Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS

- US OCT NONFARM PAYROLLS +261K; PRIVATE +233K, GOVT +28K

- FED BARKIN: UNSURE OF DECEMBER FOMC MOVE, MORE DATA STILL COMING, Bbg

- FED COLLINS: SMALLER INCREMENTS WILL OFTEN BE APPROPRIATE, Bbg

- BANK OF ENGLAND'S PILL: THERE IS STILL MORE TO COME ON RATE RISES, Bbg

- CHINA'S PRESIDENT XI: CHINA WILL CONTINUE TO OPEN UP, TO PURSUE WIN-WIN COOPERATION, Rtrs

Key links:MNI INTERVIEW-Fed Set For ‘Lively Debate’ On Size Of Dec. Hike / MNI: Fed Collins Says Sept SEP ‘Starting Point’ For Rate Peak / MNI PODCAST: FedSpeak-Weinberg Says Need Positive Real Rates / MNI: Canada Red Hot Job Mkt Returns On 108K Jobs Vs 5K Forecast

Oct Jobs Strong, But Off Mid-Yr Pace, Short End Firm on Dovish Fedspeak

Tsy futures mixed after the bell, well off post-data lows: yield curves broadly steeper - near highs (2s10s +7.322 at -50.00 vs. -61.953 low) as earlier dovish Fed speak gained traction again: short end higher (Dec 2022: cumulative hikes slips 57.3 to 4.40% as Terminal Funds rate holds at 5.155% in June'23).

- Earlier comments from Fed speakers: Boston Fed Collins and Richmond Fed Barkin also helped stocks rally on the day. “I believe it is time to shift focus from how rapidly to raise rates, or the pace, to how high – in other words, to determining what is sufficiently restrictive,” Collins said. “Down the road, when we get there, in my view we’ll need to shift again to focus on how long to hold rates at that level.”

- Barkin headlines from CNBC: "UNSURE OF DECEMBER FOMC MOVE, MORE DATA STILL COMING .. CAN CREDIBLY SAY FED HAS `FOOT ON THE BRAKE'".

- Tsys sold-off after Oct NFP climbed +261k higher than estimated +195k, while Sep up-revised to +315k, Aug to +292k. Unemploy rate climbs to 3.7% - sources say "for the wrong reasons as the labor force participation rate and the share of workers with a job declined."

- Look ahead: Fed speakers and Tsy auctions outweigh data in the first half of next week. Focus on Oct CPI Wed morning: MoM 0.6% est vs. 0.4% prior

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00300 to 3.81629% (+0.75243/wk)

- 1M +0.01157 to 3.85814% (+0.09043/wk)

- 3M +0.01872 to 4.55029% (+0.11072/wk) * / **

- 6M +0.01400 to 5.01129% (+0.08043/wk)

- 12M +0.01286 to 5.66643% (+0.29743/wk)

- * Record Low 0.11413% on 9/12/21; ** New 14Y high: 4.55029% on 11/4/22

- Daily Effective Fed Funds Rate: 3.83% volume: $97B

- Daily Overnight Bank Funding Rate: 3.82% volume: $284B

- Secured Overnight Financing Rate (SOFR): 3.80%, $1.074T

- Broad General Collateral Rate (BGCR): 3.76%, $418B

- Tri-Party General Collateral Rate (TGCR): 3.75%, $393B

- (rate, volume levels reflect prior session)

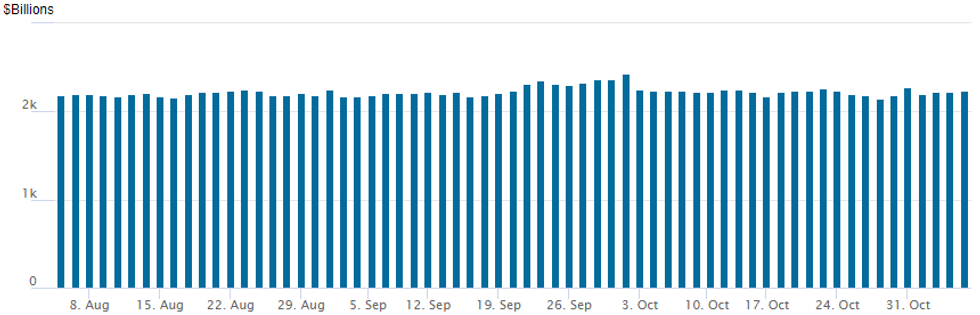

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,230.840B w/ 108 counterparties vs. $2,219.791B in the prior session. Prior record high stands at $2,425.910B on Friday, September 30.

EURODOLLAR/SOFR/TREASURY OPTIONS SUMMARY

- SOFR Options:

- Block, 5,000 SFRG3 94.50/94.75 put spds, 6.0

- Block, 5,000 SFRZ2 95.37/95.43/95.50/95.56 call condors, 2.25

- 1,250 short Dec 94.50/95.00/95.50 put trees

- Block/screen: 3,000 SFRZ2 95.31/95.43/95.56 call flys, 2.5

- Eurodollar Options:

- over 9,000 Dec 96.62 calls, 0.5

- over 5,000 EDM3 94.37 puts

- Treasury Options:

- 5,000 TYG3 110/110.5/111 call flys

- 2,500 TYZ2 109.5/TYH3 107.5 puts, 25

- 4,000 wk2 5Y 106.5/106.75/107/107.25 call condors

- Block, -10,000 TYH3 110.5 calls, 160 vs. 110-13/0.48%

- 4,000 FVZ 108.5 puts

- 5,000 FVZ 106.25 puts, 49.5 ref 105-30.5

- 1,500 TYZ 109 puts, 33 total volume >10.2k

- Block, 10,000 FVZ2 106.25 puts, 43 ref 106-00.75 - same time as 7,500 TUZ2 101-23.12 (0441:03ET)

- Block, 15,000 TYZ2 112.75 calls, 7 ref 109-27.5

- Block, 20,000 TYZ2 112.75 calls, 6 vs. 10,000 FVZ2 106 puts, 39

- 3,000 TYZ2 108 puts, 18

- 4,250 FVZ 106 puts, 40

- 2,000 TYZ 109/110.5 put spds

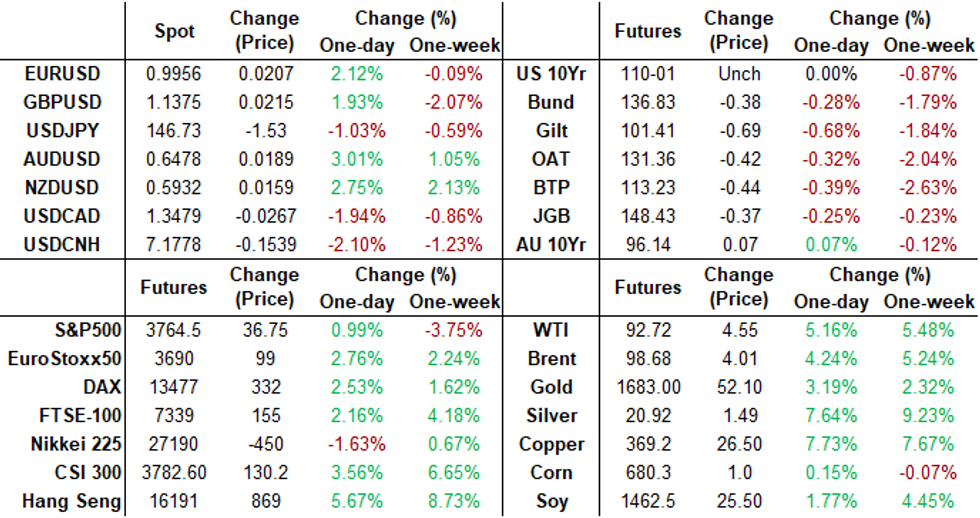

FOREX: Greenback Weakness Extends Ahead Of The Close, AUDUSD Up 3%

- Friday saw a broadly solid US employment report for October, despite a small miss on the unemployment rate. Despite further solid job gains, the US dollar saw a sharp depreciation on Friday with strength in both equity markets but especially in the commodity complex working against the greenback for the majority of Friday trade.

- Potentially one of the dominant drivers were early headlines about possible easing of China covid curbs attracting dip buyers in equities following the data, weighing on the US Dollar, with price action being exacerbated by short-term positioning.

- The USD index is down just shy of two percent and gains in G10 were broad based. CNH is set to post one of its largest advances on record at 2.10%, which certainly filtered through to the likes of AUD and NZD, rising well over 2.5%.

- In similar vein, EURUSD (+2.10%) bounced two full points to trade back above 0.9950 and GBPUSD (+1.85%) reversed the majority of yesterday’s fall which had been pronounced by the Bank of England’s latest downbeat statement.

- Focus next week turns the US Midterm Election and to Thursday’s US CPI print, which may prove pivotal in determining pricing ahead of the December Fed meeting given many Fed officials have been hinting the pace of rate hikes may need to decelerate, despite also signalling a higher terminal rate.

FX: Expiries for Nov07 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9750(E1.2bln), $0.9800(E1.9bln), $0.9850-60(E631mln), $0.9935-55(E1.2bln)

- USD/JPY: Y148.60($650mln)

- GBP/USD: $1.1460-75(Gbp524mln)

- AUD/USD: $0.6425-30(A$872mln), $0.6450(A$750mln)

- USD/CNY: Cny7.1500($1.5bln), Cny7.2000($1.9bln)

Late Equity Roundup, Late Rebound As Metals Surge

Stocks bouncing off midday lows, earlier dovish Fed speak gaining traction again as short end rates rebounded, Dec 2022: cumulative hikes slips 57.3 to 4.40% as Terminal Funds rate holds at 5.155% in June'23.

- Materials and Financials sectors outperforming: SPX eminis currently trading +32 (0.86%) at 3758.25; DJIA +230.73 (0.72%) at 32221.63; Nasdaq + 64.1 (0.6%) at 10402.25.

- SPX leading/lagging sectors: Materials sector continued to gain (+3.11%) -- lead by metals and mining shares as Gold (+3.16%), Silver (+7.54%) and Copper (+7.82%) surge, Freeport McMoran (FCX) +11.06%, Newmont (NEM) +8.04%. Financials a distant second (+1.33%) with banks leading (FifthThird +3.62%, USB +2.77%, SBNY +2.62%). Laggers: HealthCare (-0.14%), Utilities (-0.01%) and Consumer Discretionary (+0.15%).

- Dow Industrials Leaders/Laggers: Goldman Sachs (GS) +7.25 at 356.12, Caterpillar (CAT) +7.23 at 226.49, NIKE (NKE) +4.93 at 95.33. Laggers: United Health (-12.51 at 531.10), Salesforce.Com (CRM) -7.42 at 138.91, Apple (AAPL) -2.52 at 136.36.

E-MINI S&P (Z2): Watching Support

- RES 4: 4100.00 Round number resistance

- RES 3: 4023.44 61.8% retracement of the Aug 16 - Oct 13 downleg

- RES 2: 3981.25 High Sep 14

- RES 1: 3830.59/3928.00 50-day EMA / High Nov 1

- PRICE: 3765.5 @ 1510ET Nov 4

- SUP 1: 3704.25/3641.50 Low Nov 3 / Low Oct 21

- SUP 2: 3590.50/3502.00 Low Oct 17 / 13 and the bear trigger

- SUP 3: 3491.13 50.0% retracement of the 2020 - 2022 bull cycle

- SUP 4: 3453.78 1.618 proj of the Aug 16 - Sep 7 - 13 price swing

S&P E-Minis traded lower Thursday, extending the pullback from 3928.00, the Nov 1 high. Despite the latest retracement, a bull cycle remains in play following the recovery from 3502.00, Oct 13 low. A strong resumption of gains would refocus attention on 3928.00, where a break would confirm the bull theme and open 3981.25, Sep 14 high. Key S/T support to watch is 3641.50, the Oct 21 low. A break would strengthen any developing bearish threat.

COMMODITIES

- WTI Crude Oil (front-month) up $4.58 (5.19%) at $92.74

- Gold is up $50.89 (3.12%) at $1680.45

Monday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/11/2022 | 0645/0745 | ** |  | CH | Unemployment |

| 07/11/2022 | 0700/0800 | ** |  | DE | Industrial Production |

| 07/11/2022 | 0730/0730 |  | UK | DMO Announces Second H2-Nov Linker Synd | |

| 07/11/2022 | 0830/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 07/11/2022 | 0830/0930 | | DE | S&P Global Germany Construction PMI | |

| 07/11/2022 | 0840/0940 | | EU | ECB Lagarde Video Message for EC/ECB Conference | |

| 07/11/2022 | 0930/1030 | * | | EU | Sentix Economic Index |

| 07/11/2022 | 0930/1030 | | EU | ECB Panetta Panels EC/ECB Conference | |

| 07/11/2022 | - | *** |  | CN | Trade |

| 07/11/2022 | - | | EU | COP 27 Begins | |

| 07/11/2022 | - | | EU | ECB Panetta at Eurogroup meeting | |

| 07/11/2022 | 1630/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 07/11/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 07/11/2022 | 2000/1500 | * | | US | Consumer Credit |

| 07/11/2022 | 2040/1540 | | US | Fed's Loretta Mester and Susan Collins | |

| 07/11/2022 | 2300/1800 | | US | Richmond Fed's Tom Barkin |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.