Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI FED: Powell Remains Confident On Housing Inflation

- MNI US: INDIA: US Gambles On India As Key Bilateral Partner

- MNI US: Treasury Sec Yellen To Lead US Delegation At EM Finance Summit Tomorrow

- MNI NATO: Blinken Encourages Turkish Counterpart To Ratify Sweden's Accession

- ECB'S NAGEL: 2% INFLATION GOAL CAN BE MET, STILL WAY TO GO .. DOESN'T SEE CREDIT CRUNCH, POLICY TRANSMISSION IS NORMAL, Bbg

US TSYS: FED Non-Voter Bostic Underpins Tsy Bid

- Treasury futures rebounded off midmorning lows, are drifting near the top end of the range with curves extending inversion: 2s10s marking -99.634 low.

- Second half support arrived after 20Y Bond auction re-open stopped through, strong auction drawing 4.01% high yield vs. 4.03% WI; 2.87x bid-to-cover vs. prior month's 2.56x.

- Meanwhile, Atlanta Fed Bostic (non-voter) supports holding the fed funds rate at the current 5%-5.25% target range and letting past rate increases work their way through the economy, adding the bar to justify further rate hikes is higher than it was a few months ago.

- Not too much of a reaction to Fed Chairman Powell semi-annual testimony to Congress earlier, reiterating talking points from last week's hawkish hold. He said last week's decision to hold rates steady for the first time since March 2022 reflected "how far and how fast we have moved," adding that future decisions will be made on a meeting-by-meeting basis.

- Chairman Powell reappears at Senate Banking Committee tomorrow at 1000ET.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00534 to 5.08247 (+.00618/wk)

- 3M +0.00888 to 5.22913 (+.02229/wk)

- 6M +0.00313 to 5.31173 (+.02235/wk)

- 12M -0.01681 to 5.24977 (+.01945/wk)

US DOLLAR LIBOR: Latest settlements:

- O/N -0.01258 to 5.06271%

- 1M -0.00657 to 5.14757%

- 3M +0.01928 to 5.53957% */**

- 6M +0.00843 to 5.68243%

- 12M +0.00071 to 5.89857%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.55743% on 6/12/23

- Daily Effective Fed Funds Rate: 5.07% volume: $134B

- Daily Overnight Bank Funding Rate: 5.06% volume: $295B

- Secured Overnight Financing Rate (SOFR): 5.05%, $1.427T

- Broad General Collateral Rate (BGCR): 5.03%, $625B

- Tri-Party General Collateral Rate (TGCR): 5.03%, $610B

- (rate, volume levels reflect prior session)

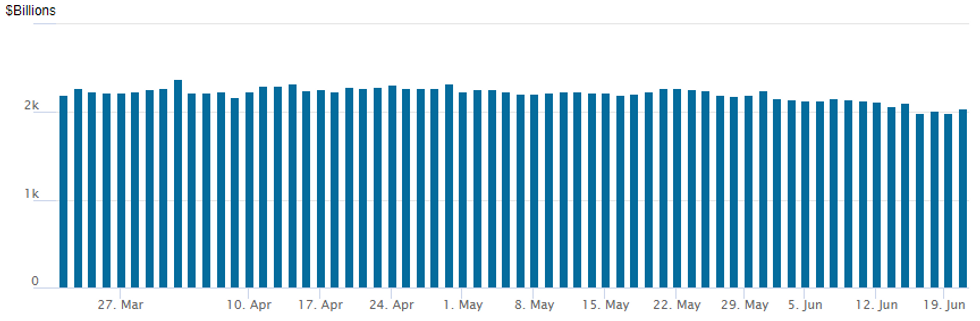

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage bounces to $2,037.102B w/ 106 counterparties, compared to $1,989.489B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTIONS SUMMARY

- In the lead-up to Chairman Powell's semi-annual policy testimony to Congress, the latest option trade includes better downside put positioning for two 25bp hikes by year end (put condor roll-down and Sep put fly with underlying SFRU3 trading 94.64. On the flipside, paper positioning for rate cuts in 2025 with long duration Green Mar'25, Sep'25 and Dec'25 upside call buying.

- SOFR Options:

- -7,500 SFRU3 94.25/94.75 put spds 11.0 over SFRH4 93.5/94.0/94.5 put flys at 1125:34ET

- -15,000 SFRZ3 94.50/94.75/95.00/95.25 put condors vs. 94.12/94.37/94.62/94.87 put condors

- +10,000 SFRU3 94.25/94.37/94.50 put flys, 2.25

- +2,000 SFRZ3 94.50/94.62/94.75 put flys

- -5,000 SFRH5 96.00/97.00 put over risk reversals 0.0 vs. 96.495/0.72%

- +15,000 SFRU5 97.50 calls, 45.0

- 3,000 SFRQ3 94.62/94.81 put spds, 12.5 ref 94.655

- Treasury Options:

- 4,000 FVQ3 109/110 call spds, 10 ref 107-29.5

- 3,000 TYQ3 110 puts ref 113-07

- 1,500 USU3 122/123 put spds, ref 127-30

- 1,200 FVN3/FVQ3 108.5/109/109.5 call fly spd

- 2,000 FVQ3 105.25/106/107.5 broken put fly on 2x3x1 ratio of 107-23.75

- -20,000 TYN3 112 puts, 2 ref 113-02.5

- 3,500 FVXN3 107.5 puts vs. 1750 FVQ3 107.25 puts, 6.5 net on the 2x1

- over 3,100 FVQ3 108 calls, 39.5-40.5

- 1,400 FVN3 108/108.25/108.5 call flys

- over 2,600 TYN3 113.5 calls, 15-11

- 2,000 TYN3 111.5/112.5 put spds 2 over TYN3 114 calls ref 113-01

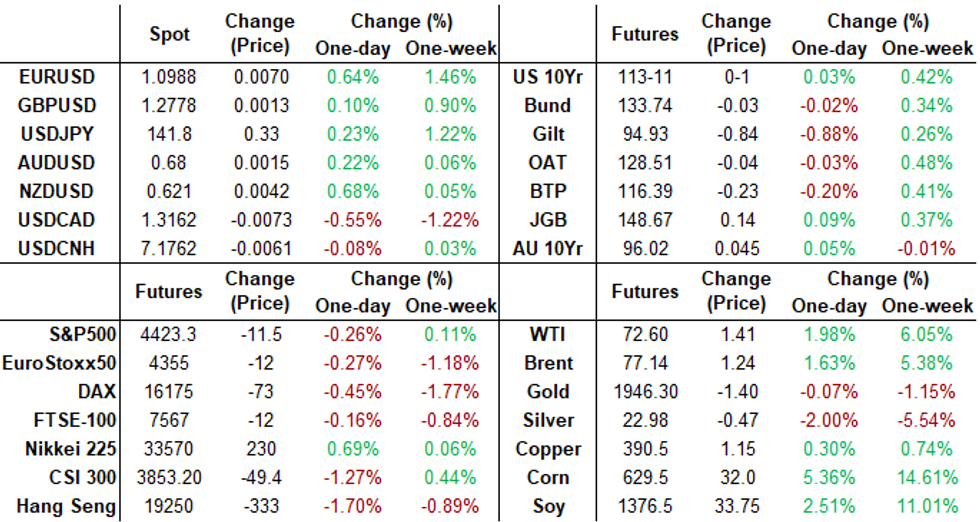

EGBs-GILTS CASH CLOSE: High UK CPI Hits Short-End Gilts Ahead Of BoE

Gilts bear flattened yet again Wednesday after a higher-than-expected UK inflation print pushed up Bank of England hike pricing for tomorrow and beyond.

- After core CPI came in at 7.1% (vs 6.8% survey), hike pricing for Thursday's BoE decision neared 50% of a 50bp (vs 25bp hike) before settling down (our preview published pre-CPI is here). Terminal Bank rate pricing remained above 6%.

- The UK cash curve in turn hit its flattest levels in post-open trade, partially reversing the move over the course of the session but ending up bear flatter on the day once again. 2s10s hit a fresh post-2000 low (-70.5bp before closing a little less inverted than that).

- Bunds easily outperformed Gilts, in turn, with the belly underperforming on the German curve.

- Periphery spreads tightened modestly, with Greece outperforming following a well-received GGB auction.

- Focus Thursday is of course on the BoE, though the SNB and Norges Bank decisions could also have an impact early in the session.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.6bps at 3.133%, 5-Yr is up 3.7bps at 2.562%, 10-Yr is up 3bps at 2.435%, and 30-Yr is down 0.6bps at 2.482%.

- UK: The 2-Yr yield is up 9.3bps at 5.046%, 5-Yr is up 8.2bps at 4.591%, 10-Yr is up 6.8bps at 4.405%, and 30-Yr is up 5.9bps at 4.513%.

- Italian BTP spread down 1bps at 161.6bps / Greek down 1.6bps at 130.4bps

EGB Options: Unwind In Sonia Upside Post-UK CPI Shock

Wednesday's Europe rates/bond options flow included:

- DUQ3 105.00/105.20/105.30/105.50c condor, bought for 4 in 2k

- RXQ3 129.00/127.00/126.50p ladder, bought for 4.5 and 5 in 7k

- SFIZ3 94.40/94.70 cs vs 94.00/93.70 ps, bought the ps for 4.25 in 2.5k (unwind)

FOREX: Volatile GBP Following CPI, BOE Decision Now Takes Focus

- An initial knee jerk higher for sterling, on the back of stronger than expected inflation, was quickly pared as markets weighed the potential impact of more aggressive tightening from the BOE going forward as well as short-term positioning adjustments ahead of tomorrow’s rate decision. GBPUSD traded as low as 1.2691 from a 1.2802 peak but late greenback weakness has seen the pair rise back to around 1.2775 ahead of the APAC crossover.

- GBPUSD technical bulls remain in the driver’s seat and short-term pullbacks are considered corrective. The rally last week confirmed a clear break of 1.2680, the May 10 high and a bull trigger. This strengthens bullish conditions and opens 1.2849, a Fibonacci projection.

