Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- Treasuries marched off early session lows Wednesday, following EGBs lead despite pickup in inflation metrics.

- Limited economic data, US mortgage applications rose despite higher rates.

- Fed Beige Book: overall economic activity expanded slightly on net.

US TSYS Near Late Session Highs Ahead Thu's Weekly Claims, Existing Home Sales

- Treasuries marched off early session lows Wednesday, following EGBs lead despite pickup in inflation metrics. Jun'24 10Y marked 108-08 session high well after futures rallied following the second consecutive stop for the 20Y auction reopen: 4.818% high yield vs. 4.840%.

- Limited economic data, US mortgage applications rose despite higher rates: seasonally adjusted 3.3% last week after a flag week prior.

- Fed Beige Book: overall economic activity expanded slightly on balance since late February. Ten out of twelve Districts experienced either slight or modest economic growth—up from eight in the previous report, while the other two reported no changes in activity.

- Short end rates lagged the rally while Projected rate cut pricing steady vs. late Tuesday levels: May 2024 steady at -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 steady at -16.2% w/ cumulative rate cut -4.7bp at 5.282%. July'24 cumulative at -12.6bp, Sep'24 cumulative -24.9bp.

- Thursday Data Calendar: Weekly Claims, Exist Home Sales, Fed Speak from Fed Gov Bowman, NY Fed Williams, Atlanta Fed Bostic and Boston Fed Collins.

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00007 to 5.31882 (-0.00047/wk)

- 3M -0.00037 to 5.32656 (-0.00100/wk)

- 6M -0.00328 to 5.30154 (-0.00183/wk)

- 12M -0.00992 to 5.21009 (+0.01097/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (-0.01), volume: $1.809T

- Broad General Collateral Rate (BGCR): 5.31% (+0.00), volume: $705B

- Tri-Party General Collateral Rate (TGCR): 5.31% (+0.00), volume: $696B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $83B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $244B

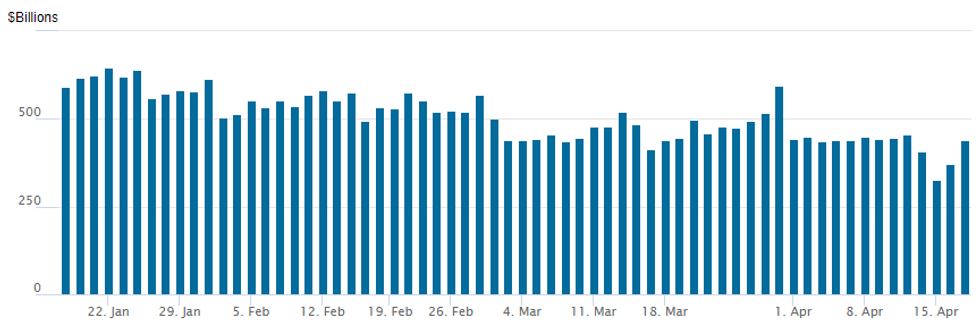

FED Reverse Repo Operation: Back Over $400B

NY Federal Reserve/MNI

- RRP usage climbs back over $400B to $440.508B vs. $371.554B yesterday. Compares to $327.066B on Monday -- the lowest level since mid-May 2021 as desks cited Federal tax deadline for the drop.

- Meanwhile, the latest number of counterparties surges to 89 vs. 68 prior.

SOFR/TEASURY OPTION SUMMARY

SOFR and Treasury option trade leaned toward better upside calls Wednesday as underlying futures followed EGBs higher despite a pick-up in UK inflation metrics. Projected rate cut pricing steady vs. late Tuesday levels: May 2024 steady at -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 steady at -16.2% w/ cumulative rate cut -4.7bp at 5.282%. July'24 cumulative at -12.6bp, Sep'24 cumulative -24.9bp.- SOFR Options:

- +10,000 SFRN4 94.87 straddles, 28.5

- 8,000 SFRZ4 97.00/98.00 call spds ref 95.075

- +15,000 SFRK4 96.50 calls, 0.5 ref 94.73

- +20,000 SFRZ4 96.00/97.00 call spds, 6.5 ref 95.07

- -7,000 SFRM4 94.50/94.62/94.75 put flys, 5.75 vs. 94.735

- -3,000 0QM4 95.50/95.87 call spd w/ 0QM4 95.50/95.93 call spd strip, 22.5

- 2,500 SFRZ4 94.37/94.50/94.75/94.87 put condor vs SRH4 94.25/94.62/95.00 put flys 2.5

- Block, 11,750 SFRV4/SFRZ4 94.62 put spds, 3.0

- Block, 8,880 SFRV4/SFRZ4 94.62 put spds, 2.5

- 2,000 SFRM4 94.87/94.93/95.00/95.06 call condors ref 94.725

- 2,000 SFRU4 95.18/95.37 put spds ref 94.885

- 2,000 SFRZ4 95.87/96.12 call spds, ref 95.05

- 4,000 SFRZ4 95.50/95.75/96.25/96.50 call condors ref 95.06

- 3,000 SFRZ4 94.62/94.87/95.25/95.37 put condors, ref 95.04 to -.045

- Treasury Options:

- 5,300 TYK4 107.5 puts, 18 ref 107-28, total volume over 13.2k

- 6,000 TYM4 108 calls, 58 ref 107-29

- Block, 8,500 TYM4 107.5 puts, 48 ref 107-30

- 5,000 FVK4 105.75/106 call spds ref 105-03.5

- 6,000 USK4 115 puts vs. USM4 113 puts, 5 net/May over

- 5,000 TYK4 106.5/107.5 put spds ref 107-28.5

- 6,000 wk3 TY 107.75 calls, 13 ref 107-23 (expire Friday)

- over 8,000 TYK4 106.25 puts 3-4

EGBs-GILTS CASH CLOSE: Gilts Rally Despite Robust Inflation Data

Gilts outperformed Bunds Wednesday despite stronger-than-expected UK CPI data

- An initial post-UKI CPI sell off in Gilts proved limited and yields began heading decisively lower in the early afternoon.

- Overall the gains in core FI were more of a bounce from extreme weakness earlier in the week, with a risk-off tone and softer energy prices also contributing.

- BoE's Greene sounded slightly more dovish on the inflation situation than expected.

- The German and UK curves bull flattened, with Gilt yields closing on the lows as equities faded in late afternoon and BoE Gov Bailey commented that inflation was due for a "strong drop".

- Periphery spreads closed tighter on the day, led by BTPs.

- Multiple speakers feature Thursday, including ECB's Nagel.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.8bps at 2.944%, 5-Yr is down 1bps at 2.475%, 10-Yr is down 2.1bps at 2.465%, and 30-Yr is down 2.8bps at 2.599%.

- UK: The 2-Yr yield is down 1.3bps at 4.463%, 5-Yr is down 1.7bps at 4.185%, 10-Yr is down 3.8bps at 4.261%, and 30-Yr is down 5.5bps at 4.694%.

- Italian BTP spread down 1.4bps at 144.5bps / Spanish bond spread down 0.6bps at 83.8bps

EGB Options: Leaning Toward Upside Wednesday

Wednesday's Europe rates/bond options flow included:

- RXK4 134/135cs sold at 3 in 7.5k vs RXM4 135/136cs, bought for 8 in 5.6k

- RXM4 132/134cs 1x4, bought the 4 for 64 in 1.5k

- OEK4 118/118.5/119c ladder, bought for 2.5 in 3.4k

- ERU4 96.75/96.87/97.00c fly sold at 1.25 in 6k

- SFIK4 94.90/94.85/94.80p fly, sold at 1 in 1.5k

- SFIK4 94.95/94.80/94.65p fly, sold at 6.5 in 3k

- SFIU4 95.15/95.30 cs vs 94.75p, bought the cs for flat in 4k

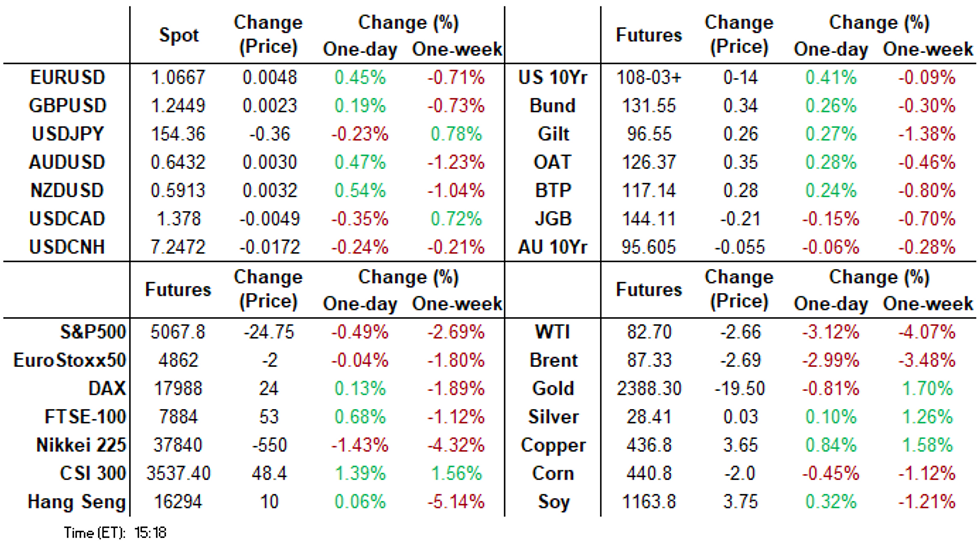

FOREX G10 Ranges Relatively Subdued Despite Lower Core Yields, EM FX Recovers

- Lower core rates on Wednesday have had little impact on G10 currencies throughout the session, with any dollar weakness perhaps offset by the renewed negative sentiment across equity markets. The USD index sits moderately in the red, however, has broadly been consolidating at its most recent lofty levels.

- USDJPY sprung to life late in the session with a small downtick to print fresh session lows at 154.17. The move likely driven by a breach of the overnight lows following an extremely tight trading range on Wednesday. Relatively low volumes support this theory, and the move is much less aggressive than yesterday's sharp selloff during US hours, exacerbated by markets speculating over potential MOF action.

- Overall, the USDJPY uptrend is overbought, however, this is not - for now - a concern for bulls. Sights are on the 155.00 handle next. Support lies much lower at 152.00 and 151.84, 20-day EMA.

- Despite the equity weakness, AUD and NZD are outperforming although these are similarly partial reversals from the steep selloffs this week. In similar vein, emerging market currencies such as PLN, MXN and CLP have traded on the front foot as short-term price action stabilised.

- GBP was only moderately in the green despite the above-expectation CPI data. A bearish theme in GBPUSD remains intact and scope is seen for an extension towards 1.2364, a Fibonacci retracement.

- Fed’s Mester is due to speak late on Wednesday before Australia unemployment data headlines the Thursday APAC calendar. US jobless claims, Philly Fed manufacturing and existing home sales are all scheduled.

FX Expiries for Apr18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0625(E560mln), $1.0635-50(E1.6bln), $1.0700(E700mln), $1.0735-40(E691mln), $1.0750-70(E1.5bln), $1.0800-05(E1.3bln)

- USD/JPY: Y151.85-00($3.2bln), Y153.00($4.9bln), Y153.25($1.0bln), Y153.80($980mln), Y154.00($755mln), Y154.50($898mln), Y155.00($1.0bln)

- GBP/USD: $1.2390-00(Gbp1.1bln), $1.2450(Gbp586mln)

- EUR/GBP: Gbp0.8525-35(E585mln), Gbp0.8590(E782mln)

- EUR/JPY: Y163.99-00(E540mln)

- AUD/USD: $0.6370(A$596mln), $0.6435(A$1.4bln)

- NZD/USD: $0.5900-08(N$1.1bln), $0.5995(N$780mln)

- USD/CAD: C$1.3750($703mln)

Late Equities Roundup: Bouncing Off Lows, Utilities, Banks Leading

- Stocks are trading modestly mixed late Wednesday, off second half lows with the Dow outperforming. Stocks had reversed morning gains earlier as risk assets remain sensitive to Middle East tensions. Currently, DJIA is up 145.39 points (0.38%) at 37946.06, S&P E-Minis up 1.75 points (0.03%) at 5094.5, Nasdaq down 53.2 points (-0.3%) at 15812.38.

- Leading gainers: Utilities and Financials sector shares outperformed in the second half. Gas and multi-energy providers buoyed the former: Southern Co +2.91%, NextEra Energy +2.77%, Consolidated Edison +2.72%. Banks supported Financials late: Citizends Financial +2.78%, Citigroup +2.77%, Bank of America +2.75%.

- Laggers: Information Technology and Industrials continued to underperform in late trade, chip stocks weighing on the former as they reversed prior session gains: Advanced Micro Devices -4.75%, Applied Materials -464%%, Lam Research -4.54%. Transportation stocks weighed on the Industrial sector: JB Hunt -8.66% after missing earnings expectations yesterday including some downgrades, Old Dominion -4.70%.

E-MINI S&P TECHS: (M4) Bear Cycle Still In Play

- RES 4: 5400.00 Round number resistance

- RES 3: 5285.00/5333.50 High Apr 10 / 1 and the bull trigger

- RES 2: 5209.21 20-day EMA

- RES 1: 5154.43 50-day EMA

- PRICE: 5109.25 @ 14:59 BST Apr 17

- SUP 1: 5070.36 38.2% retracement of the Oct 27 ‘23 - Apr 1 bull leg

- SUP 2: 5018.00 Low Feb 21

- SUP 3: 4994.25 Low Feb 13

- SUP 4: 4907.57 50.0% retracement of the Oct 27 ‘23 - Apr 1 bull leg

The short-term trend condition in S&P E-Minis is unchanged and remains bearish. This week’s move lower reinforces the current condition - the contract has traded through support at the 50-day EMA, signalling scope for a continuation lower near-term. Sights are on 5070.36 next, a Fibonacci retracement. Clearance of this level would open 5018.00, the Feb 21 low. Firm resistance is seen at 5209.2, the 20-day EMA.

COMMODITIES WTI Crude Dips Below Support Level

- WTI has dipped below its first support level to be at its lowest since April 1. Oil is shedding some of the geopolitical risk premium as focus shifts to demand concerns from delayed US rate cuts.

- WTI May 24 is down 3.0% at $82.8/bbl.

- Having broken initial support at $83.9, the 20-day EMA, focus turns to $81.06 next, the 50-day EMA. On the upside, the next objective is $89.08, a Fibonacci projection.

- Spot gold edged down by 0.2% to $2,378/oz on Wednesday, leaving the yellow metal 2.2% off its recent record high.

- Sights remain on $2452.5 next, a Fibonacci projection. Initial firm support is at $2286.3, the 20-day EMA.

- Meanwhile, copper rose by 0.9% to $437/lb today, just 1% below its recent 22-month high.

- Earlier Goldman Sachs reported that they see a “very significant” refined copper deficit for this year, which could take copper prices to $12,000 a ton by Q1 2025.

- Iron ore prices jumped another 3.6% on optimism that more Chinese steel mills would restart as demand picks up. Analysts say that there’s been a notable rebound in steel demand for construction, particularly in China’s mid-west.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/04/2024 | 2315/1915 |  | US | Fed Governor Michelle Bowman | |

| 18/04/2024 | 0130/1130 | *** |  | AU | Labor Force Survey |

| 18/04/2024 | 0715/0915 |  | EU | ECB's De Guindos ECB Report Presentation | |

| 18/04/2024 | 0800/1000 | ** | | EU | Current Account |

| 18/04/2024 | 0900/1100 | ** | | EU | Construction Production |

| 18/04/2024 | 1230/0830 | *** | | US | Jobless Claims |

| 18/04/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 18/04/2024 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 18/04/2024 | 1305/0905 | | US | Fed Governor Michelle Bowman | |

| 18/04/2024 | 1315/0915 | | US | New York Fed's John Williams | |

| 18/04/2024 | 1315/0915 | | US | Fed's Miki Bowman | |

| 18/04/2024 | 1400/1000 | *** | | US | NAR existing home sales |

| 18/04/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 18/04/2024 | 1500/1100 | | US | Atlanta Fed's Raphael Bostic | |

| 18/04/2024 | 1500/1600 |  | UK | BOE's Greene with Atlantic Council GeoEconomics Center | |

| 18/04/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 18/04/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 18/04/2024 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 18/04/2024 | 1730/1930 | | EU | ECB's Schnabel Speaks At 2024 EU-US Symposium | |

| 18/04/2024 | 2145/1745 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok