Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI SECURITY: US Official: US Remains "Very Open" To Diplomacy With North Korea

- MCCONNELL SAYS SENATE WILL WORK TO KEEP GOVERNMENT OPEN, Bbg

- UAW Threatens to Strike More Auto Plants Friday If No Progress, Bbg

- BIDEN TO HOST TOP EU OFFICIALS FOR SUMMIT IN WASHINGTON ON OCT 20, WITH STEEL TARIFFS AMONG ISSUES TO RESOLVE - SENIOR EU OFFICIAL, Rtrs

cropfilter_vintageloyaltyshopping_cartdelete

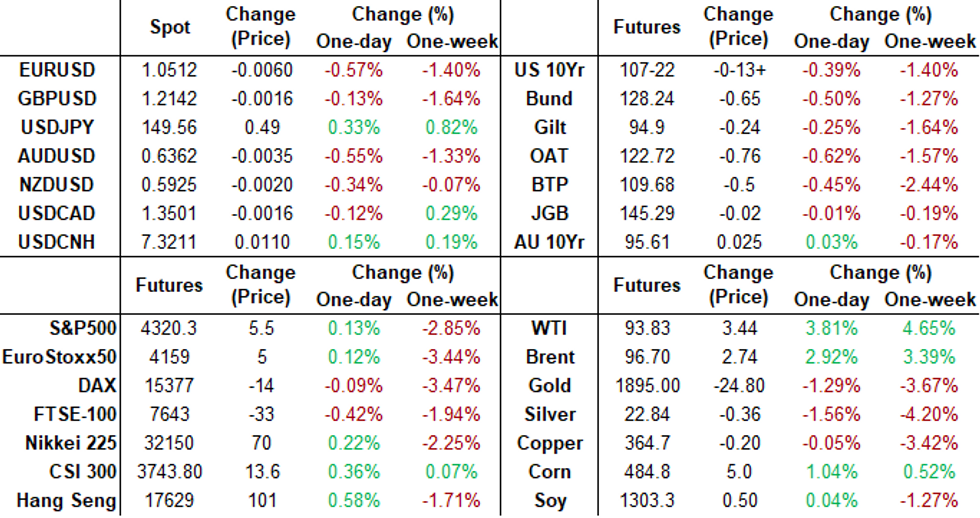

US TSYS Brief Post-Auction Support, Fed Speak Remains Hawkish, Strong 5Y Sale

- Treasury futures weaker, near late session lows after bounce on strong 5Y note auction (4.659% vs. 4.672% WI) proved short lived. Dec'23 10Y futures through technical support to 107-15.5 (-20), puts focus on 107-05+ 1.382 proj of the Jul 18 - Aug 4 - Aug 10 price swing.

- Curves bear steepening again, 3M10Y +8.096 to -87.514, 2Y10Y +6.767 at -52.175 (steepest since mid-May 2023).

- Rates actually extended highs after Core durable goods orders came out stronger than expected in August preliminary data, rising 0.9% M/M (cons 0.1) but with the gloss taken off by a sizeable downward revision to -0.4% M/M (initial 0.1) in July.

- Little (or perhaps a delayed) reaction to MN Fed President Kashkari making the rounds again this morning (CNN, CNBC), reprising higher for long stance if inflation persists: "holding rates through 2024" (despite dots showing a cut next year).

- Cross asset summary: Greenback near highs (DXY +.426 at 106.657), Gold weaker (-24.5 at 1876.15), crude broadly higher (WTI +3.40 at 93.79) and stocks bounced after Senate Leader McConnell headlines re: avoiding a Govt shutdown: DJIA is down DJIA is down 56.82 points (-0.17%) at 33564.46, S&P E-Mini Future down 0.25 points (-0.01%) at 4315.25, Nasdaq up 27.7 points (0.2%) at 13092.47.

- Thursday focus: Weekly Claims, GDP, PCE, Fed Speakers inclding Chairman Powell, 7Y Note Sale.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M -0.00235 to 5.31608 (-0.00143/wk)

- 3M +0.00450 to 5.39008 (-0.00973/wk)

- 6M +0.00422 to 5.46749 (-0.01206/wk)

- 12M +0.00936 to 5.46909 (-0.01654/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $96B

- Daily Overnight Bank Funding Rate: 5.32% volume: $260B

- Secured Overnight Financing Rate (SOFR): 5.31%, $1.561T

- Broad General Collateral Rate (BGCR): 5.30%, $568B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $555B

- (rate, volume levels reflect prior session)

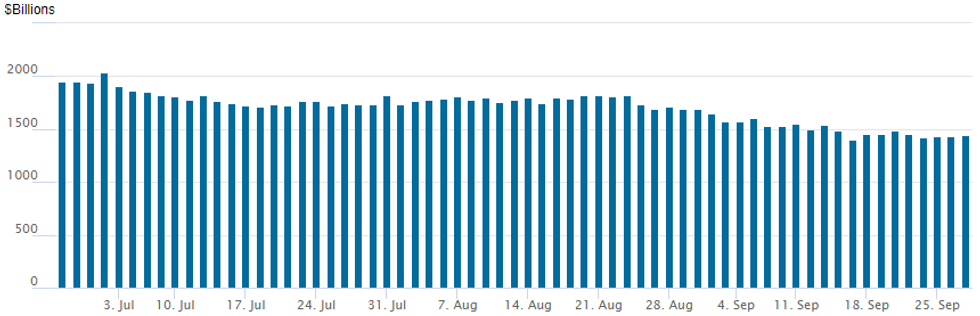

FED REVERSE REPO OPERATION

Repo operation up to 1,442.805B w/100 counterparties, compared to $1,438.301B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

SOFR and Treasury option trade remained mixed on decent volumes Wednesday as underlying futures reversed early support, 10Y yields extending new 16Y high of 4.6404%. Rate hike projections into early 2024 bounced amid continued hawkish Fed messaging: November at 22.8% w/ implied rate change of +6.2bp to 5.390%, December cumulative of 12.2bp at 5.449%, January 2024 13.5bp at 5.463%. Fed terminal at 5.46% in Feb'24.

- SOFR Options:

- Block, 40,000 SFRF4 94.00/94.25 2x1 put spds, 0.25-0.5 net ref 94.575

- Block, 12,000 0QH4 97.25 calls, 5.5 ref 95.62

- Block, 40,000 SFRZ3 96.0 combo, 145.75 net vs. 94.53/100% - parity play, more on screen

- 7,650 SFRZ3 94.25/94.32/94.38/94.43 put condors, 1.25

- 3,000 SFRF4 94.62/94.75/94.87/95.00 call condors ref 94.62

- 3,500 SFRH4 94.75/94.87/95.00/95.12 call condors ref 94.62

- 1,500 0QV3 95.25 puts vs. 0QV3 95.62/95.87 call spds on 1x2 basis, ref 95.395

- Treasury Options:

- 7,500 FVZ3 105/106/106.75/108.25 broken call condors, 18.5

- -10,500 TYX 108/109.5 call spds 35 vs. 107-30.5/0.24%

- Block, 13,000 TYZ3 104 puts 17 vs. 107-27/0.15%

- 6,000 TYX3 109.5/111/112 1x3x2 broken call flys

- -5,000 TYX3 107/110 strangles, 43

- over 3,700 USX3 114 puts, 122 last

- over 4,500 TYZ3 113 calls, 9 last

- 3,000 TYZ3 108/109.5 put spds ref 108-14

- 2,500 FVX3 105.5/106.5 call spds ref 105-13.5

- 3,700 TYZ3 113/115 call spds ref 108-14

EGBs-GILTS CASH CLOSE: German Long-End Yields Hit Post-2011 Highs

European core yields closed on the highs Wednesday after an afternoon selloff in sympathy with US Treasuries.

- The bellies of the German and UK curves underperformed, with Bobl yields at a post-March high.

- 10Y and 30Y German yields started the day constructively but after a sell-off in the last 2 hours of trade alongside Tsys (but with no particular catalyst) closed at a new post-2011 high. UK rates sold off but in contrast the curve move was more of a bear flattening motion.

- Peripheral spreads widened amid anxiety over the Italian government's deficit forecasts due to be released after the cash close, and a broader risk-off move (equities down once again).

- Data was 2nd tier, with Euro money supply contracting more quickly than expected in August, while German and French consumer confidence was a little soft but basically in line. ECB's Elderson told MNI that policy rates have not necessarily peaked.

- MNI hosts an event with BoE's Hauser Thursday morning; we also get appearances by ECB's Holzmann and BoE's Greene.

- The September flash inflation round unofficially begins at 0630UK time Thursday with Germany's North Rhine Westphalia setting the tone for the rest of the prints through Friday morning, including Spain and the German national number Thursday. Our preview is here (PDF).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.3bps at 3.244%, 5-Yr is up 4.1bps at 2.812%, 10-Yr is up 3.5bps at 2.843%, and 30-Yr is up 2.9bps at 3.033%.

- UK: The 2-Yr yield is up 6.6bps at 4.874%, 5-Yr is up 7.4bps at 4.472%, 10-Yr is up 3.2bps at 4.358%, and 30-Yr is down 1.2bps at 4.793%.

- Italian BTP spread up 1.1bps at 194.5bps / Greek up 3.3bps at 153.3bps

EGB Options: Mixed Midweek Trade

Wednesday's Europe rates/bond options flow included:

- 0RX3 96.625 straddle sold at 26.5 in 3k

- 0RZ3 96.87/97.12/97.37c fly, bought for 2.75 and 3 in 4k

- ERU4 96.25/95.75 1x2 put spread bought for 5.25 in 2k

- DUX3 105.20/105.50/105.70c fly, bought for 4.5 in 2k

- RXX3 131/132cs, bought for 18.5 and 19 in 10k

- RXX3 125.00/122.50ps 1x1.5, bought for 8.5 in 2.5k

- RXX3 129.50/130.50cs vs 128.50p bought the cs for -46 and -48 (receive) In 4k.

FOREX: Single Currency Continues to Spiral, EUR/USD Downtrend Cemented

- The single currency was the poorest performing currency in G10 Wednesday, sliding against all others to retain the solid downtrend in EUR/USD. The pair traded to a fresh cycle low of 1.0509, to extend the recent clearance of 1.0632.

- Sights are on 1.0484 next, the Jan 6 low. Moves in the EUR come ahead of the September preliminary CPI estimate due on Friday, at which markets expected headline inflation to dip below 5.0% for the first time since late 2021.

- NOK sits at the other end of the table, with the strength in oil markets remaining the primary driver. The prompt WTI crude spread rallied to its highest in over a year, lending further support to oil-tied currencies and putting the NOK at the top of the table. EURNOK is has breached the 11.40-11.60 range that has contained the pair since mid-August, meaning the 200-day EMA at 11.2735 provides the next key support. The NOK bid also allows NOKSEK to retrace yesterday's downtick, with the cross rising by ~0.7% today.

- The medium-term uptrend across the greenback continues to dominate, with concerns surrounding a possible US government shutdown at top of mind. Fed's Kashkari spoke to say that near-term economic risks from a shutdown could force the Fed to "do less" on policy than might otherwise be the case, leaving markets watching politics and Capitol Hill for any further developments. Fed's Powell hosts a town hall with educators on Thursday, at which the Q&A will be watched for any comments on policy.

- Focus Thursday turns to regional German CPI data, ahead of a national print expected to show inflation at 4.5% for the Y/Y EU harmonized release. From the US, weekly jobless claims and the tertiary read for Q2 GDP also cross.

FX Expiries for Sep28 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0600(E593mln), $1.0665-70(E910mln)

- USD/JPY: Y144.90-00($1.2bln), Y145.70-76($2.0bln), Y146.60($1.5bln), Y147.50-70($1.2bln)

- GBP/USD: $1.2000(Gbp1.2bln), $1.2200(Gbp1.4bln) EUR/GBP: Gbp0.8640(E770mln)

- AUD/USD: $0.6600(A$782mln), $0.6650(A$832mln), $0.6685(A$521mln)

- USD/CAD: C$1.3450($682mln), C$1.3530-35($561mln)

- USD/CNY: Cny7.3070($1.1bln)

Late Equity Roundup: Stocks Bounce on Hopes Gvt to Avoid Shutdown

- The continued sell-off in stocks to new cycle lows caught a reprieve late Wednesday, bouncing back to near session open levels after headlines from Senate Leader McConnell said the "SENATE WILL WORK TO KEEP THE GOVERNMENT OPEN". Whether a spending bill is passed before the US Gvt runs out of capital this weekend remains to be seen - but algos took it as a green light to start buying stocks. Currently, the DJIA is down 53.7 points (-0.16%) at 33569.34, S&P E-Mini Future up 0.25 points (0.01%) at 4315.75, Nasdaq up 37.4 points (0.3%) at 3102.75.

- Leaders: Energy, Industrials and Communication Services continued to outperform in late trade, equipment and service providers buoyed the former: Haliburton +3%, Schlumberger +2.8%, Baker Hughes +1.7%.

- Meanwhile, Capital goods shares, particularly construction and engineering, supported Industrials: Generac +6.6%, Carrier Group +4.45%, Axon +3.05%. Media and entertainment names buoyed Communications sector: Warner Bros +3.5%, Paramount +2.95%, Interactive Group +1.7%.

- Laggers: Utilities, Consumer Staples and Health Care sectors underperformed, electric and water providers weighed on the former: NextEra Energy -7.95% (adding to -2% decline Tue after cutting growth outlook), American Water Works -2%, NiSource -1.7%.

- Consumer Staples weighed by household and personal products makers: Kenvue -1.8%, Kimberly-Clark -1.3%, Colgate Palmolive -1.4%. Pharmaceuticals and biotech shares reversed prior session support, weighing the Health Care sector: Organon -3.25%, Viatris -1.5%, Merck -1.2%.

E-MINI S&P TECHS: (Z3) Trend Needle Points South

- RES 4: 4597.50 High Sep 1 and a near-term bull trigger

- RES 3: 4566.00 High Sep 15

- RES 2: 4485.10 50-day EMA

- RES 1: 4399.00 High Sep 22

- PRICE: 4320.00 @ 1515 ET Sep 27

- SUP 1: 4300.62 50.0% retracement of the Mar 13 - Jul 27 bull cycle

- SUP 2: 4277.00 Low Sep 27

- SUP 3: 4259.00 Low May 31

- SUP 4: 4242.15 1.236 proj of the Jul 27 - Aug 18 - Sep 1 price swing

A bear cycle in S&P E-minis remains in play and the contract traded lower Tuesday, extending the current downleg. Last Thursday’s sell-off resulted in a break of support at 4397.75, the Aug 18 low. This breach reinforced bearish conditions and signals scope for a continuation lower. Sights are on 4300.62, a Fibonacci retracement point. Initial firm resistance is 4485.10, the 50-day EMA. Short-term gains would be considered corrective.

COMMODITIES WTI Surges Further As Stocks Near Operational Lows, Gold Slumps With USD Bid

- Crude markets have seen particularly strong gains, extended after a below expected crude draw (-2,169 vs exp -600) and another drop in Cushing stocks. Crude inventories at Cushing fell for the seventh week with a draw of 943k this week taking stocks to the lowest since July 2022, getting close to the operational low of 20mbbls.

- Premiums for near term WTI will continue their rally unless Cushing stocks see substantial builds, according to Bloomberg.

- Crude inventories in the European ARA region fell -1.025mbbls in the week ending 22 Sep according to the latest Genscape data.

- BofA has raised its Brent crude oil forecast for the second half of this year to average $91/bbl, from $81/bbl previously, as the recent run up in refining margins has helped to support prices, together with the extension to OPEC+ supply cuts.

- WTI is +3.7% at $93.78 off its high of $94.17 that has cleared the bull trigger at $92.43 (Sep 19) before a Fibo projection at $93.31 to next open the round $95.

- Brent is +2.9% at $96.65 off a high of $97.06 to clear two resistance levels including $96.95 (Nov 14, 2022 high).

- Gold meanwhile is -1.2% at $1877.13, slumping under pressure from further strong USD increases to new YtD highs on the back of Treasury yields surging to fresh multi-year highs. It has pushed through two support levels including the bear trigger at $1884.9 (Aug 21 low), with a low of $1872.7 stopping short of next support at $1871.6 (Mar 13 low).

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/09/2023 | 0130/1130 | ** |  | AU | Retail Trade |

| 28/09/2023 | 0530/0730 | *** |  | DE | North Rhine Westphalia CPI |

| 28/09/2023 | 0700/0900 | *** |  | ES | HICP (p) |

| 28/09/2023 | 0800/1000 | ** |  | IT | ISTAT Business Confidence |

| 28/09/2023 | 0800/1000 | ** | | IT | ISTAT Consumer Confidence |

| 28/09/2023 | 0800/1000 | *** | | DE | Baden Wuerttemberg CPI |

| 28/09/2023 | 0800/1000 | *** | | DE | Bavaria CPI |

| 28/09/2023 | 0900/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 28/09/2023 | 0900/1100 | ** | | IT | PPI |

| 28/09/2023 | 0900/1100 | *** | | DE | Saxony CPI |

| 28/09/2023 | 0930/1030 |  | UK | BoE's Hauser Speaks at MNI | |

| 28/09/2023 | 1200/1400 | *** | | DE | HICP (p) |

| 28/09/2023 | 1230/0830 | *** |  | US | Jobless Claims |

| 28/09/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 28/09/2023 | 1230/0830 | * |  | CA | Payroll employment |

| 28/09/2023 | 1230/0830 | *** | | US | GDP |

| 28/09/2023 | 1300/0900 | | US | Chicago Fed's Austan Goolsbee | |

| 28/09/2023 | 1400/1000 | ** | | US | NAR Pending Home Sales |

| 28/09/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 28/09/2023 | 1445/1545 | | UK | BOE's Greene speaks on panel | |

| 28/09/2023 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 28/09/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 28/09/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 28/09/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 28/09/2023 | 1700/1300 | | US | Fed Governor Lisa Cook | |

| 28/09/2023 | 1900/1500 | *** |  | MX | Mexico Interest Rate |

| 28/09/2023 | 2000/1600 | | US | Fed Chair Jerome Powell | |

| 28/09/2023 | 2300/1900 | | US | Richmond Fed's Tom Barkin |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.