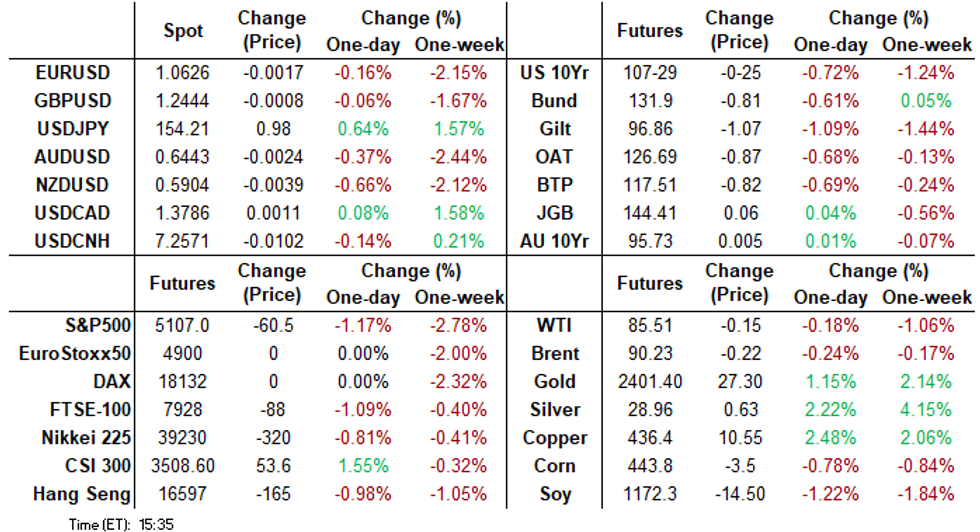

- Treasuries remained sensitive to Middle East geopolitical headlines Monday, overshadowing Retail Sales beat.

- Treasuries more than unwound Friday's safe-haven rally after Iran attacked Israeli Military sites with few casualties.

- Monday's sell-off stalled after Israeli military officials said they had "no choice but to retaliate against Iran", Axios.

US TSYS Off Early Lows, Curves Steepen, Remain Sensitive to Middle East Tension

- Treasury futures remain sensitive to Middle East tensions Monday, bouncing off lows late morning after headline fromAxios that Israel has "no choice but to retaliate against Iran.

- Futures had extended session lows this morning (TYM4 107-18.5) more than reversing Friday's risk-off rally tied to tensions in the Middle East before rebounding to 108-00 - trading sideways through the close. Several factors at play:

- Rates rallied with a strong safe-haven bid last Friday amid simmering Middle East tensions going into the weekend. Iran did indeed retaliate against Israel with some 200 drone attacks targeting military sites, many were repelled with few casualties.

- Tsy yields also gained as US$ bounced against the Yen, the latter falling to lowest lvl since 1990 as Japan said they would take steps (intervene) to counter.

- Tsy curves bear steepened, 2s10s +7.184 at -30.529, short end still weaker as projected rate cut pricing recedes: May 2024 at -4.7% w/ cumulative -1.2bp at 5.317%; June 2024 at -19.8% vs. -22.6% (compares to -55.1% pre-CPI) w/ cumulative rate cut -6.1bp at 5.286%. July'24 cumulative at -14.4bp vs -16.9bp earlier, Sep'24 cumulative -25.9bp vs. -28.8bp.

- Look ahead: Tuesday's data calendar includes Building Permits, IP/Cap-U, and Fed Speak with Chairman Powell moderating a Q&A session with BoC head Macklem.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00305 to 5.31624 (+0.00083 total last wk)

- 3M -0.01059 to 5.31707 (+0.03427 total last wk)

- 6M -0.02153 to 5.28184 (+0.08303 total last wk)

- 12M -0.03703 to 5.17201 (+0.17797 total last Wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.805T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $701B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $687B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $88B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $243B

FED Reverse Repo Operation: Tax Deadline Spurs New Low Usage

NY Federal Reserve/MNI

- RRP usage falls well below $400B for the first time since mid-May 2021 to $327.066B vs. $407.322B last Friday, desks citing today's Federal tax deadline for the drop.

- Meanwhile, the latest number of counterparties falls to new low of 62 vs. 65 Friday.

SOFR/TEASURY OPTION SUMMARY

Better SOFR, Treasury option put trade reported on net early Monday followed by some large unwinds/repositions and upside calls in the second half as the sell-off in underlying futures stalled since midday. Projected rate cut pricing recedes from Friday's levels: May 2024 at -4.7% w/ cumulative -1.2bp at 5.317%; June 2024 at -19.8% vs. -22.6% (compares to -55.1% pre-CPI) w/ cumulative rate cut -6.1bp at 5.286%. July'24 cumulative at -14.4bp vs -16.9bp earlier, Sep'24 cumulative -25.9bp vs. -28.8bp.

