Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

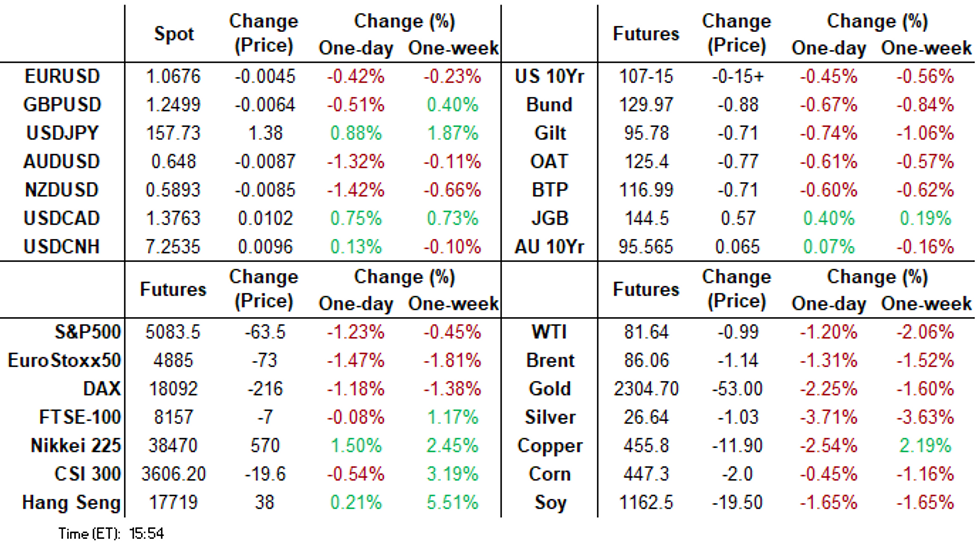

- Treasuries gapped lower early Tuesday, adjusting to higher than expected Employment Cost Index data.

- Rates continued to extend lows into the close, unlikely month end related while stocks, gold and crude sagged.

- Focus squarely on Wednesday's FOMC announcement, no major changes in guidance expected.

US Tsys Nearing Technical Support Ahead FOMC, Month End, May Day Holiday

- Treasury futures gap lower after higher than expected Employment Cost Index (1.2% vs. 1.0% est, 0.9% prior), holding lower levels after much lower than expected MNI Chicago PMI comes out at 37.9 vs 45.0 est (41.4 prior).

- Broader macro considerations will have to wait until Thursday’s Q1 preliminary release for productivity. Strong productivity gains have offset labor costs in recent quarters but consensus sees productivity growth tailing off to 0.7% annualized in Q1.

- Futures extended lows into the close, Jun'24 10Y marking 107-13 low, still above initial technical support at 107-04 (Low Apr 25).

- Focus turns to Wednesday's FOMC announcement with Chairman Powell discussing guidance 30 minutes later. That said May Day holiday in Europe tomorrow, closings inconsistent across markets and asset classes (Eurex closed, but not ICE: Gilts re: FI) - that may be exacerbated by month end squaring.

- Projected rate cut pricing continued to recede vs. morning levels: May 2024 -1.0 vs. -2.1% earlier w/ cumulative -0.3bp at 5.326%; June 2024 at -6.6% vs. -10.6% w/ cumulative rate cut -1.9bp at 5.310%, July'24 cumulative at -5.1bp, Sep'24 cumulative -12.6bp.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00275 to 5.31592 (+0.00019/wk)

- 3M +0.00133 to 5.32814 (-0.00136/wk)

- 6M +0.00204 to 5.31151 (-0.00271/wk)

- 12M -0.00199 to 5.23454 (-0.00926/wk)

- Secured Overnight Financing Rate (SOFR): 5.32% (+0.00), volume: $1.781T

- Broad General Collateral Rate (BGCR): 5.31% (+0.00), volume: $696B

- Tri-Party General Collateral Rate (TGCR): 5.31% (+0.00), volume: $666B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $94B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $270B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage climbs to $534.234B vs. $505.530B Monday. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

- Meanwhile, the latest number of counterparties inches up to 76 vs. 75 prior.

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury option trade remained mixed Tuesday, slightly better early bullish flow evaporated as underlying futures continued to extend lows into the close. Focus on tomorrow's FOMC announcement. Projected rate cut pricing continued to recede vs. morning levels: May 2024 -1.0 vs. -2.1% earlier w/ cumulative -0.3bp at 5.326%; June 2024 at -6.6% vs. -10.6% w/ cumulative rate cut -1.9bp at 5.310%, July'24 cumulative at -5.1bp, Sep'24 cumulative -12.6bp.

- SOFR Options:

- +10,000 SFRV4 94.37/94.62 put spreads 3.75 ref 94.96

- +4,000 0QH4 94.75/96.75 put over risk reversals 0.5 vs. 95.69/0.40%

- +10,000 SFRU4 94.93/95.12/95.18 1x3x2 broken call flys, 1.75 ref 94.815

- -15,000 SFRM4 94.68/94.75 2x1 put spds,

- -5,000 SFRZ4 94.43/94.68 put spds vs. 0QZ4 95.50/95.75 put spds, 7.25 net

- +6,000 SFRM5 93.75/94.25 put sods, 6.25 ref 95.325

- +8,000 SFRU4 94.43/94.56 put spds, 1.0 vs. 94.84/0.20%

- Block (adds to +10k earlier), +10,000 0QU4 94.62 puts, 7.0

- -5,000 SFRU4 94.75/96.25 call spd w/ SFRU 94.68 put, 19.5-19.25 ref 94.82

- -10,000 SFRK4 94.75/94.81/95.00/95.06 put condor ref 94.70) w/ SFRN4 95.06/95.18/95.43/95.56 put condor (ref 94.82), selling both structures for 1.25 total.

- Block, 10,000 0QU4 94.62 puts, 7.0 ref 95.465

- 5,000 0QK4 95.75 calls ref 95.36

- 5,000 SFRM4 96.18 calls ref 94.71 to -.705

- 2,000 SFRM4 94.87/95.00 2x3 put spds ref 94.705

- Treasury Options:

- 2,000 TYM4 111/112/113/114 call condors

- 10,000 Monday weekly 108.5/109 call spds, 4-5 ref 107-19 to -20.5 (expire May 6)

- 3,000 Wednesday weekly 30Y 114.5/115 call spds, 2 (expire tomorrow)

- over 8,700 TYM4 106 puts, 12 last

- 1,500 FVM4 106.25/107/107.75 call flys ref 104-31.75

- 1,500 TYM4 111.5/112 call spds ref 107-29

- 2,000 FVM4 107.75/108.5 call spds ref 105-01.5

- 4,000 TYM4 107/108 put spds vs. TYM4 109 calls ref 107-31

EGBs-GILTS CASH CLOSE: Broad Weakness As Data Pares Implied ECB/BoE Cuts

European yields rose sharply Tuesday as data pointed to fewer 2024 BoE/ECB rate cuts.

- While French and Dutch April inflation out early in the session were largely in line with expectations, the Eurozone-wide report saw slight upside surprises on both core and services HICP while GDP was above-expected, putting pressure on core FI.

- Stronger-than-expected US employment cost data and latterly a jump in MNI Chicago PMI prices paid saw Treasuries drag Bunds and Gilts down further in the afternoon.

- A pullback in oil prices and equities helped EGBs/Gilts find a floor toward the cash close.

- On the day, ECB 2024 cut pricing was pared 5bp to 66bp; BoE by 6bp to 41bp.

- Bunds underperformed Gilts, with the German curve bear flattening and the UK's bear steepening. Periphery EGB spreads widened modestly.

- Wednesday's calendar sees the US Federal Reserve decision featuring, but European trade will be limited due to the May Day holiday.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 7.2bps at 3.034%, 5-Yr is up 6.8bps at 2.616%, 10-Yr is up 5.2bps at 2.584%, and 30-Yr is up 2.6bps at 2.69%.