- Elsewhere in G10, the Swedish Krona is the strongest performer, marking a swift reversal from the fresh all-time lows against the Euro on Tuesday. NZDUSD has also risen 0.75% on Wednesday.

- The modest greenback weakness in the aftermath of Fed Chair Powell’s semi-annual monetary policy report bolstered EURUSD to fresh six-week highs. The broad-based single currency strength also saw EURJPY print fresh trend highs and extend the move above the 155 mark. The 0.77% advance stands out in G10 fx, with the pair having recently confirmed a resumption of the longer-term uptrend. The focus remains on a material break of 155.59, a Fibonacci projection. 156.23 is the next topside target, the 2.00 projection of the Mar 20 - 21 - Apr 6 price swing.

- A packed central bank schedule on Thursday with the SNB, Norges Bank and the Bank of England all deciding on rates.

FX Expiries for Jun22 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0790-00(E1.8bln), $1.0845-55(E829mln), $1.0875(E674mln), $1.0900(E2.1bln), $1.1000-05(E748mln), $1.1045-50(E709mln)

- USD/JPY: Y138.48-50($1.4bln), Y141.00-20($1.3bln), Y142.00($903mln), Y142.50($760mln)

- AUD/NZD: N$1.1100(A$1.4bln)

- USD/CAD: C$1.3100-15($795mln), C$1.3200-10($755mln)

Late Equities Roundup

- Stocks turning lower late, Communication Services and Information Technology sectors underperformed stronger Energy sector shares as crude held midday gains (WTI +1.37 at 72.56).

- Otherwise, no specific headline driver as S&P E-Mini future trade down 23 points (-0.52%) at 4412.25, DJIA down 91.72 points (-0.27%) at 33963.04, Nasdaq down 140.9 points (-1%) at 13527.22.

- Despite the modest reversal, a bull theme in S&P E-minis remains intact and this week’s pullback appears to be a correction. Last week’s gains confirmed a resumption of the uptrend, marking an extension of the bull cycle that started in October 2022.

- The focus is on 4497.21, the top of a bull channel drawn from the Oct 2022 low (cont). Initial support is at 4381.75, the Jun 13 low. A firmer support lies at 4342.60, the 20-day EMA.

E-MINI S&P TECHS: (U3) Bullish And Sights Are on The Channel Top

- RES 4: 4576.72 2.50 projection of the May 4 - 19 - 24 price swing

- RES 3: 4556.71 2.382 projection of the May 4 - 19 - 24 price swing

- RES 2: 4532.08 2.236 projection of the May 4 - 19 - 24 price swing

- RES 1: 4497.21 Bull channel top drawn from the Oct 2022 low (cont)

- PRICE: 4415.00 @ 1545ET Jun 21

- SUP 1: 4381.75/4342.60 Low Jun 13 / 20-day EMA

- SUP 2: 4257.39 50-day EMA

- SUP 3: 4154.75 Low May 24

- SUP 4: 4098.25 Low May 4 and a key support

A bull theme in S&P E-minis remains intact and this week’s pullback appears to be a correction. Last week’s gains confirmed a resumption of the uptrend, marking an extension of the bull cycle that started in October 2022. The focus is on 4497.21, the top of a bull channel drawn from the Oct 2022 low (cont). Initial support is at 4381.75, the Jun 13 low. A firmer support lies at 4342.60, the 20-day EMA.

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/06/2023 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 22/06/2023 | 0730/0930 | *** |  | CH | SNB PolicyRate |

| 22/06/2023 | 0800/1000 | *** |  | NO | Norges Bank Rate Decision |

| 22/06/2023 | 0800/0400 |  | US | Fed Governor Chris Waller | |

| 22/06/2023 | 0915/1115 |  | EU | ECB Panetta Speech at Buba/ECB/Chicago Fed Conference | |

| 22/06/2023 | 1100/1200 | *** |  | UK | Bank Of England Interest Rate |

| 22/06/2023 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 22/06/2023 | 1100/1200 | *** | | UK | Bank Of England Interest Rate |

| 22/06/2023 | 1230/0830 | ** | | US | Jobless Claims |

| 22/06/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 22/06/2023 | 1230/0830 | * | | US | Current Account Balance |

| 22/06/2023 | 1400/1000 | *** | | US | NAR existing home sales |

| 22/06/2023 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 22/06/2023 | 1400/1000 | | US | Fed's Michelle Bowman, Loretta Mester | |

| 22/06/2023 | 1400/1000 | | US | Fed Chair Jerome Powell | |

| 22/06/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 22/06/2023 | 1430/1630 | | EU | ECB de Guindos at Financial Journalists' Roundtable | |

| 22/06/2023 | 1500/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 22/06/2023 | 1500/1100 | ** | | US | DOE Weekly Crude Oil Stocks |

| 22/06/2023 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 22/06/2023 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 22/06/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 22/06/2023 | 1900/1500 | | US | Atlanta Fed's Raphael Bostic | |

| 22/06/2023 | 2030/1630 | | US | Richmond Fed's Tom Barkin | |

| 23/06/2023 | 2300/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.