Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: Fed's SVB Review Focused on Fixing Regulation Flaws

- FED BLAMES SVB FAILURE ON MANAGEMENT, INADEQUATE SUPERVISION, Bbg

- BARR: FED TO WEIGH IMPROVED LIQUIDITY AND CAPITAL REQUIREMENTS, Bbg

- MNI UKRAINE: Def Min-Preparations For Counteroffensive Being Concluded

- MNI RUSSIA: Kremlin Downplays Prospect Of Nuclear Test

US TSYS: US FI Rates, Equities Finish Strong Ahead Next Wed's FOMC

- After a rocky start, Treasury futures are trading broadly higher late Friday, short end lagging with curves running flatter, 2s10s -6.119 at -61.515. Heavy two-way flow noted after March Core PCE climbed 0.3% vs. 0.2% est, the 1Q ECI up 1.2% vs. 1.1%.

- Close to expectations, it’s technically the softest core PCE print since Nov’22 but clearly remains far stronger than the monthly rate consistent with the 2% target.

- Services eased from 0.38% to 0.23% M/M whilst Bloomberg's calculation of non-housing core services fell from 0.35% to 0.24% M/M for its softest since Jul'22.

- Treasuries marked session highs by midmorning (TYM3 115-12 (+20.5), trading sideways after a brief decline on stronger than expected Chicago Business BarometerTM, produced with MNI.

- The barometer improved by 4.8 points to 48.6 in April. This was the highest reading since August 2022. Nonetheless, the headline index remained sub-50, thus signaling an eight consecutive month of contractionary business activity.

- Focus turns to next Wednesday's FOMC policy announcement where a 25bp hike in could mark the end of the Fed’s hiking cycle. With rates above 5%, and sticky inflation fears offset by the tightening effect of banking sector woes, the FOMC is likely to move to a meeting-by-meeting policy beyond May, while retaining a bias toward further policy firming.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.02549 to 5.01870 (+.04818/wk)

- 3M +0.03787 to 5.08132 (+.01357/wk)

- 6M +0.05826 to 5.07957 (-.00877/wk)

- 12M +0.08282 to 4.80908 (-.07339/wk)

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00086 to 4.81100%

- 1M +0.02800 to 5.06214%

- 3M +0.00329 to 5.30243% */**

- 6M +0.02014 to 5.40700%

- 12M +0.04486 to 5.36629%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.30243% on 4/28/23

- Daily Effective Fed Funds Rate: 4.83% volume: $119B

- Daily Overnight Bank Funding Rate: 4.81% volume: $282B

- Secured Overnight Financing Rate (SOFR): 4.81%, $1.337T

- Broad General Collateral Rate (BGCR): 4.78%, $545B

- Tri-Party General Collateral Rate (TGCR): 4.78%, $538B

- (rate, volume levels reflect prior session)

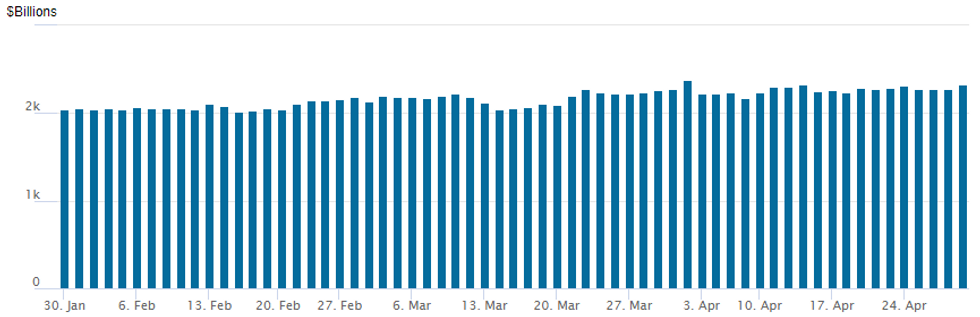

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage rebounds to $2,325.479B w/ 108 counterparties, compares to prior $2,273.926B. Compares to high usage for 2023: $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTIONS SUMMARY

Despite a strong rebound and robust volumes in underlying rate futures Friday, it's difficult to draw broad conclusions on the muted overall option flow. Most option desks appeared to be plying the sidelines ahead the weekend (and month-end allocation) not to mention next week Wednesday's FOMC policy announcement.

- Two trades of note, however, were in SOFR put options. Jun'24 94.68 puts at 5.0 (vs. 94.90/0.29%) were bought in small lots for a total over 45,000 in the first half. Prior to that, was a sale of over -40,000 (Block, screen, pit) SFRM3 94.37/94.50/94.56/94.68 put condors at 2.0 ref 94.90. Heavy open interest in all four strikes from 188k low to 377k high, put the sale likely a closer as the account looks for the Fed's rate hike to evaporate after next Wed's likely 25bp move.

- SOFR Options:

- +7,000 SFRZ3 94.25/95.25 put spds, 28.0

- +45,000 SFRM3 94.68 puts, 5.0 vs. 94.90/0.29%

- Block/pit, -40,000 SFRM3 94.37/94.50/94.56/94.68 put condors, 2.0 ref 94.895 to -.90

- 2,000 SFRZ3 96.00/96.50/97.00/97.50 call condors ref 95.53

- +5,000 SFRU3 95.00/95.50/96.00 call flys, 5.5

- 5,000 SFRK3 94.93/95.00 call spds, ref 94.915

- Block/screen, 8,700 SFRM3 94.68 puts, 4.75 vs. 94.90/0.29%

- Treasury Options:

- 2,750 TYM3 114/114.5 put spds, 11 ref 115-10.5

- 2,000 FVM3 108.75/110.75 strangles, 44.5

- 2,500 USM3 125.5/128 2x1 put spds,

- over 5,000 TYM3 116 calls, 45 last

- 1,400 TYM3 112.75/117.25 strangles, 35 ref 115-08.5

- 2,500 TYM3 110/111 put sprd ref 115-05

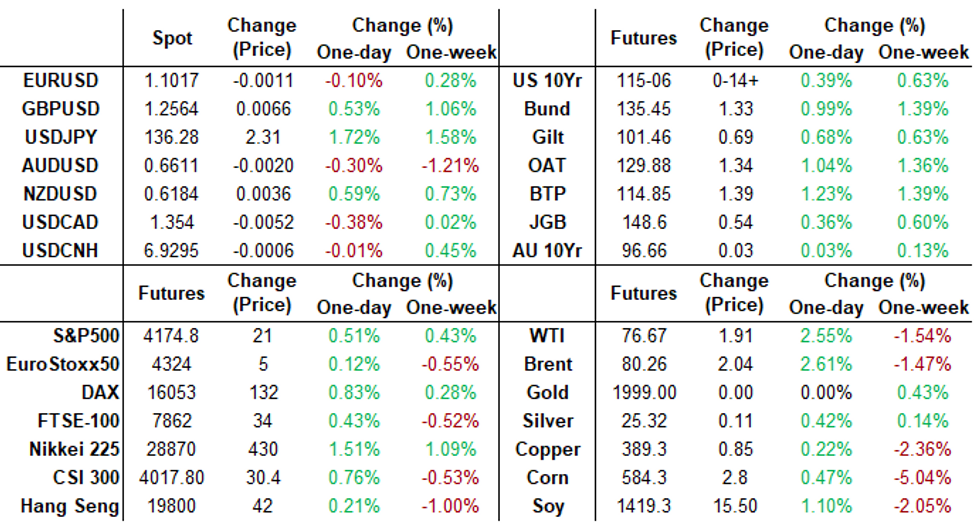

FOREX: EURJPY Rises Above 150.00, Highest Since 2008

- Moves in currency markets on Friday were dominated by the Japanese Yen, comfortably the weakest performer in G10 following the latest BoJ Monetary Policy decision. USDJPY (+1.67%) rose back above 136.00 to print as high as 136.56, a seven-week high for the pair. More notably, EURJPY (+1.52%) breached the 150.00 mark for the first time since 2008 after breaking above the 2014 highs and reaching 150.43.

- The BoJ removed reference to Covid in its forward guidance. It also removed reference to rates in terms of the guidance (expecting rates to remain at low or present levels was left out), but the Bank left in that is prepared to take further easing measures if necessary. The BOJ will also conduct a review, which is expected to take 1-1.5 yrs.

- The USDJPY rally initially pulled the USD index higher and some further greenback strength was seen following the firmer employment cost index data and an in-line set of PCE figures. However, an extension of strength for major equity indices throughout the US session weighed on the greenback which saw the DXY pare those gains.

- Moves/position squaring may have been exacerbated heading into month-end where there was a notable rally for GBPUSD. Cable has breached 1.2546, the Apr 14 high and the technical bull trigger. Clearance of this level would resume the uptrend and open 1.2599, the Jun 7 2022 high. Moving average studies remain in a bull mode position, highlighting the uptrend. Above here we have 1.2667, the May 27 2022 high.

- After a Uk/Europe bank holiday on Monday, US ISM manufacturing data is scheduled. The focus then inevitably turns to Wednesday’s FOMC decision where a 25bp hike could mark the end of the Fed’s hiking cycle. Next week, we also have the RBA & ECB meetings as well as Friday’s release of non-farm payrolls.

FX OPTION EXPIRY

- EURUSD 3.27bn at 1.1000.

- AUDUSD 1.3bn at 0.6600.

- EURUSD; 1.0950 (472mln), 1.0960 (251mln), 1.0970 (206mln), 1.0975 (500mln), 1.1000 (3.27bn), 1.1025 (486mln), 1.1040 (738mln).1.1050 (413mln).

- GBPUSD: 1.2500 (343mln).

- USDJPY: 135.00 (423mln).

- USDCAD: 1.3600 (809mln), 1.3625 (388mln).

- AUDUSD: 0.6550: 880mln), 0.6600 (1.3bn).

Late Equities Roundup: Two Day Rally Off April Lows Into Month End

Stocks look to extend late session highs Friday, adding to Thursday's largest one-day rally since January 6 (+77.75 vs. +86.75). At the moment, DJIA up 221.63 points (0.66%) at 33983.68; S&P E-Mini Future up 28.5 points (0.69%) at 4175; Nasdaq up 61.3 points (0.5%) at 12188.54.

- There appeared to be no particular headline or catalyst for the support other than a reluctance to sell into the bounce off Wednesday's low for the month (SPX 4070.25) going into moth end. That, and generally positive quarterly earnings announced in the latest cycle.

- Friday's move higher exposes key resistance and the bull trigger at 4198.25, the Apr 18 high. Clearance of this level would confirm a resumption of the uptrend that started Mar 13 and open 4244.00, the Feb 2 high.

- On the downside, key short-term support has been defined at 4068.75, the Apr 26 low. A break would be bearish.

- Meanwhile, the Federal Reserve issued it's supervisory report on Silicone Valley Bank Friday, laying blame on the banks board of directors and management but is also critical of its own supervisors that the Fed says did not appreciate the extent of SVB vulnerabilities and did not take sufficient steps to ensure the bank fixed those problems quickly enough.

E-MINI S&P TECHS: (M3) Strong Recovery Extends

- RES 4: 4244.00 High Feb 2 and a medium-term bull trigger

- RES 3: 4223.00 High Feb 14

- RES 2: 4205.50 High Feb 16

- RES 1: 4198.25 High Apr 18 and key resistance

- PRICE: 4178.50 @ 19:25 BST Apr 28

- SUP 1: 4123.96/4068.75 20-day EMA / Low Apr 26

- SUP 2: 4061.11 38.2% retracement of the Mar 13 - Apr 18 bull leg

- SUP 3: 4052.50 Low Mar 30

- SUP 4: 4018.75 50.0% retracement of the Mar 13 - Apr 18 bull leg

S&P E-minis rallied Thursday to erase the sell-off earlier this week and the contract continues to appreciate. The move higher exposes key resistance and the bull trigger at 4198.25, the Apr 18 high. Clearance of this level would confirm a resumption of the uptrend that started Mar 13 and open 4244.00, the Feb 2 high. On the downside, key short-term support has been defined at 4068.75, the Apr 26 low. A break would be bearish.

COMMODITIES: Risk-On Session Can’t Quite Offset Earlier Declines In Crude On Wk

- Crude oil is finishing the session on a strong note but still sits lower over the week after prior demand concerns haven’t been fully allayed despite a recovery in broader risk sentiment.

- Pioneer sees a WTI price at $80-100 later this year whilst in products, JPM sees a structural and permanent shift in diesel usage, including a greater shift to biofuels.

- WTI is +2.7% at $76.78, bucking its prior vulnerable trend to move closer but still some way off a key short-term resistance level at $79.18 (Apr 24 high).

- Brent is +1.5% at $79.55, moving closer but still some way off to resistance at $82.88 (Apr 25 high).

- Gold is +0.1% at $1990.34 as a reversal in prior USD strength has allowed the yellow metal to recover mid-session off a low of $1976.4. It didn’t trouble support at $1969.3 (Apr 19 low), whilst resistance remains at $2015.1 (Apr 17 high).

- Weekly moves: WTI -1.4%, Brent -2.6%, Gold +0.4%, US nat gas +8%, EU TTF nat gas -4.1%

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 01/05/2023 | 2300/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

| 01/05/2023 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 01/05/2023 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (final) |

| 01/05/2023 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 01/05/2023 | 1400/1000 | * | | US | Construction Spending |

| 01/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 01/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.