Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

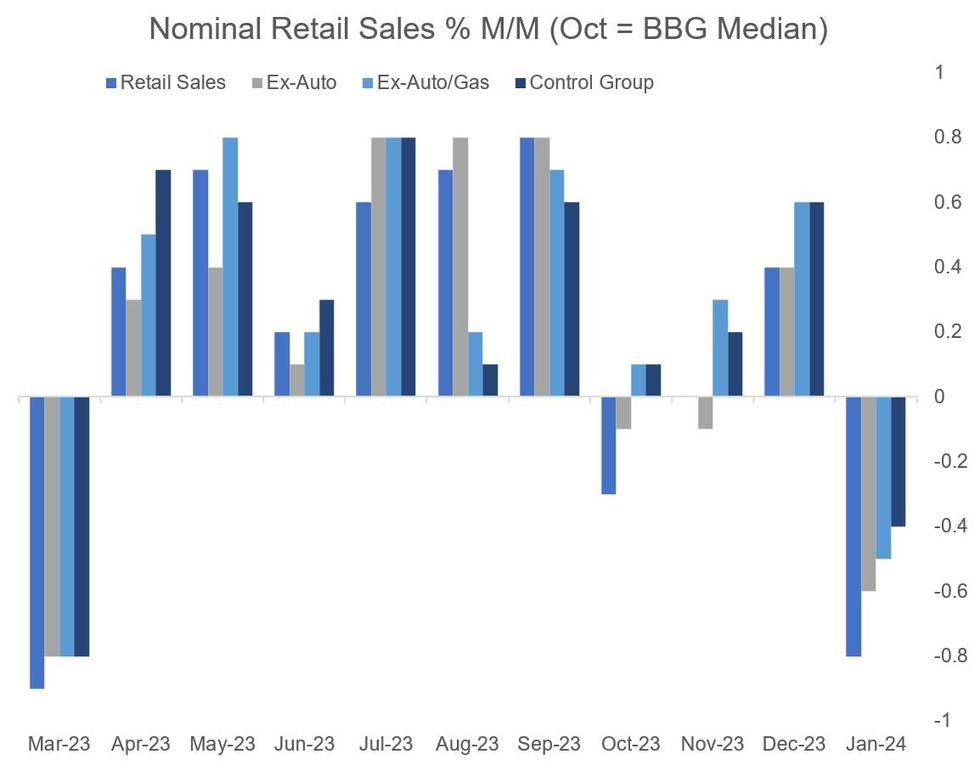

US retail sales came in weaker than expected in January's advance estimates, with the headline figure printing -0.8% M/M (vs -0.2% survey, 0.4% prior revised down from 0.6%).

- The core categories also started the year on a negative note, inc contrast to relative strength at the end of 2023: ex-autos -0.6% (+0.2% survey, +0.4% prior), ex-auto/gas -0.5% (+0.2% survey, +0.6% prior), and for the key Control Group which is a GDP input, -0.4% (+0.2%, +0.8% prior). Overall the contractions pointed to the weakest report since March 2023 (see chart).

- Contributing heavily to the decline was motor vehicles/parts (-1.7% vs +0.3% prior), building material/garden equipment (-4.1% vs +0.9% prior), and gas stations (-1.7% vs -0.8% prior).

- Broader retailer categories fared poorly: general merchandise store growth was flat (vs +1.2% prior), with miscellaneous stores (-3.0% vs -0.3% prior) and nonstore retailers (-0.8% vs +1.4% prior) showing deteriorating activity.

- Elsewhere, there was some improvement in furniture (+1.5% vs -0.2% prior) and food services/drinking places (+0.7% vs 0.2% prior).

- We wouldn't read too closely into these figures: it's possible that unusually poor weather in January may have negatively impacted some categories unduly, even considering the relevant seasonal adjustment. December's very strong data (note downwardly revised) may have been due a retracement and we would wait until February's report to get a better sense of the health of the retail sector. That said, the poor Control Group figure poses immediate downside risks to consumption in quarterly GDP estimates.

- The "real" (CPI-deflated) retail sales index pulled back to the weakest level since April 2023.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok