- MNI Fed Preview-Apr 2024: Disinflation Delayed, Not Yet Denied

- MNI US-CHINA: Tsy Sec Yellen: Sanctioning Chinese Banks Is A "Tool That Is Available"

- MNI BOE POLICY: BOE Split Over Measures Of Inflation Persistence

- MNI US DATA: Real GDP and Consumer Spending Misses But Firmer Underlying Details

- MNI US DATA: Jobless Claims Better Than Expected Again

US

Fed Preview-Apr 2024 (MNI): Disinflation Delayed, Not Yet Denied: Persistently high inflation readings to start the year have shaken the FOMC’s confidence in initiating rate cuts, but the April 30-May 1 meeting is too soon for them to reconsider their easing bias.

- Though Chair Powell could confirm that a June cut is a doubtful prospect unless major surprises emerge, he is likely to affirm that the FOMC currently sees a higher-for-longer policy as appropriate and sufficient to quell inflation.

- In other words, rate hikes are not at all the Committee’s base case – though the degree to which Powell plays down this possibility will be key to the market’s takeaway from the meeting.

- Changes to the Statement are likely to be limited, with the forward rate guidance remaining intact, though the Committee’s characterization of recent inflation will be scrutinized for any hawkish shift.

NEWS

US-CHINA (MNI): Yellen: Sanctioning Chinese Banks Is A "Tool That Is Available": US Treasury Secretary Janet Yellen spoke to Reuters on a range of issues related to the US-China relationship. Asked about potential sanctions on Chinese banks if they facilitate transactions on ‘dual use’ goods to Russia’s military. Yellen says: “There’s an executive order that the President has signed which gives Treasury the power to sanction foreign banks, in China or other places, that are facilitating the flow of military goods to Russia. That’s an important power and one we would be prepared to use if necessary."

BOE POLICY (MNI): BOE Split Over Measures Of Inflation Persistence: Uncertainty over when the Bank of England is likely to begin cutting rates is being increased by divisions within the Monetary Policy Committee over how much weight to place on different measures of the persistence of service sector inflation. MPC policy statements have stressed that components of services prices are continuing to feed consumer price inflation as goods inflation fades, but public comments by its members point to a lack of agreement over how much the different measures matter.

ISRAEL (MNI): US & 17 Other Leaders Issue Joint Statement Calling For Hostage Release: US President Joe Biden and 17 other world leaders have released a joint statement calling on Hamas to release its Israeli hostages as a pathway to end the Gaza crisis. The statement claims that the "deal on the table to release the hostages would bring an immediate and prolonged ceasefire in Gaza, that would facilitate a surge of additional necessary humanitarian assistance to be delivered throughout Gaza, and lead to the credible end of hostilities."

FRANCE (MNI): Macron-'Europe Should Show It Is Not A Vassal Of The US': French President Emmanuel Macron making a wide-ranging speech on foreign and security policy at the Sorbonne University in Paris. Making some fairly headline-grabbing comments Macron claims that “There is a risk our Europe could die,” adding that the continent must review its growth model, "because the rules of the game have changed", and that "Europe is at risk of impoverishment".

RUSSIA/CHINA (MNI): Putin To Visit China In May: Wires carrying comments from Russian President Vladimir Putin confirming that he will travel to China in May. It will be Putin's first international trip since he secured a new six-year term at the Russian Presidential Election in March.

SECURITY (MNI): Lukashenko Adds To Heightened Nuclear Rhetoric: Wires carrying comments from Belarussian President Alexander Lukashenko appearing to threaten the preemptive use of nuclear weapons, and confirming the presence of "dozens" of Russian nuclear weapons in Belarus.

HUNGARY (MNI): Minister-Xi's Visit Confirmed For 8-10 May: Hungarian cabinet minister Gergely Gulyas has confirmed that Chinese President Xi Jinping's visit to Hungary will take place 8-10 May.

POLAND (MNI): PM Announces Reshuffle Ahead Of EP Elections: Wires reporting that Prime Minister Donald Tusk has confirmed that a cabinet reshuffle will take place on 10 May, almost a full month ahead of the European Parliament elections.

SCOTLAND (MNI): SNP Loses Majority, Could Lose Power If Greens/Alba Withhold Support: The governing pro-independence Scottish National Party (SNP) has lost its majority in the Scottish Parliament following the collapse of its coalition deal with the left-wing environmentalist Greens.

US TSYS Weekly Claims Miss, Strong Core PCE Weighs on Tsys, 7Y Sale In-Line

- Treasury futures held weaker levels after this morning's lower than expected weekly claims and strong core PCE (3.7% vs. 3.4% est) saw chances of a rate cut in 2024 evaporate.

- Jobless claims printed a seasonally adjusted 207k (cons 215k) in the week to Apr 20 after an unrevised 212k. Meanwhile, Real GDP was softer than expected in Q1 at 1.6% (cons 2.5) after 3.4% in Q4 (no revisions in this advance release), and Pending home sales were stronger than expected in March as they increased 3.4% M/M (cons 0.4) after 1.6% in Feb.

- Projected rate cut pricing vs. pre-data levels: May 2024 -2.6% w/ cumulative -2.6bp at 5.322%; June 2024 at -8.9% from -16.2% earlier w/ cumulative rate cut -2.9bp at 5.300%. July'24 cumulative at -8.6bp from -12.1bp, Sep'24 cumulative -18.6bp from -24.4bp.

- Little reaction in Tsys futures (TYM4 107-13.5 last) after the $44B 7Y note auction (91282CKN0) in line with WI of 4.716%; bid-to-cover slips to the lowest since November at 2.48x vs. 2.61x last month.

- Focus turns to Friday's Data Calendar: Personal Income/Spending, UofM Sentiment, while May Treasury options expire.

OVERNIGHT DATA

US DATA (MNI): Jobless Claims Better Than Expected Again: Initial jobless claims printed a seasonally adjusted 207k (cons 215k) in the week to Apr 20 after an unrevised 212k.

- The four-week average fell 2k to 213k after three weeks at 215k. It’s off January lows of 201k but still low historically vs the 218k averaged in 2019 for perspective.

- Continuing claims came in at a seasonally adjusted 1781k (cons 1814k) in the week to Apr 13 – covering a payrolls reference period – after a downward revised 1796k (initial 1812k).

- It leaves continuing claims back at the lower end of their recent narrow range. It’s also the third consecutive beat for initial claims vs the second weekly beat for continuing claims.

US DATA (MNI): Real GDP and Consumer Spending Misses But Firmer Underlying Details: Real GDP was softer than expected in Q1 at 1.6% (cons 2.5) after 3.4% in Q4 (no revisions in this advance release).

- Relative to expectations, personal consumption disappointed at 2.5% (cons 3.0) whilst net exports were a larger drag than the Atlanta Fed’s GDPNow had envisaged (-0.86pps vs -0.5pps) along with the contribution from inventories (-0.35pps vs -0.1pps).

- It meant the contribution from final sales to domestic purchases was still strong though, adding 2.8pps after two quarters averaging 3.6pps.

- Within personal consumption, goods spending was extremely weak at -0.4% after +3.0% considering the strength in the retail sales control group, but services helped offset with a strong +4.0% after +3.4% for its strongest quarter since 3Q21.

- The strength in domestic demand was further evident by imports increasing 7.2% on the quarter (goods 6.8%, services 9.0%).

US DATA (MNI): Pending Home Sales Surprise Higher After Lagging Existing Lift: Pending home sales were stronger than expected in March as they increased 3.4% M/M (cons 0.4) after 1.6% in Feb.

- Considering their nature, they should lead existing home sales by 1-2 months but surprisingly missed the latest uplift in the latter.

- Nevertheless, today’s uplift in pending sales is starting to push sales away from multi-year lows:

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 307.7 points (-0.8%) at 38154.05

- S&P E-Mini Future down 18 points (-0.35%) at 5089.75

- Nasdaq down 72.8 points (-0.5%) at 15639.82

- US 10-Yr yield is up 6 bps at 4.7019%

- US Jun 10-Yr futures are down 11/32 at 107-12.5

- EURUSD up 0.0036 (0.34%) at 1.0735

- USDJPY up 0.22 (0.14%) at 155.56

- Gold is up $19.48 (0.84%) at $2335.80

- European bourses closing levels:

- EuroStoxx 50 down 50.87 points (-1.02%) at 4939.01

- FTSE 100 up 38.48 points (0.48%) at 8078.86

- German DAX down 171.42 points (-0.95%) at 17917.28

- French CAC 40 down 75.21 points (-0.93%) at 8016.65

US TREASURY FUTURES CLOSE

- 3M10Y +7.923, -71.966 (L: -85.95 / H: -69.057)

- 2Y10Y -0.634, -29.357 (L: -30.188 / H: -27.264)

- 2Y30Y -2.211, -17.991 (L: -19.023 / H: -12.64)

- 5Y30Y -1.105, 10.192 (L: 8.518 / H: 14.877)

- Current futures levels:

- Jun 2-Yr futures down 3.75/32 at 101-13.75 (L: 101-12 / H: 101-20.125)

- Jun 5-Yr futures down 7.5/32 at 104-25.75 (L: 104-20.25 / H: 105-07.75)

- Jun 10-Yr futures down 11/32 at 107-12.5 (L: 107-04 / H: 108-01)

- Jun 30-Yr futures down 17/32 at 113-12 (L: 112-27 / H: 114-11)

- Jun Ultra futures down 22/32 at 119-1 (L: 118-14 / H: 120-07)

US 10Y FUTURE TECHS: (M4) Resumes Its Downtrend

- RES 4: 110-06 High Apr 4

- RES 3: 109-26+ High Apr 10

- RES 2: 109-22+ 50-day EMA

- RES 1: 108-22+ High Apr 19 and the 20-day EMA

- PRICE: 107-12 @ 1531 ET Apr 25

- SUP 1: 107-07+ 76.4% of the Oct - Dec ‘23 bull leg (cont)

- SUP 2: 106-27 2.764 proj of Dec 27 - Jan 19 - Feb 1 price swing

- SUP 3: 106-18 Base of a bear channel drawn from the Feb 1 low

- SUP 4: 106-08 3.00 proj of Dec 27 - Jan 19 - Feb 1 price swing

The trend outlook in Treasuries is unchanged and the direction is down. The contract has traded to a fresh cycle low today. MA studies are in a bear-mode set-up too, highlighting a clear downtrend. Note that the recent consolidation appears to have been a flag formation - a bearish continuation pattern. Sights are on 107.07+ (tested), a Fibonacci retracement. A break would open 106-27, a Fibonacci projection. Firm resistance is 108-22+, the 20-day EMA.

SOFR FUTURES CLOSE

- Jun 24 -0.025 at 94.710

- Sep 24 -0.055 at 94.850

- Dec 24 -0.075 at 95.010

- Mar 25 -0.085 at 95.185

- Red Pack (Jun 25-Mar 26) -0.085 to -0.075

- Green Pack (Jun 26-Mar 27) -0.07 to -0.06

- Blue Pack (Jun 27-Mar 28) -0.06 to -0.05

- Gold Pack (Jun 28-Mar 29) -0.05 to -0.045

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00131 to 5.31816 (+0.00006/wk)

- 3M +0.00090 to 5.32445 (+0.00035/wk)

- 6M -0.00805 to 5.28965 (-0.00885/wk)

- 12M -0.02235 to 5.18826 (+0.00045/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.778T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $673B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $664B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $71B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $248B

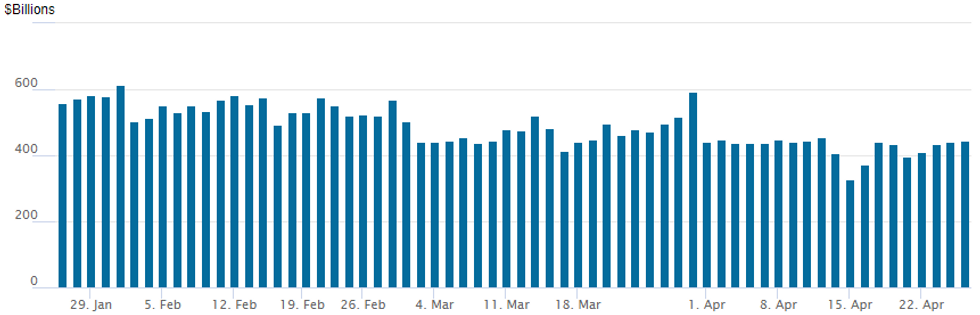

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage inches up to $443.928B vs. $441.215B Wednesday. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

- Meanwhile, the latest number of counterparties recedes to 74 vs. 82 prior.

PIPELINE $1.1B GXO Logistics 2Pt Debt Launched

Date $MM Issuer (Priced *, Launch #)

4/25 $1.1B #GXO Logistics $600M 5Y +165, $500M 10Y +195

4/25 $Benchmark Arab Petroleum Inv Corp 5Y SOFR+115

FOREX USD Index Reverses Data-Inspired Spike, Approaching Session Lows

- The greenback has been slowly edging lower over the course of the US session as the post-data spike for the USD index slowly recedes. Most G10 pairs are now trading back towards pre-data levels, with the likes of EURUSD and GBPUSD hovering just below the best levels of the week. The reaction to the above estimate core PCE price index appears to have been tempered by the poorer GDP print and keeps G10 currency market adjustments relatively contained.

- JPY weakness was once again the market focus on Thursday, as USDJPY's ascent continued, printing a new cycle high of 155.75. Markets continue to test the resolve of the Japanese authorities, as several 'lines in the sand' at Y152.00 and Y155.00 go by with little sign of intervention. The BoJ are expected to discuss the weakening currency at their ongoing policy meeting - on which MNI understands that the USDJPY at current levels is insufficient to prompt any immediate rate hike from the BoJ.

- Overnight JPY options vols are pricing a sizeable swing across the BoJ decision on Friday, with markets pricing options at their most sensitive level of the year so far.

- As noted, GBP trades more favourably despite the lower equity benchmarks and higher US yields. The trend condition in GBPUSD remains bearish and this week’s recovery appears to be a correction. However, initial resistance at 1.2512, the 20-day EMA, has been pierced and eyes will be on further strength towards 1.2586, the 50-day EMA.

- In emerging markets, USDMXN experienced some sharp volatility on the US data, bouncing over 2% from session lows and briefly testing resistance around 17.38 as the initial impact on stocks and bonds pressured the renewed sensitivity of the peso.

- The BOJ decision and press conference takes focus Friday before the US PCE Core Deflator crosses. UMich consumer sentiment and inflation expectations will round off the week’s data calendar.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 26/04/2024 | 2301/0001 | ** |  | UK | Gfk Monthly Consumer Confidence |

| 26/04/2024 | 2330/0830 | ** |  | JP | Tokyo CPI |

| 26/04/2024 | 0130/1130 | ** |  | AU | Trade price indexes |

| 26/04/2024 | 0200/1100 | *** | | JP | BOJ Policy Rate Announcement |

| 26/04/2024 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 26/04/2024 | 0800/1000 | ** |  | EU | M3 |

| 26/04/2024 | 0800/1000 | ** | | EU | ECB Consumer Expectations Survey |

| 26/04/2024 | 0800/1000 | | EU | ECB's De Guindos at Academia Europea Leadership | |

| 26/04/2024 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 26/04/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 26/04/2024 | 1500/1100 |  | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 26/04/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |