $83.93 off an earlier high of $84.47 that moved closer to key resistance at $85.47 (Apr 12/13 highs).

- Gold is -1.35% at $1945.43 as the US dollar surged on a combination of strong data and a dovish ECB. Treasury yields climbed strongly with an added tailwind from BoJ YCC speculation ahead of the upcoming decision, but gold had already touched lows before then. It has cleared support at the 50-day EMA of $1951.2 with a low of $1942.74, after which lies further support at $1924.5 (Jul 11 low).

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/07/2023 | 0130/1130 | ** |  | AU | Retail Trade |

| 28/07/2023 | 0200/1100 | *** |  | JP | BOJ policy announcement |

| 28/07/2023 | 0530/0730 | *** |  | FR | GDP (p) |

| 28/07/2023 | 0530/0730 | ** | | FR | Consumer Spending |

| 28/07/2023 | 0530/0730 | *** |  | DE | North Rhine Westphalia CPI |

| 28/07/2023 | 0600/0800 | ** |  | SE | Unemployment |

| 28/07/2023 | 0600/0800 | ** | | SE | Retail Sales |

| 28/07/2023 | 0645/0845 | *** | | FR | HICP (p) |

| 28/07/2023 | 0645/0845 | ** | | FR | PPI |

| 28/07/2023 | 0700/0900 | *** |  | ES | GDP (p) |

| 28/07/2023 | 0700/0900 | *** | | ES | HICP (p) |

| 28/07/2023 | 0800/1000 | ** |  | IT | PPI |

| 28/07/2023 | 0800/1000 | *** | | DE | Bavaria CPI |

| 28/07/2023 | 0900/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 28/07/2023 | 0900/1100 | *** | | DE | Saxony CPI |

| 28/07/2023 | 1200/1400 | *** | | DE | HICP (p) |

| 28/07/2023 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 28/07/2023 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 28/07/2023 | 1230/0830 | ** | | US | Employment Cost Index |

| 28/07/2023 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 28/07/2023 | 1500/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.