- SOFR Options:

- +65,000 SFRZ4 98.50/99.00 call spds 0.5 vs. 95.065/0.05%

- -20,000 SFRM4 94.81/94.93 put spds 1.75 over SFRU4 94.87/95.00 put spreads

- -10,000 SRM4 94.87 calls vs 0QM'4 96.50 calls 1.75

- +10,000 0QN4 94.37/94.75 put spread vs SRK4 94.68 puts 0.75

- +3,500 SRN4 94.62/94.75/94.87 put trees 3.25

- -7,500 0QK4 95.75 calls 5.0 ref 95.40

- +5,000 SFRZ4 97.50/98.50 call spds 8.5

- +2,000 SRQ4 94.62/94.87/95.00 put flys 3.75 ref 94.875

- -5,000 0QK4 95.62 calls, 7.5 vs. 95.385 to -.39/0.30%

- -12,500 0QK4 96.00 calls, 2.5-2.0 vs. 95.37/0.10%

- Block, 5,000 SFRU4 95.75/96.00 call spds, 1.0 ref 94.89

- 2,000 0QZ4 96.00/96.50 call spds ref 95.715

- 2,000 SFRK4 94.68 puts vs. 3,000 SFRM4 94.62/94.68 put spds

- 5,000 SFRH5 94.62 puts ref 95.265

- +29,250 SFRU4 94.75 puts, 9.0 vs. 94.94/0.32%

- 1,000 SFRH4 94.62/95.12 2x1 put spds vs. 3,000 SFRU4 94.75 puts

- 1,500 SFRM4 94.62/94.68/94.75/94.81 call condors

- Treasury Options:

- 3,750 TYM4 108/109.5 1x2 call spds, 8 ref 107-29

- 9,250 TYK4 109.75 calls, 4 ref 107-28.5

- 3,350 USK4 115 puts, 1-23 ref 114-04

- 10,000 TYM4 108.5 calls, 51 ref 107-27

- Block, -14,000 TYM4 108 puts, 106 vs. 107-27/0.50%

- +10,000 TYK4 107.75 puts, 28 vs. 107-30.5

- 7,800 wk3 10Y 107.5 puts, 7 ref 108-07.5

- +9,000 TYK4 110.25 calls, 5

- 2,000 wk1 10Y midcurve 107/107.25/108/108.25 put condors ref 108-12

- -10,000 Monday 10Y midcurve 108/108.5 put spds 12-14

FOREX USDJPY Surges Above 154.00 Amid Further Hot US Data

- Higher-than-expected retail sales data in the US prompted further upward pressure on US yields to start the week, maintaining an underlying bid for the greenback and further weighing on a struggling Japanese Yen.

- USDJPY had already rallied in Asia as risk sentiment stabilised amid the ongoing concerns in the middle east. This saw the pair extend its impressive advance to around 153.80, following the prior clean break above 152.00.

- Aided by the US data, the pair then cleared 154.00 and printed fresh cycle highs at 154.45. Japan’s top currency official said that the MOF is in frequent contact with FX officials abroad, however, the fundamental backdrop and widening yield differentials continue to drive USDJPY higher.

- Further defying the Japanese authorities’ warnings of intervention against outsized moves in the currency, CFTC data shows the JPY net short position growing to 50% of open interest – leaving markets outright short by 162,151 contracts, the largest net short since the onset of the Global Financial Crisis in 2007.

- Elsewhere, G10 ranges were more subdued with EURUSD briefly matching Friday’s lows around 1.0622 in the aftermath of the US data release. The moderate pull lower for equities leaves NZD as the underperformer, falling 0.4% against the greenback.

- The high frequency of UK risk events this week has prompted a solid rally in the front-end of the vol curve, with 1-week vols touching new multi-month highs today. This leaves the one-week breakeven on a GBP/USD straddle at ~100 pips, leaving support at 1.2427 – last week’s GBP/USD low - exposed ahead of 1.2364, seen as firmer support.

- Chinese activity data will be the highlight of Tuesday’s Asia-Pac session, before focus turns to employment data in the UK. The latter half of the session will have Canada CPI for March.

FX Expiries for Apr16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0650-70(E3.2bln), $1.0700(E936mln), $1.0750-60(E1.0bln), $1.0800(E2.1bln), $1.0820(E1.0bln), $1.0900(E1.9bln)

- USD/JPY: Y153.00($510mln)

- AUD/USD: $0.6500(A$1.0bln), $0.6600(A$737mln)

- AUD/NZD: N$1.0900(A$594mln)

- AUD/JPY: Y97.50-60(A$1bln)

- USD/CNY: Cny7.2450($1.3bln)

Late Equities Roundup: Under Pressure, Near Round Number Support

- Stocks are trading weaker late Monday amid ongoing, reversing this morning's bounce off Friday's lows as Middle East geopolitical tensions sapped markets risk appetite. Several rounds of program selling reported after Israeli military officials said they had "no choice but to retaliate against Iran" Axios reported.

- S&P E-Mini future neared round number technical support of 5100.0 late rebounded to 5118.5 down 49 points (-0.95%) at 5118.5, Nasdaq down 233.7 points (-1.4%) at 15940.88, DJIA down 189.23 points (-0.5%) at 37790.59.

- Laggers: Real Estate and Information Technology sector shares underperformed in late trade, estate management and services weighed on the former: CoStar Group -3.46%, CBRE Group -2.43%. Software stock weighed on the IT sector late: Salesforce -6.72%, Enphase -4.27%, ServiceNow Inc -3.73%.

- Leading Gainers: Health Care and Financial sector stocks outperformed in the first half, equipment and services shares buoyed the former with Centene +3.35%, Cardinal Health +2.12%, United Health Care +1.52%. Banks led gains in the Financial sector after announcing better than expected earnings this morning: M&T Bank +4.52%, Goldman Sachs +2.99%, Wells Fargo (annc last Friday) +0.71%.

- Expected to announce quarterly earnings Tuesday: Bank of NY Melon, PNC Financial, Bank of America and Morgan Stanley.

E-MINI S&P TECHS: (M4) Testing Support At The 50-Day EMA

- RES 4: 5434.54 Bull channel top drawn from the Jan 17 low

- RES 3: 5428.25 1.00 proj of the Oct 27 - Dec 28 - May 1 price swing

- RES 2: 5400.00 Round number resistance

- RES 1: 5285.00/5333.50 High Apr 10 / 1 and the bull trigger

- PRICE: 5102.00 @ 1505 ET Apr 15

- SUP 1: 5100.75 Intraday low Apr 15

- SUP 2: 5100.00 Round number support

- SUP 3: 5018.00 Low Feb 21

- SUP 4: 4994.25 Low Feb 13

The trend condition in S&P E-Minis is unchanged and remains bullish. Near-term, the recent move down appears to be a correction and this is allowing an overbought signal to unwind. The contract has recently breached bull channel support drawn from the Jan 17 low. The next key support lies at the 50-day EMA, at 5159.12. A clear break of the EMA would signal scope for a deeper retracement. Key resistance is 5333.50, the Apr 1 high.

COMMODITIES Spot Gold Edges Higher On Geopolitical Tensions

- Spot gold rose by 1.1% to $2,370/oz on Monday, as geopolitical tensions in the middle east continued to drive safe haven demand.

- Although down from Friday’s record intra-day high of $2,431.5, the trend condition in gold remains bullish. The next objective is $2452.5, a Fibonacci projection. Initial firm support is at $2264.8, the 20-day EMA.

- Meanwhile, silver outperformed today, rising by 3.1% to $28.7/oz. This brought the gold/silver ratio down further, to its lowest level since early December.

- Crude prices are marginally lower on the day, having tapered their losses amid the continued tensions between Israel and Iran.

- WTI May 24 is down 0.3% at $85.4/bbl.

- The Iranian attack on Israel was well known about prior to its launch, leading to a lack of price impact on Monday, according to analysts. Iran’s strike on Israel is also not expected to disrupt oil markets.

- For WTI futures, the bull theme remains intact, with the next objective at $89.08, a Fibonacci projection. Initial firm support to watch lies at $83.70, the 20-day EMA.

- Henry Hub has fallen further on the day to its lowest level since March 26, amid further curtailed LNG flows and limited heating and cooling demand.

- US Natgas May 24 is down 4.5% at $1.69/mmbtu

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/04/2024 | 0000/2000 |  | US | San Francisco Fed's Mary Daly | |

| 16/04/2024 | 0200/1000 | *** |  | CN | GDP |

| 16/04/2024 | 0200/1000 | *** | | CN | Fixed-Asset Investment |

| 16/04/2024 | 0200/1000 | *** | | CN | Retail Sales |

| 16/04/2024 | 0200/1000 | *** | | CN | Industrial Output |

| 16/04/2024 | 0200/1000 | ** | | CN | Surveyed Unemployment Rate M/M |

| 16/04/2024 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 16/04/2024 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 16/04/2024 | 0900/1100 | *** |  | DE | ZEW Current Conditions Index |

| 16/04/2024 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 16/04/2024 | 0900/1100 | * |  | EU | Trade Balance |

| 16/04/2024 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 16/04/2024 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 16/04/2024 | 0915/1015 | | UK | BOE's Lombardelli TSC pre-appointment hearing | |

| 16/04/2024 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 16/04/2024 | 1230/0830 | *** | | CA | CPI |

| 16/04/2024 | 1230/0830 | *** | | US | Housing Starts |

| 16/04/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 16/04/2024 | 1300/0900 | | US | Fed Vice Chair Philip Jefferson | |

| 16/04/2024 | 1315/0915 | *** | | US | Industrial Production |

| 16/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 16/04/2024 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 16/04/2024 | 1630/1230 | | US | New York Fed President John Williams | |

| 16/04/2024 | 1700/1800 | | UK | BoE's Bailey Interview On IMF Today | |

| 16/04/2024 | 1700/1300 | | US | Richmond Fed's Tom Barkin | |

| 16/04/2024 | 1715/1315 | | US | Fed Chair Jerome Powell | |

| 16/04/2024 | 2000/1600 | | CA | Canada federal budget |