- UK: The 2-Yr yield is up 5.2bps at 4.506%, 5-Yr is up 4.8bps at 4.251%, 10-Yr is up 5.5bps at 4.347%, and 30-Yr is up 4.1bps at 4.787%.

- Italian BTP spread up 0.9bps at 133.3bps / Spanish bond down 0.1bps at 77bps

EGB Options Mixed But Busy In Euro Rates

Tuesday's Europe rates/bond options flow included:

- RX 129/128ps, 1x1.5 bought for 15 in 2k

- ERN4 96.37/96.50/96.75c fly, bought 1.25 and 1.5 in 8k total

- ERZ4 96.62/96.50/96.37p fly, bought for 1.5 in 7k

- ERZ4 96.625/97.25cs 1x1.5 sold at 16 in 8k (ref 96.735, 35 del)

- ERZ4 96.625/97.125/97.625c fly vs 96.37p, bought the fly for 6.75 in 2.5k

FOREX US Data Underpins Supportive Greenback Tone, AUD, NZD and CHF all Plummet

- Higher-than-expected US data has underpinned a strong USD bid throughout Tuesday’s session, prompting a further adjustment of fed pricing and an associated 0.58% rally for the USD index.

- A firmer-than-expected Q1 employment cost reading provided the latest ‘hawkish’ input for FOMC-dated OIS, leaving ~31bp of cuts priced through ’24 vs. ~35bp pre-release. Even within the Chicago Business Barometer details prices paid rose 6.7 points to 69.3, the highest level since August 2023, and 5.7 points above the prior 12-month average of 63.6.

- Downside pressure on equity markets has provided an additional tailwind for the greenback, with potential month-end dynamics also bolstering the supportive greenback tone.

- AUD and NZD have extended their poor performance overnight and remain the weakest in G10, both declining around 1.2% as we approach the APAC crossover. Weaker-than-expected Australian data overnight set the tone here and AUDUSD has grinded below the 0.6500 handle, narrowing the gap to initial support at 0.6441.

- The Swiss Franc has also notably suffered which sees USDCHF (+0.81%) rise to a fresh cycle high on Tuesday, printing at 0.9185. It’s worth highlighting that we have April Swiss CPI data on Thursday, an important data point given the Swiss Franc’s sensitivity to the March release amid the dovish stance of the SNB, who unexpectedly cut rates in March. USDCHF’s impressive rally across 2024 will continue to target the October 2023 highs, residing at 0.9244.

- For the major pairs, EURUSD remained heavy and briefly traded a new low on the week at 1.0676, however, the pair remains in a 60 pip range on the day. USDJPY edged higher, taking out 157.00 and consolidated around 157.50 as markets slowly eroded the sharp move lower from Monday, following the touted intervention from the BOJ.

- RBNZ Governor Orr is due to hold a press conference about the Financial Stability Report overnight. Multiple European holidays may pave the way for a subdued session before the focus swiftly turns to the US ISM Manufacturing PMI and the May Fed decision/press conference.

Late Equities Roundup: Hugging Lows Into Month End, FOMC, EU Holiday

- Stocks in the red after the bell - trader notes the S&Ps are "poised to halt a streak of five consecutive monthly gains". Treasury futures marked new lows into the close too amid broad based position squaring ahead of tomorrow's FOMC announcement.

- Note: May Day holiday in Europe tomorrow, closings inconsistent across markets and asset classes (Eurex closed, but not ICE: Gilts re: FI) - that may be exacerbated by month end squaring.

- Currently, DJIA is down 443.13 points (-1.15%) at 37941.46, S&P E-Minis down 55.25 points (-1.07%) at 5091.75, Nasdaq down 205 points (-1.3%) at 15775.96.

- Energy and Consumer Discretionary sectors continued to underperform in late trade. Oil and Gas shares weighed on the Energy sector: Marathon Petroleum -7.66%, Phillips66 -4.76%, Valero -3.490%. Auto and parts makers weighed on the Consumer Discretionary sector: EV maker Tesla -4.98% after gaining 14.27% Monday, Ford -4.04%, GM -3.0% while parts makers Aptiv declined 2.44%, Borg Warner -1.96%.

- Leading gainers: Health Care and Utilities sector shares continued to outperform in late trade: pharmaceuticals and biotech shares supported the former: after boosting revenue outlook for the year, Eli Lilly gained 5.72%, West Pharmaceutical Services +2.24%, AbbVie +0.41%. The Utilities sector was next up with CMS Energy +1.05%, AEP +0.73%, Public Services Enterprises +0.71%.

- Expected corporate earnings announcements after today's close: Stryker, Prudential Fncl, ONEOK, Boston Properties, Diamondback Energy, Public Storage, Pinterest, Amazon, Starbucks, Advanced Micro Designs.

E-MINI S&P TECHS: (M4) Testing Resistance At The 20-Day EMA

- RES 4: 5333.50 High Apr 1 and the bull trigger

- RES 3: 5285.00 High Apr 10

- RES 2: 5213.25 High Apr 15

- RES 1: 5139.03/5154.25 20-day EMA / High Apr 29

- PRICE: 5089.50 @ 1527 ET Apr 30

- SUP 1: 5022.25/4963.50 Low Apr 25 / 19 and the bear trigger

- SUP 2: 4907.57 50.0% retracement of the Oct 27 ‘23 - Apr 1 bull leg

- SUP 3: 4863.75 Low Jan 19

- SUP 4: 4799.50 Low Jan 17

The S/T trend condition in S&P E-Minis remains bearish and the latest recovery appears to be a correction. The contract has recently traded through the 50-day EMA, signalling scope for a continuation lower. A resumption of the bear leg would open 4907.57, a Fibonacci retracement. Firm resistance at 5139.03, the 20-day EMA, has been pierced, a clear break would instead signal a reversal and expose key resistance at 5333.50, the Apr 1 high.

COMMODITIES Strong USD Weighs On Gold, Crude Set for Losses

- Crude is heading for US close trading lower amid a stronger US dollar due to the firmer-than-expected U.S. economic data. An easing geopolitical risk premium adds further pressure.

- WTI Jun 24 is down 1.0% at $81.8/bbl.

- For now, WTI futures remain above key short-term support at $81.22, the 50-day EMA. Key resistance and the bull trigger has been defined at $86.97, the Apr 12 high.

- The firmer USD and rise in US yields weighed on gold Tuesday, ahead of tomorrow’s FOMC decision.

- Spot gold is down 1.9% at $2,291/oz, trimming what is set to be a third consecutive month of gains.

- The 20-day EMA has given way, signalling scope for an extension towards the 50-day EMA at $2,239.9.

- ETF holdings continue to pull lower, with related participants continuing to trim exposure during the rally from the early October lows.

- Meanwhile, silver is underperforming, down 2.9% on the day at $26.3/oz, lifting the gold/silver ratio back to its highest since early April.

- Copper is also down by 2.4% to $456/lb, the first decline in five sessions.

- A bullish theme in copper futures remains intact, with scope seen for $477.04 a Fibonacci projection. Key support is seen at $420.54, the 50-day EMA.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/05/2024 | 2300/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

| 01/05/2024 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 01/05/2024 | 0830/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 01/05/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 01/05/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 01/05/2024 | - | *** | | US | Domestic-Made Vehicle Sales |

| 01/05/2024 | 1215/0815 | *** | | US | ADP Employment Report |

| 01/05/2024 | 1230/0830 | *** | | US | Treasury Quarterly Refunding |

| 01/05/2024 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/05/2024 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 01/05/2024 | 1400/1000 | * | | US | Construction Spending |

| 01/05/2024 | 1400/1000 | *** | | US | JOLTS jobs opening level |

| 01/05/2024 | 1400/1000 | *** | | US | JOLTS quits Rate |

| 01/05/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 01/05/2024 | 1800/1400 | *** | | US | FOMC Statement |

| 01/05/2024 | 2015/1615 |  | CA | BOC Governor at Senate Banking Committee |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.