Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- ECB'S SCICLUNA: EUROPE'S ECONOMY IS FACING A SOFT LANDING, Bbg

- ECB'S SCICLUNA: RISKS ARE EVERYWHERE BUT INFLATION IS EASING, Bbg

- MNI SECURITY: Blinken: Israel-Hamas Hostage Deal Is Still Possible

- MNI UKRAINE: Zelenskyy To Sign Security Deal w/France Ahead Of MSC Appearance

- MNI MIDEAST: US Intercepts Iran Weapons Set For Houthis As Frequency Of Attacks Fall

Key Links:MNI US DATA: Poorest Retail Sales Report In 10 Months, Weather A Potential Factor / MNI SOURCES: ECB Cut Expectations Range From 50-100BP In 2024 / MNI SOURCES: New ECB Framework To Maintain Continuity / MNI BRIEF: Lawmakers Debate Fed's Lender of Last Resort Role / MNI FED: Fed's Waller Sees Dollar Staying Dominant World Currency /

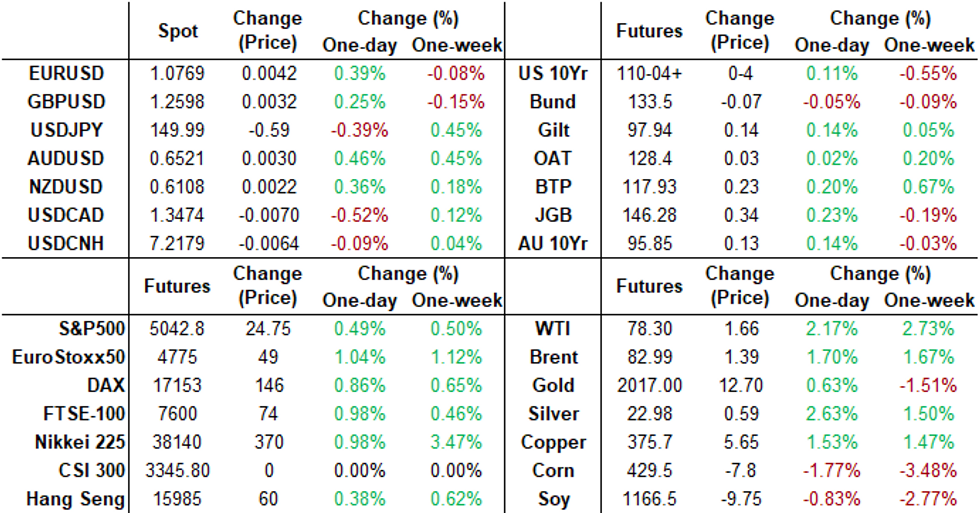

US TSYS Hold Modest Bid After Weakest Retail Sales Since March 2023

- Still bid, Treasury futures are drifting near the lower end of a narrow session range Thursday (TYH4 +4.5 at 110-05 vs. 110-00.5 low, yield -.0117 at 4.2437). No significant technical breakout despite an initial gap bid after this morning's deluge of economic data.

- Cash Tsys mirrored similar bull flattening moves in EGBs while off highs following wait and see tones from ECB Lagarde wanting to avoid any "hasty" decisions to cut rates with more evidence of inflation decline needed.

- Treasury futures gap higher, retrace half the move after lower than expected Retail Sales MoM (-0.8% vs. -0.2% st, 0.6% prior). The core categories also started the year on a negative note, inc contrast to relative strength at the end of 2023: ex-autos -0.6% (+0.2% survey, +0.4% prior), ex-auto/gas -0.5% (+0.2% survey, +0.6% prior), and for the key Control Group which is a GDP input, -0.4% (+0.2%, +0.8% prior). Overall the contractions pointed to the weakest report since March 2023.

- Initial Jobless Claims less than expected, however: 212k vs. 220 est, while Continuing Claims rise 1.895M vs. 1.880M est.

- TYH4 breached Initial technical resistance at 110-16 (low Feb 9) briefly before settling in around 110-06 +/- 1-2 tics. little react to the rest of the data: Industrial Production/Capacity Utilization, Business Inventories and NAHB Housing Market Index. Total Net TIC Flows wraps things up at 1600ET.

- Look ahead: Friday data calendar includes PPI, House Starts/Build Permits, UoM Inflation

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00156 to 5.31979 (-0.00093/wk)

- 3M -0.00659 to 5.31909 (+0.01004/wk)

- 6M -0.01340 to 5.24355 (+0.05489/wk)

- 12M -0.01429 to 5.00468 (+0.12443/wk)

- Secured Overnight Financing Rate (SOFR): 5.30% (-0.01), volume: $1.596T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $671B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $656B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $107B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $270B

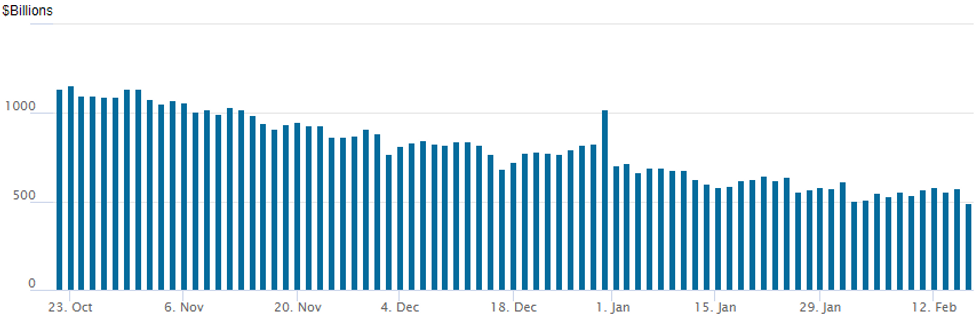

FED Reverse Repo Operation: Falls Below $500B

NY Federal Reserve/MNI

- RRP usage falls below $500B for the first time since early June 2021 today: $493.065B vs. $575.332B Wednesday.

- Meanwhile, the latest number of counterparties is at 82 from 91 Wednesday (compares to 65 on January 16, the lowest since July 7, 2021).

SOFR/TREASURY OPTION SUMMARY

Second day of heavy SOFR and Treasury option volumes, mostly targeting downside puts and put structures as accts hold to the post-CPI mindset of significantly delayed rate cuts as the Fed waits for sign inflation is at bay.- Notable SOFR call condor spread (highlighted), similarly structured: Given where underlying futures are, it appeared the spread initiator looked for rate cut pricing in the fall of 2024 to wane vs. positioning for rate cut pricing in the fall of 2025 to increase.

- Projected rate cut pricing looks steady by mid-year (Jun fully priced): March 2024 chance of 25bp rate cut currently -14.4% w/ cumulative of -3.6bp at 5.293%; May 2024 at -31.2% w/ cumulative -11.4bp at 5.215%; June 2024 -68.5% w/ cumulative cut -28.5bp at 5.043%. Fed terminal at 5.3275% in Feb'24

- Block -20,000 SFRU4 95.00/95.50/95.75/96.25 call condors ref 95.345 vs. +20,000 SFRM4 96.25/97.00/98.50/99.25 call condors ref 96.18, Jun25 bought over 5.0-5.5 on splits

- Block, 20,000 SFRH4 94.93/95.37 call spds, 0.5 ref 94.73

- Block, +20,000 SRJ4 94.37/94.75/94.87put flys 2x3x1 +.75

- Block, -10,000 SFRM5 96.25/97.00/98.50/98.75 broken call condors, 23.75 ref 96.21

- Block 10,000 SFRM5 96.25/97.25 call spds, 31.25 splits ref 96.20

- +8,000 SRH4 94.68/94.81/94.87/94.93 put condor 3 ref 94.74

- -10,000 SRM4 95.25/95.50/95.75 call flys, 1.25 ref 95.04

- +10,000 SRU4 94.75/94.87 p spds vs. 95.415/0.10% with SRZ4 94.75/94.87 put spds, 5.0 total

- -10,000 SFRJ4 95.00/95.25 call spds, 7.75 ref 95.04

- +4,000 SRJ4 95.31/95.50 call spds v SRK4 95.00/95.06 call spd .75

- -5,000 SRH4 94.62/94.75/94.87/95.00 call condor 7.5 ref 94.74

- -5,000 SRJ4 95.25/95.50/96.00 call flys 1.0 ref 9502

- +4,000 SRJ4 95.00 puts 12.0 vs. 95.00/0.48%

- +5,000 SRM4 94.87 calls v 0QM4 96.50 calls 2.0

- +5,000 SFRM4 94.25/94.50 put spds 0.75

- Block, total -26,886 SFRK4 94.75 puts, 3.25 on splits

- over 6,900 SFRM4 96.37 calls, ref 95.01

- 8,000 SFRJ4 95.12/95.25/95.37/95.50 call condors ref 95.10

- 5,000 SFRM4 94.56/94.68/94.81 put flys 2.0 ref 95.005

- 7,500 SFRJ4 95.00/95.25 call spds ref 95.01

- 2,000 SFRG4 94.62/94.75/94.81 1x3x2 put flys

- 3,000 0QH4 96.12/96.25 put spds ref 95.955

- +22,500 TYJ4 109.5 puts, 28 (adds to +50k earlier at 30)

- +15,000 TYJ4 108.5/110 put over risk reversals 22 ref 110-10.5 (+50,000 TYJ4 108/112 put over risk reversals 3 ref 110-00 yesterday)

- +50,000 FVJ4 106.5 puts 22 ref 107-10.75

- 8,000 USH4 116/117 put spds 4 ref 119-13

- +50,000 TYJ4 109.5 puts, 30 ref 110-24.5 (total volume over 65k)

- 5,000 TYJ4 107/108 put spds ref 110-24.5

- 15,000 TYH4 109/110 put spds 3 over TYJ4 108.5/109.5 put spds

- 2,500 TUH4 101.87/102.25 put spds ref 102-03

- 5,000 wk3 TY 110.5/111 2x3 call spds (expire tomorrow)

- 2,000 TYH4 111/112 put spds ref 110-06.5

- *On Wednesday:

- +50,000 TYJ4 108/112 put over risk reversals 3 ref 110-00 (open interest +40k in each strike this morning).

- +40,000 TYH4 109.50 put 24 vs. 109-22.5 (open interest +11,900 on total volume of 117,500) - partially funded by sales in 109.25 and 109 puts

EGBs-GILTS CASH CLOSE: Marginally Weaker As Data Is Second-Guessed

Bunds and Gilts faded after a constructive start Thursday, with negative data surprises being second-guessed.

- Core FI got off on the front foot as Q4 UK GDP came in weak and confirmed a technical recession in 2H 2023, but the move fades as the report wasn't seen to be shifting the needle significantly for BoE policy.

- Likewise, Bunds and Gilts got a boost in early afternoon trade amid mixed-to-soft US data highlighted by poor January retail sales but eventually reversed lower as the miss was seen to be at least partially influenced by poor weather, and US jobless claims/regional manufacturing surveys were more favourable.

- While there was plenty of central banker commentary, from ECB's Lagarde and BoE's Greene (sounding as though she won't soon vote for a cut) among others, there was little evident immediate reaction in rates markets.

- Even so, rate cut expectations drifted lower overall on the day, with 77bp in BoE cuts now seen in 2024 (vs 79bp Weds); ECB cut pricing was likewise pared by 2bp, last 112bp.

- Bunds underperformed Gilts, with the German curve leaning bear flatter; the UK curve marginally bear steepened. Periphery spreads were a little tighter

- UK retail sales will be the highlight early Friday, concluding a busy week for UK data; we also hear from ECB's Schnabel (and BoE's Pill after the close).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 2.5bps at 2.755%, 5-Yr is up 3bps at 2.332%, 10-Yr is up 2.2bps at 2.359%, and 30-Yr is up 2.2bps at 2.531%.

- UK: The 2-Yr yield is up 0.5bps at 4.58%, 5-Yr is up 0.6bps at 4.063%, 10-Yr is up 1bps at 4.054%, and 30-Yr is up 2.5bps at 4.604%.

- Italian BTP spread down 2bps at 149.6bps / Spanish down 1.4bps at 91.6bps

EGB Options: Mixed UK Rates Trade Features Thursday

Thursday's Europe rates/bond options flow included:

- SFIG4 94.75p, bought for 0.25 in 4.5k

- SFIM4 95.10/95.20/95.30/95.40c condor, bought for 1.5 in 17k total

- ERJ4/ERK4 96.37/96.25/96.12p fly strip, bought for 4 in 5k

FOREX USD Index Extends Retracement Lower Amid Equities Recovery

- Following Tuesday’s strong advance for the greenback on the back of hotter-than-expected inflation data, the past two sessions have seen the dollar steadily reverse lower. The USD index is down a further 0.40% on Thursday and has been assisted lower by the impressive recovery for major equity indices and e-mini S&Ps within close proximity of the all-time highs for the index.

- Associated gains for G10 currencies were broad based, with the likes of AUD, NZD and CAD all moderately outperforming and the Swiss Franc the major beneficiary to the more optimistic risk sentiment across global markets.

- USDCHF has declined 0.7% on the session but in the broader context remains around 5.5% above the December low, with the softer-than-expected local CPI data stoking the most recent CHF weakness this week.

- Overall, intra-day volatility was spurred on by a weaker set of January retail sales data in the US, however, firmer Philly Fed and Empire Manufacturing data quickly offset the greenback dip. USDJPY reached as low as 149.57 on the data from the earlier 150.58 highs, but has since settled around mid-range and close to the psychological 150.00 mark.

- EURUSD rose in line with the moves for the greenback, breaching its initial resistance point of 1.0750 (50% retracement for this week's downleg) and has continued to narrow the gap to the 50-dma which resides at 1.0796.

- UK retail sales data headlines the European docket on Friday before focus turns to US PPI figures and building permits. Preliminary UMich consumer sentiment and inflation expectations will round off the week.

FX Expiries for Feb16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0615(E1.65bln), $1.0670-75(E1.9bln), $1.0700(E2.5bln), $1.0715-25(E1.9bln), $1.0750-55(E2.5bln), $1.0800(E3.6bln), $1.0820-25(E1.4bln), $1.0850(E1.2bln), $1.0870-80(E2.0bln), $1.0900-05(E2.6bln), $1.0925(E1.1bln)

- GBP/USD: $1.2280-90(Gbp1.1bln), $1.2650-60(Gbp1.9bln), $1.2685-90(Gbp716mln)

- USD/JPY: Y148.90-00($1.8bln), Y150.00($1.7bln), Y150.15-25($947mln), Y150.40-50($1.1bln), Y151.95-00($1.0bln)

- EUR/GBP: Gbp0.8575-80(E842mln)

- AUD/USD: $0.6350(A$1.6bln), $0.6475(A$625mln), $0.6495-00(A$715mln), $0.6535-41(A$1.2bln), $0.6600-10(A$1.1bln)

- AUD/NZD: N$1.0610(A$591mln)

- USD/CAD: C$1.3485-95($1.1bln), C$1.3500-05($1.9bln)

- USD/CNY: Cny7.2000($1.2bln)

Late Equities Roundup: Oil & Gas Shares Buoy the Energy Sector

- Stocks clinging to modestly higher levels, SPX Eminis above pre-CPI levels, but still shy of contract high of 5066.50 at the moment. Currently, the DJIA is up 161.23 points (0.42%) at 38585.7, S&P E-Minis up 4.25 points (0.08%) at 5022.25, Nasdaq down 41.5 points (-0.3%) at 15817.05.

- Leading gainers: Energy and Real Estate sector shares continued to outperform in late trade, oil and gas shares supported the Energy sector after paring early week gains yesterday: APA +5.1%, Diamondback Energy (FANG) +5.06%, Targa Resources +4.82%. Estate management company CBRE Group buoyed the Real Estate sector as it gained 8.55% after beating earnings this morning, Costar Group only gained 1% in comparison.

- Laggers: Information Technology and Communication Services sectors underperformed, hardware and equipment makers weighed on IT: Cisco -1.95, NetApp -1.37%, Apple -1.17%. Paring midweek gains, Media and entertainment shares weighed on the Communication Sector: Paramount -5.12%, Google -2.75%, Comcast -0.40%.

- Looking ahead: corporate earnings expected after the close: DoorDash Inc, Ingersoll Rand, Roku, Applied Materials

E-MINI S&P TECHS: (H4) Bullish Outlook

- RES 4: 5170.86 2.236 proj of Nov 10 - Dec 1 - 7 price swing

- RES 3: 5110.50 2.00 proj of Nov 10 - Dec 1 - 7 price swing

- RES 2: 5100.00 Round number resistance

- RES 1: 5066.50 High Feb 12 and the bull trigger

- PRICE: 5045.00 @ 1450 ET Feb 15

- SUP 1: 4947.87 20-day EMA

- SUP 2: 4866.000/4836.90 Low Jan 31 / 50-day EMA values

- SUP 3: 4702.00 Low Jan 5

- SUP 4: 4594.00 Low Nov 30

The trend condition in S&P E-Minis is unchanged and remains bullish. The pullback from Monday’s 5066.50 high is considered corrective and support to watch lies at 4947.87, the 20-day EMA. A clear break of this average would suggest potential for a deeper retracement, possibly towards the 4866.00 key support, the Jan 31 low. For bulls, the trigger for a resumption of gains is 5066.50, the Feb 12 high.

COMMODITIES Weaker Greenback Supports Both Crude Futures and Precious Metals

- Crude markets are finishing the day stronger, boosted by a weakening in the US dollar with front month WTI up around 1.9% at 78.08$/bbl. Focus remains on headlines from the middle east where most recently wires carried comments from Houthi leader Abdul Malik al-Houthi stating that "We will continue our operations as long as Israel continues its crimes."

- Separately, Global oil demand growth is forecast to rise by 1.2mbpd, unchanged from last month’s report, according to the IEA Monthly Oil Market Report.

- Recent gains in WTI futures, since Feb 5, appears to be a correction - for now. Key short-term resistance has been defined at $79.29, the Jan 29 high. Clearance of this level would be a bullish development.

- For natural gas, Henry Hub has continued its downtrend amid additional pressure from below-expectation storage draw. Front-month remains at a seven-month low, down -1.4% on Thursday at 1.59$/mmbtu.

- The weaker greenback helped precious metals climb, although silver (+2.34%) has outpaced the advance for gold (+0.57%) on Thursday.

- Technical conditions for spot gold may be limiting the advance, following the prior breach this week of $2001.9, the Jan 17 low and a key short-term support. The breach highlights a resumption of the bear leg that started Dec 28. A continuation lower would open $1973.2, the Dec 13 low and the next key support. On the upside, the yellow metal would need to clear resistance at $2065.5, the Feb 1 high, to reinstate a bullish theme.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/02/2024 | 1300/0800 |  | US | Richmond Fed's Tom Barkin | |

| 16/02/2024 | 1330/0830 | * |  | CA | International Canadian Transaction in Securities |

| 16/02/2024 | 1330/0830 | ** | | CA | Wholesale Trade |

| 16/02/2024 | 1330/0830 | *** | | US | PPI |

| 16/02/2024 | 1330/0830 | *** | | US | Housing Starts |

| 16/02/2024 | 1410/0910 | | US | Fed Vice Chair Michael Barr | |

| 16/02/2024 | 1500/1000 | ** | | US | U. Mich. Survey of Consumers |

| 16/02/2024 | 1710/1210 | | US | San Francisco Fed's Mary Daly | |

| 16/02/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 16/02/2024 | 1940/1940 |  | UK | BOE's Pill panellist at 40th NABE Conference |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.