Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MN FED KASHKARI: NEED TO GET MORE DATA ABOUT ECONOMY; POSSIBLE MILD RECESSION WOULD BRING INFLATION DOWN; IF INFLATION STAYS HIGH, MAY NEED TO KEEP RATES HIGHER, Bbg

- US TREASURY ASKS AGENCIES IF PAYMENTS CAN BE MADE LATER: Washington Post

- US: Debt Ceiling Talks Resume - Parties Still "Far Apart"; McCarthy: "We Are Nowhere Near A Deal" vs. "We Could Still Finish This By June 1"

- REPUBLICAN NEGOTIATOR GRAVES: I DON'T THINK THINGS ARE GOING WELL' OVER DEBT CEILING TALKS

- DEMOCRAT NEGOTIATOR JEFFRIES: NOT A LOT OF PROGRESS TOWARD RESOLUTION HAS BEEN MADE

- DALLAS FED LOGAN: TECH DISRUPTION ‘QUITE VISIBLE' IN FINANCE; SPEED OF TRANSACTIONS HAS HIGHLIGHTED NEED TO MANAGE LIQUIDITY RISKS; EVERY BANK SHOULD BE READY TO BORROW FROM THE FED

- FLORIDA GOV DESANTIS TO ANNOUNCE HIS CANDIDACY FOR 2024 REPUBLICAN PRESIDENTIAL NOMINATION WEDNESDAY -NBC

Key Links:MNI INTERVIEW: Fed Must Hike Rates To 6%, Maybe 7%-Ex-Staffer / May FOMC Minutes Preview: June Pause Potential In Focus / MNI US: White House Negotiators Depart Capitol After Two-Hour Debt Limit Talks / MNI BRIEF: 'Several' More ECB Rate Hikes Needed - Buba's Nagel / US Treasury Auction Calendar

US TSYS: Debt Ceiling Talks Remain Deadlocked; Curves Extend Inversion

Rates extended modest session highs in a late risk-off move as White House debt ceiling negotiators departed the capitol. Stocks extended session lows (SPX Eminis tap 4154.50) in turn as no resolution to avoid default somewhere on or after June 1 yet reached.

- Treasury Jun'23 10Y futures marked a session high of 113-22 (+7), while yield slipped to 3.6861% low, scaling back to 113-18 amid reports that negotiators will resume talks this evening.

- Short end continued to underperform, Jun'23 2Y futures -2 at 102-15.12; 2s10s curve -3.574 at -64.273 - amid higher market expectation of a near-term default.

- Separately, Fed Chairman Powell has left the New Democrat Coalition lunch recently, lack of notable headlines from the closed door meeting other than to note debt-ceiling was not part of the discussion.

- Despite the bounce, Treasury futures bear cycle extends. The break of 113-30+ last week, the Apr 19 low and a key support, has strengthened a bearish theme. Today’s move lower opens 112-30 next, a Fibonacci retracement.

- On the upside, initial resistance is seen at 113-30+ ahead of the 50-day EMA, at 114-25. A break of the average is required to signal a potential reversal.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00205 to 5.09996 (+.00623/wk)

- 3M +0.01532 to 5.16617 (+.00270/wk)

- 6M +0.02418 to 5.16336 (+.01683/wk)

- 12M +0.02638 to 4.91373 (+.03607/wk)

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00400 to 5.06614%

- 1M +0.01114 to 5.13800%

- 3M +0.02115 to 5.39586% */**

- 6M +0.04943 to 5.50429%

- 12M +0.09114 to 5.52214%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.39586% on 5/23/23

- Daily Effective Fed Funds Rate: 5.08% volume: $124B

- Daily Overnight Bank Funding Rate: 5.06% volume: $290B

- Secured Overnight Financing Rate (SOFR): 5.05%, $1.434T

- Broad General Collateral Rate (BGCR): 5.02%, $580B

- Tri-Party General Collateral Rate (TGCR): 5.02%, $572B

- (rate, volume levels reflect prior session)

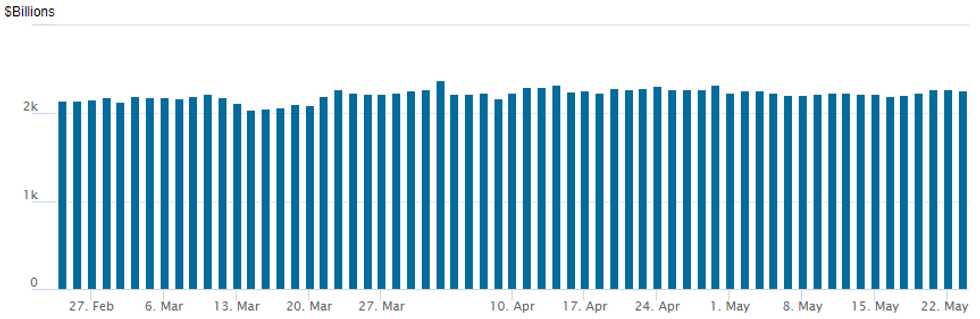

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,256.689B w/ 102 counterparties, compares to prior $2,275.311B. Compares to high usage for 2023: $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTIONS SUMMARY

Consistently better low delta put and put spread trade reported in SOFR options Tuesday, in line with heavy selling through mid-2024 futures as projected rate cuts through year end continue to evaporate (pricing in slightly higher than 25bp cut by the Dec 13 FOMC). Treasury options, on the other hand, centered on upside calls even before underlying futures rallied as debt ceiling negotiations remained deadlocked.- SOFR Options:

- Block, 5,000 SFRH4 93.75/94.50 2x1 put spds, 2.5

- Block, 5,000 2QM3 96.25/96.50 put spds, 3.5 ref 96.885

- +10,000 SFRM3 94.56/94.62 put spds, 1.0

- 3,000 SFRM3 94.43/94.50/94.68/94.75 put condors ref 94.78

- 6,000 SFRN3 94.62/94.81 put spds, ref 94.95

- 4,000 OQM3 95.31/95.75/96.03 put flys ref 96.16

- 3,000 OQM3 95.81/96.00/96.25 broken put trees, ref 96.14 to -.145

- 2,250 OQM3 96.18/96.43 2x1 put spds ref 96.185

- 2,500 OQM3 96.18 puts, ref 96.185

- 4,500 OQM3 96.12 puts, 19.0 ref 96.185

- Treasury Options:

- 2,000 FVN3 109.25/110.5 1x2 call spds , 1 net ,2-leg over ref 109-03

- 3,000 FVM3 108.5/109 call spds, 8 ref 108-12.25

- 3,700 TYM3 113.75/114 call spds, 7 ref 113-07

- 2,000 TUN3 103.5 calls, 14.5 ref 103-01.5

- Block, 5,000 FVM3 109.5/110 call spds, 1 ref 108-12.5/0.04%

- over 8,700 FVM3 108 puts, 8 ref 108-12.75

- 1,500 TYN3 117/119/120 broken call flys, 7 ref 113-30.5

- over 10,000 TYN3 118 calls, 12 ref 114-06.5

- 1,500 TYN3 116/117 call spds, 11 ref 114-05.5

- 1,500 TYM3 114.5/115.5 call spds ref 113-13.5

- 2,000 TYM3 114.25 calls, 7 ref 113-14

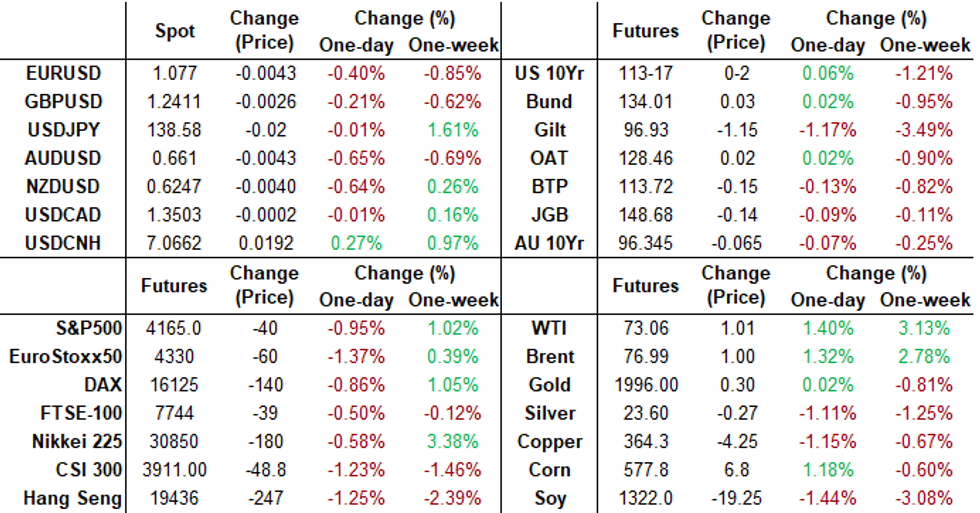

EGBs-GILTS CASH CLOSE: Gilts Lead Rout

Gilts led a global core FI rout Tuesday, with UK yields rising 8-9bp across the curve.

- The Gilt sell-off was not due to a single factor: partly in anticipation of Wednesday's CPI release, and partly on prelim May services PMI which slipped to a 2-month low but held hawkish details.

- Terminal BoE pricing rose as much as 13bp to 5.13%, before fading.

- Weakness in the German curve was relatively tame, with yields up 0-1bp. Like the UK's PMI report, Eurozone manufacturing came in weak, but services were probably too strong for the ECB's comfort.

- Eurozone central bank speakers had little impact: BoE's Bailey had little new to say, while the largest mover was Monday's hawkish-leaning after hours comments by ECB's de Cos who said there was still a way to go on rate hikes.

- Following Monday's strong rally led by Greece, periphery spreads were mixed/unchanged.

- UK inflation leads Wednesday's docket, but we also get German IFO, Bund and Gilt supply, and appearances by Bailey and ECB's Lagarde.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.3bps at 2.822%, 5-Yr is up 0.3bps at 2.451%, 10-Yr is up 1bps at 2.469%, and 30-Yr is up 0.8bps at 2.642%.

- UK: The 2-Yr yield is up 8.2bps at 4.135%, 5-Yr is up 8.8bps at 3.991%, 10-Yr is up 9.4bps at 4.158%, and 30-Yr is up 8.1bps at 4.533%.

- Italian BTP spread down 0.3bps at 185.2bps / Greek down 0.4bps at 141.4bps

EGB Options: Upside Plays Gain Steam As Rates Sell Off

Tuesday's Europe rates / bond options flow included:

- OEM3 117.5/116.75/116p fly, sold at 30.5 in 2k

- RXQ3 124.50p, bought for 10 in 5k

- RXQ3 137/140 call spread, paper paid 36 on 15K, covered via 1,650 RXU3 futures at 132.85, 11% delta

- ERZ4 99.25/100.00cs 1x2, is now bought for half in 10k. This was bought last week for flat in 45k, suggest 55k total now

FOREX: Greenback Firms Amid Weakness In Equities, NZD Falls 0.6% Ahead of RBNZ

- Despite the US dollar whipsawing throughout US hours, the DXY sits 0.3% firmer as we approach the APAC crossover. The moderate greenback strength is in line with weaker major equity benchmarks as e-mini S&P futures extend their decline to 1%.

- Antipodean FX sits bottom of the G10 pile, with both Aussie and Kiwi seen down around 0.6%. The move for NZDUSD comes ahead of Wednesday’s RBNZ decision where MNI believe that the RBNZ can afford to step down to a 25bp hike as inflation and inflation expectations are moving in the right direction and policy is now restrictive. However, with inflation elevated and demand robust, the RBNZ is still likely to tighten further and keep its tightening bias.

- EURUSD (-0.30%) has also moved south on Tuesday, although last Friday’s low at 1.0760 has acted as solid support up to this point. Overall, following the break of the 50-day EMA, at 1.0879, EURUSD has strengthened bearish conditions, signalling scope for a continuation lower towards 1.0737 next, a Fibonacci retracement. Clearance of this level would place the focus on 1.0713, the Mar 24 low. A firm resistance is now seen at 1.0899, the 20-day EMA.

- USDJPY sits close to unchanged on the session, although the pair has registered a new multi-month high at 138.91, placing the pair briefly at the best levels since November 2022.

- Looking ahead, UK April CPI will precede German IFO data, both due to cross the wires on Wednesday. The focus for the US docket will be on the FOMC minutes. Attention will then be on any revisions to Q1 growth data and US Core PCE Price Index data due later in the week.

FX: Expiries for May24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0750(E953mln), $1.0830-40(E732mln)

- USD/JPY: Y138.25($500mln)

- GBP/USD: $1.2320-25(Gbp501mln)

- AUD/USD: $0.6610(A$555mln), $0.6695-00(A$835mln)

Late Equity Roundup: Slipping Lower

Stocks trading weaker, near late session lows as it looks like another day will pass with no resolution to the impending Debt Ceiling "x" date where the US will be in default on or around June 1. That said, negotiations will likely resume this evening.

Currently, S&P E-Mini futures are down 41.25 points (-0.98%) at 4163.5; DJIA down 175.34 points (-0.53%) at 33111.85; Nasdaq down 141.3 points (-1.1%) at 12580.

- Leading gainers: Energy sector continues to outperform as WTI crude holds moderate gains (+0.86 at 72.91) with oil & gas refiners well bid (Chevron +2.70%, Occidental +1.85%, Exxon +1.70%, Marathon +1.15%).

- Laggers: Materials, Information Technology and Communication Services sectors underperforming, software and services providers weighing on the latter (ORCL -2.90%, ADSK -2.80%, SNPS -2.05%).

- For a technical point of view, S&P E-minis trend needle continues to point north and today’s pullback is considered corrective. The contract traded higher last week and breached key resistance and the bull trigger at 4206.25, the May 1 high. Clearance of this level confirms an extension of the bull trend from Mar 13 and opens 4244.00, Feb 2 high and the next important resistance.

- On the flipside, key support is 4062.25, May 4 low. Initial support lies at 4156.44, the 20-day EMA.

E-MINI S&P TECHS: (M3) Corrective Pullback

- RES 4: 4288.00 High Aug 19 2022

- RES 3: 4244.00 High Feb 2 and a medium-term bull trigger

- RES 2: 4231.00 High Feb 3

- RES 1: 4227.25 High May 19

- PRICE: 4161.00 @ 1525ET May 23

- SUP 1: 4156.44 20-day EMA

- SUP 2: 4123.13/4062.25 50-day EMA / Low May 4 and key support

- SUP 3: 4052.50 Low Mar 30

- SUP 4: 4022.75 50.0% retracement of the Mar 13 - May 1 bull leg

The S&P E-minis trend needle continues to point north and today’s pullback is considered corrective. The contract traded higher last week and breached key resistance and the bull trigger at 4206.25, the May 1 high. Clearance of this level confirms an extension of the bull trend from Mar 13 and opens 4244.00, Feb 2 high and the next important resistance. Key support is 4062.25, May 4 low. Initial support lies at 4156.44, the 20-day EMA.

COMMODITIES: Oil Boosted By OPEC+ Supply Risks

- Despite fading in recent trade, crude oil has seen solid gains today with both Brent and WTI earlier testing resistance levels. OPEC+ supply risks support prices, which have mostly remained resilient to some renewed souring in debt ceiling talks on GOP comments later in the session with equities also sliding.

- Comments from the Saudi Energy Minister Prince Abdulaziz bin Salman early today for oil speculators to watch out have added to upside risks with OPEC+ production intentions uncertain ahead of the ministerial meeting on 3-4 June.

- Further on the supply side, the Russian government is considering a gasoline export ban to prvent domestic fuel shortgaes and prices inceases after a decision to reduce subsidies for refineries, industry and government sources told Reuters.

- WTI is +1.6% at $73.17 having come close to key short-term resistance at $73.81 (May 10 high) after which lies $76.74 (Apr 28 high).

- Brent is +1.4% at $77.09 having briefly spiked to $77.58 off $77.60 (May 10 high) after which lies $78.63 (50-day EMA).

- Gold is +0.2% at $1975.82, gaining later in the session off lows of $1954.33 as Tsy yields have slipped intraday. Resistance is seen at the 20-day EMA of $1996.4.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/05/2023 | 2301/0001 | * |  | UK | XpertHR pay deals for whole economy |

| 24/05/2023 | 0200/1400 | *** |  | NZ | RBNZ official cash rate decision |

| 24/05/2023 | 0600/0700 | *** | | UK | Consumer inflation report |

| 24/05/2023 | 0600/0700 | *** | | UK | Producer Prices |

| 24/05/2023 | 0800/1000 | *** |  | DE | IFO Business Climate Index |

| 24/05/2023 | 0830/0930 | * | | UK | ONS House Price Index |

| 24/05/2023 | 0930/1030 | | UK | BOE Bailey Keynote Speech at Mansion House Net Zero Summit | |

| 24/05/2023 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 24/05/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 24/05/2023 | 1230/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 24/05/2023 | 1300/1500 | ** |  | BE | BNB Business Sentiment |

| 24/05/2023 | 1300/1400 | | UK | BOE Bailey Frieside Chat at WSJ CEO Council Summit | |

| 24/05/2023 | 1405/1005 | | US | Treasury Secretary Janet Yellen | |

| 24/05/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 24/05/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 24/05/2023 | 1610/1210 | | US | Fed Governor Christopher Waller | |

| 24/05/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 5 Year Note |

| 24/05/2023 | 1745/1945 |  | EU | ECB Lagarde Opens Anniversary of ECB Event | |

| 24/05/2023 | 1800/1400 | * | | US | FOMC Statement |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.