Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- MNI SECURITY: Pentagon-Russian Fighter Struck US Drone Which Came Down In Black Sea

- MNI FRANCE: PM Borne-A Majority Exists In Parliament For Pension Reform

- MNI US: Biden Pivot On Willow May Dull Impact Of GOP Energy Package

- MNI RUSSIA: Putin: "Russian Economy Stronger Than Anyone Thought"

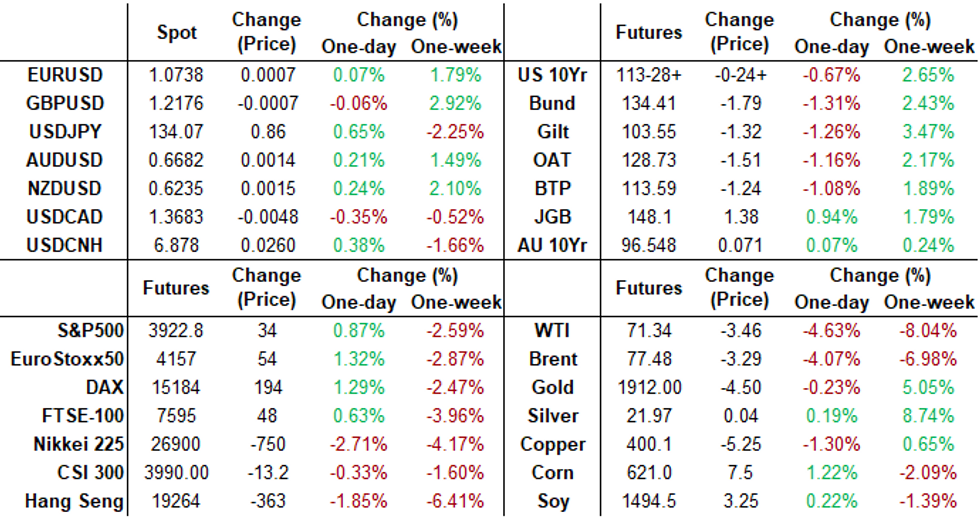

US TSYS: Yield Curves Off Lows, Bonds Weaker

Tsy yield curves have rebounded with Bond futures near lows after the bell, short end rates pare losses: Tsy 2s10s currently -15.988 -57.138, approximately 20bp off session lows.

- Little react to Feb CPI data: Core services ex OER and rent accelerate from 0.36 to 0.50% M/M, highest since September. 0.45% M/M if exclude total rent of shelter for same trend, fastest since Sep.

- Front-month 2Y note trading 103-00 (-13.12), 2Y yield at 4.2253% vs. 3.8367% overnight low (mid-Sep territory) as banking crisis concerns debatably moderated somewhat.

- Implied volatility drifting lower despite skittishness toward any contagion related headlines involving banks, however. Global rates gapped higher overnight after headlines flagged "material weakness" in financial reporting surrounding Credit Suisse - the bid reversed amid questions over how much the CS news has already been absorbed by markets. Latest from CS CEO: "SAYS FIRM SAW CLIENT INFLOWS ON MONDAY".

- Barring additional bank tied headline risk, next focus is on Wednesday's PPI data for February: MoM (0.7%, 0.3%); YoY (6.0%, 5.4%), Retail Sales Advance MoM (3.0%, -0.4%) and TIC flows in the afternoon.

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00243 to 4.55357% (-0.00357/wk)

- 1M +0.04328 to 4.72771% (-0.07086/wk)

- 3M +0.07471 to 4.94100% (-0.19714/wk)*/**

- 6M -0.08228 to 4.96843% (-0.45986/wk)

- 12M -0.15028 to 4.99229% (-0.74585/wk)

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.15371% on 3/9/23

- Daily Effective Fed Funds Rate: 4.58% volume: $41B

- Daily Overnight Bank Funding Rate: 4.56% volume: $232B

- Secured Overnight Financing Rate (SOFR): 4.55%, $1.148T

- Broad General Collateral Rate (BGCR): 4.52%, $467B

- Tri-Party General Collateral Rate (TGCR): 4.52%, $457B

- (rate, volume levels reflect prior session)

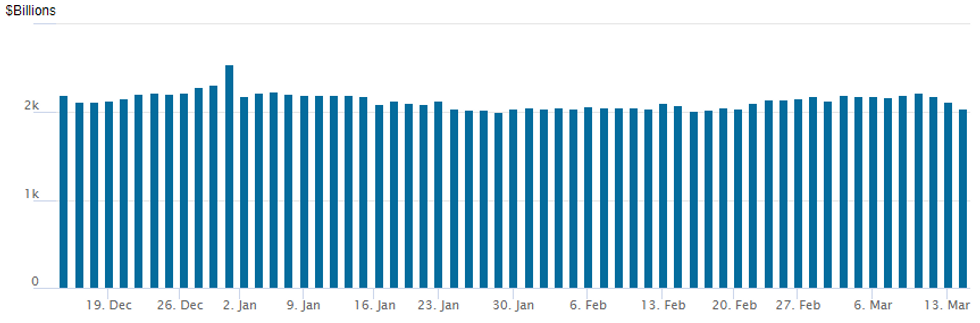

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage recedes to $2,042.579B w/ 95 counterparties vs. prior session's $2,126.677B. Compares to Friday, Dec 30 record/year-end high of $2,553.716B (prior record high was $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

Heavier block/cross volume remained mixed Tuesday: recent put buying looking for underlying to continue to reverse yesterday's banking crisis driven rally, call buyers looking for rebound on flat monetary policy guidance hopes.- SOFR Options:

- Block, 10,000 SFRK3 94.81/94.93 put spds, 5.0 vs. 95.31/0.05%

- Block, 26,000 SFRJ3 95.31/95.43 call spds, 5.0 vs. 95.235/0.06%

- 8,500 SFRJ3 94.87/95.25 put spds ref 95.615

- 7,500 SFRM3 95.31/95.43/95.56 call flys

- Block, 5,000 SFRU3 94.50 puts, 18.0 ref 95.37

- Block, 5,000 SFRN3 95.06/95.18/95.31 call flys, 0.75 ref 95.36

- Block, 13,000 SFRM3 97.75 calls, 4.0 ref 95.195

- Block, 6,000 SFRK3 94.37/94.50 put spds, 1.75 ref 95.15

- Block, 10,000 OQJ3 96.37 calls, 20.0 ref 96.06

- Block, 16,750 SFRN3 94.37 puts, 8.5 vs. 95.51/0.14%

- 65,000 SFRN3 93.87/94.12 put spds appr 2.5-3.0 ref 95.53

- Block/screen 10,000 2QJ3 96.00 puts, 9.0 ref 96.545

- 9,750 OQU3 97.37/97.50 call spds ref 96.465

- Block, 9,000 SFRJ3 94.25/94.37/94.50 put flys, 0.25 ref 95.38

- Block, 5,000 SFRJ3 94.81/95.00/95.18/95.37 put condors, 4.0 ref 95.37

- Block, 24,000 SFRZ3 94.50/95.00/95.50 put flys, 6.0 net ref 95.735

- 5,000 SFRU3 95.12/95.50 strangles, 90.5 ref 95.595

- Block, 3,000 SFRK3 94.50/94.87/95.25 put flys, 6.0 ref 95.42

- Block, 5,000 SFRK3 94.25/94.37 put spds, 1.25 ref 95.455

- Block, 10,000 SFRZ3 93.00/93.37put spds, 2.0 ref 95.855 to -.865

- Block, 10,300 SFRZ3 97.00/98.00 call spds, 19.5

- 6,000 SFRU3 97.25/98.50 3x5 call spds

- 4,000 SFRJ3 95.31/95.43 call spds ref 95.73

- 8,500 SFRJ3 94.87/95.25 put spds ref 95.615

- 8,500 SFRM3 95.31/95.43/95.56 call flys ref 95.685 to -.675

- Treasury Options:

- +7,000 TYM3 118 calls, 47

- +20,000 TYJ3 111.5/115.5 call over risk reversals, 3-41 vs. 113-16

- 2,000 USK3 123/126 put spds

- 10,000 FVJ3 109.5 calls, 16

- 5,000 TYJ3 111.5/115.5 strangles 27

- 5,000 TYJ3 116.5/118.5 call spds, 9

- over 5,000 TYM3 112/114 call spds ref 113-25.5

- 2,000 TYJ3 116/116.5 call spds ref 114-09.5

EGBs-GILTS CASH CLOSE: Yields Continue To Bounce

EGBs and Gilts sold off amid a risk asset relief rally Tuesday, as concerns over US banking stability abated vs the panic of the prior two sessions.

- Risk / swap spreads fell sharply, with periphery EGBs outperforming (10Y BTPs closed 8bp tighter to Bunds) as equities rallied.

- Bunds and Gilts fell to session lows after the highly anticipated US CPI reading was on the strong side, but traded sideways/higher for the rest of the session.

- The German curve bear flattened with Schatz yields up more than 20bp as ECB hike pricing continued to recover ground. A 50bp hike on Thursday is back to 70% probability, vs 30% at Monday's low.

- Expectations for a BoE hike later this month remain uncertain after this morning's mixed jobs data was not enough to sway the MPC in any particular direction: current implied pricing is about 65% for a 25bp hike vs a pause.

- Wednesday's Europe calendar highlight is the UK budget announcement - MNI's preview is here.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 20.2bps at 2.892%, 5-Yr is up 18.4bps at 2.512%, 10-Yr is up 16.1bps at 2.42%, and 30-Yr is up 13.4bps at 2.41%.

- UK: The 2-Yr yield is up 11.8bps at 3.481%, 5-Yr is up 11.5bps at 3.392%, 10-Yr is up 11.8bps at 3.488%, and 30-Yr is up 5.9bps at 3.894%.

- Italian BTP spread down 7.9bps at 184.5bps / Greek down 13.1bps at 191.3bps

EGB Options: Large ECB Cuts Play In Euribor Features Tuesday

Tuesday's Europe rates / bond options flow included:

- ERH4 98.00/99.00cs, bought for 7.5 in 50k

- ERJ3 96.50/96.375/96.25/96.125 put condor bought for 2.5 in 20k

- 2RU3 97.50/98.00cs, sold at 18 in 20k vs ERU3 96.75c, bought for 49 and 50 in 20k

FOREX: USD Index Unchanged As Markets Stabilise

- As concerns over US banking stability abated compared to the panic of the prior two sessions, the USD index is unchanged as we approach Tuesday’s APAC crossover. Stronger equity markets overall and the lower yields at the front-end of the US curve have weighed on the JPY, whereas risk-tied AUD, NZD and CAD have all outperformed.

- Over the US CPI data, USDJPY (+0.64%) aggressively whipsawed and price action eventually prompted a 134.90 print, an impressive recovery from the 132.29 low. Prices have since moderated back to the 134.00 mark ahead of the close and overall, last Friday’s move lower and Monday’s bearish extension, highlights potential for a deeper corrective pullback.

- The pair has traded below support at 134.22, the 50-day EMA. Traders will continue to monitor a clear break of this average which strengthens a short-term bearish threat and exposes 131.31, a Fibonacci retracement point.

- EURUSD has consolidated recent gains on Tuesday and is hovering just below the most recent highs around 1.0750 in late US trade. Price action has strengthened a short-term bull theme and targets 1.0779 next, a Fibonacci retracement, ahead of Thursday’s ECB rate decision.

- Bank of Japan minutes kick off Wednesday’s docket, followed by Chinese activity data. Later on Wednesday, US PPI, retail sales and empire state manufacturing index data will be in primary focus.

FX: Expiries for Mar15 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500(E1.7bln), $1.0696-00(E1.8bln), $1.0730-50(E3.5bln), $1.0800-10(E932mln), $1.0830-50(E1.8bln)

- USD/JPY: Y126.00($2.5bln), Y130.00($1.0bln), Y133.00($1.6bln), Y134.00($541mln), Y135.00($668mln)

- GBP/USD: $1.1895-00(Gbp1.0bln)

- AUD/USD: $0.6675(A$502mln), $0.6720(A$926mln)

- USD/CAD: C$1.3500($744mln), C$1.3575-00($1.5bln), C$1.3725($837mln), C$1.3930-45($1.1bln)

- USD/CNY: Cny6.8600($1.2bln), Cny6.9500($1.9bln)

LATE EQUITIES ROUNDUP: Bank Shares Rebound

- US equities are modestly firmer in recent trade, the e-mini S&P futures paring back advances tied to rebound in bank shares in the first half. First Republic Bank (FRC) currently trading at 38.07 (+22%) vs. 50.97 on the open.

- Front month SPX emini futures accelerated a move off midday highs following an apparent increase in geopolitical tensions after a Russia military jet striking a US unmanned drone.

- Leading gainers, communication sector shares currently outpacing financials.

- From a technical standpoint, the bounce in S&P E-Minis is considered corrective. Price last week cleared key short-term support at 3960.75, Mar 2 low to confirm a resumption of the bear cycle that has been in place since Feb 2. The move lower signals scope for an extension towards 3822.00 next, the Dec 22 low. Initial firm resistance is seen at 4039.14, the 50-day EMA.

E-MINI S&P (M3): Trend Needle Continues To Point South

- RES 4: 4244.00 High Feb 2 and key resistance

- RES 3: 4200.00 Round number resistance

- RES 2: 4119.50 High Mar 6

- RES 1: 3971.50/4039.14 High Mar 13 / 50-day EMA

- PRICE: 3930.00 @ 1450ET Mar 14

- SUP 1: 3839.25 Low Mar 13

- SUP 2: 3822.00 Low Dec 22 and a key support

- SUP 3: 3778.00 Low Nov 3

- SUP 4: 3724.86 76.4% retracement of the Oct 13 - Feb 2 bull cycle

The short-term condition in S&P E-Minis remains bearish and Monday’s move lower reinforces this theme. Today’s bounce is considered corrective. Price last week cleared key short-term support at 3960.75, Mar 2 low to confirm a resumption of the bear cycle that has been in place since Feb 2. The move lower signals scope for an extension towards 3822.00 next, the Dec 22 low. Initial firm resistance is seen at 4039.14, the 50-day EMA.

COMMODITIES: Crude Oil Closes In On Bear Trigger On Market Turmoil

- Crude oil sees heavy declines building into the close, with front WTI crude futures briefly slipping over 5% on the day and narrowing the gap with December lows. Wider financial market concerns are weighing, with further details here.

- WTI is -5.1% at $70.99, through $72.30 (Mar 13 low) and close to the bear trigger at $70.86 (Dec 9 low). Sizeable options volumes again today with most active strikes for the CLJ3 at $70/bbl puts.

- Brent is -4.5% at $77.1, through support at $78.34 (Mar 13 low) and $77.76 (Jan 5 low), opening the bear trigger at $76.04 (Dec 12 low).

- Gold is -0.2% at $1909.47 after a mixed session that broadly consolidates a $90 surge since SVB’s situation first came to light on Thursday. It doesn’t test yesterday’s high of $1914.66 after which lies resistance at $1923.2 (76.4% retrace of Feb 2 – 28 sell-off), whilst support at $1871.6 (Mar 13 low) remains intact.

Wednesday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/03/2023 | 0200/1000 | *** |  | CN | Fixed-Asset Investment |

| 15/03/2023 | 0200/1000 | *** | | CN | Retail Sales |

| 15/03/2023 | 0200/1000 | *** | | CN | Industrial Output |

| 15/03/2023 | 0200/1000 | ** | | CN | Surveyed Unemployment Rate |

| 15/03/2023 | 0700/0800 | *** |  | SE | Inflation report |

| 15/03/2023 | 0745/0845 | *** |  | FR | HICP (f) |

| 15/03/2023 | 1000/1000 | ** |  | UK | Gilt Outright Auction Result |

| 15/03/2023 | 1000/1100 | ** |  | EU | Industrial Production |

| 15/03/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 15/03/2023 | - | | UK | Chancellor Delivers Spring Budget, OBR Forecasts, Likely DMO Remit | |

| 15/03/2023 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 15/03/2023 | 1230/0830 | *** | | US | Retail Sales |

| 15/03/2023 | 1230/0830 | *** | | US | PPI |

| 15/03/2023 | 1230/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/03/2023 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 15/03/2023 | 1400/1000 | * | | US | Business Inventories |

| 15/03/2023 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 15/03/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 15/03/2023 | 2000/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.