Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- MNI EXCLUSIVE: Fed Sees Covid Surge as Mounting Recovery Risk

- MNI BRIEF: Fed Studying Climate Change Impact On Dual Mandate

- MNI SOURCES: VTC Not Right Format For EU Budget Deal Talks

- IMF WARNS RECOVERY MAY BE LOSING MOMENTUM, RISKS VERY HIGH, Bbg

- CNBC: Schumer says McConnell has agreed to resume negotiations over Covid-19 stimulus

US

FED: The latest Covid surge is putting the U.S. economic recovery at greater risk than Federal Reserve policymakers had anticipated, forcing the central bank to consider additional monetary easing even as officials acknowledge the prospect of stronger growth once a vaccine is widely rolled out, current and former officials tell MNI. For more see 11/19 MNI Policy MainWire at 1022ET.

FED: The Fed will continue to explore how climate change poses risks to markets and the central bank's dual mandate, Andreas Lehnert, director of the division of financial stability at the Fed board of governors, said Thursday.- "Just as with financial stability there is the potential for some of these risks and events and potential amplification mechanisms to cause a miss on the dual mandate so it is incumbent to understand that set of risks," Lenhnert said. Earlier this month the Fed formally called out climate change as a risk for the first time in its semiannual report.

- "Markets can be fairly nonlinear when it comes to novel risks," Lehnert said in a discussion at an OMFIF event. "All these things interact with the classic vulnerabilities."

- Cleveland Fed President Loretta Mester speaks on Bloomberg Television, saying that she sees Fed policy as being in a 'good place', despite her concern about as slowing economy amid rising COVID cases and the lack of fiscal policy aid.

- While she says the Fed will use all its tools to keep monetary policy "very accommodative", she says that it is not clear to her that monetary easing is the right tool to address the situation, and that what the economy needs is fiscal assistance.

- As such, she says she will not prejudge the outcome of the December FOMC meeting.

- For context, Mester's an FOMC voter this year. She said last month that she was 'comfortable' with where the Fed was on fwd guidance and asset purchases, but also said at the time 'I can imagine wanting to shift to longer-term Treasuries'.

- As such, while her comments certainly suggest she may not be the most vociferous voice in favor of easing action at next month's meeting, she may be willing to go along with some changes to current policy were they to otherwise see wide support (for instance extending the duration of Tsy purchases, which appears to be one of the options on the table).

EUROPE

EU: European Union leaders meeting Thursday decided that a video conference is not an appropriate format in which to broker a politically difficult compromise with Poland and Hungary over their objections to attaching Rule of Law conditions to the next EU budget, a senior Brussels official said. For more see 11/19 MNI Policy Main Wire at 1541ET.

OVERNIGHT DATA

US JOBLESS CLAIMS +31K TO 742K IN NOV 14 WK

US PREV JOBLESS CLAIMS REVISED TO 711K IN NOV 07 WK

US CONTINUING CLAIMS -0.429M to 6.372M IN NOV 07 WK

- Philadelphia Fed Manufacturing Business Outlook Survey index for current activity comes in at 26.3 in Nov, vs 22.5 expected, 32.3 prior. Moderation was seen in most subcategories, with employment notably improving - and the outlook for future prospects was seen waning.

- New orders down 5 points to 37.9, current shipments down 22 points to 24.9, current employment up 15 points to 27.2, and average workweek roughly unchanged at 25.7. Prices paid up 10 points to 38.9, prices received up 11 points to 25.4.

- As for the outlook, the future general activity index fell 18 points to 44.3, future new orders down 4 points to 48.1, future shipments down 9 points to 43.1, and future employment down 10 points to 36.2.

- Special questions: "In this month's special questions, the firms were asked to forecast the changes in the prices of their own products and for U.S. consumers over the next four quarters. Regarding their own prices, the firms' median forecast was for an increase of 2.0 percent, the same as reported when the question was asked in August. The firms' actual price change over the past year was 1.0 percent."

- Responses were collected Nov 9-16, so after the election.

- Tsys held onto gains after the report, which also coincided with the release of data showing a bigger-than-expected increase in weekly initial jobless claims.

- "Another spectacular month" as October existing home sales beat expectations, rising 4.3% to 6.85M SAAR vs 6.47M expected.

- October sales +26.6%% YOY, offsetting the spring market loses, says NAR economist Lawrence Yun.

- Median home price +16% YOY to record USD313,000, due to insufficient supply, strong demand, and higher sales of larger, more expensive homes.

- More than 7 in 10 homes sold in October, 72% were on the market for less than a month.

- Average 21 days on market is meets previous record low; 2.5 months supply is lowest inventory count all-time.

- First time home buyers were responsible for 32% of sales in October, up from 31% in both September and October 2019.

MARKETS SNAPSHOT

- DJIA up 65.74 points (0.22%) at 29315.57

- S&P E-Mini Future up 14.5 points (0.41%) at 3558.25

- Nasdaq up 102.9 points (0.9%) at 11852.43

- US 10-Yr yield is down 2.1 bps at 0.8488%

- US Dec 10Y are up 6.5/32 at 138-12.5

- EURUSD up 0.002 (0.17%) at 1.1848

- USDJPY down 0.03 (-0.03%) at 103.82

- WTI Crude Oil (front-month) down $0.01 (-0.02%) at $41.41

- Gold is down $6.17 (-0.33%) at $1862.93

- European bourses closing levels:

- EuroStoxx 50 down 30.2 points (-0.87%) at 3451.97

- FTSE 100 down 50.89 points (-0.8%) at 6334.35

- German DAX down 115.73 points (-0.88%) at 13086.16

- French CAC 40 down 36.79 points (-0.67%) at 5474.66

US TSY SUMMARY: Subdued Rally For Rates, US$ Reverses Early Bid

Despite the breadth of the move, the risk-off rally in rates was rather subdued Thursday, COVID-19 spread and concern over stricter quarantine measures supportive for rates though equities managed to break session range late to trade modestly higher.

- Long end outperformed coming into the session with two-way flow from bank portfolios overnight, light fast$ and prop buying shorts to intermediates vs. bank and swap-tied selling. Decent deal-tied hedging.

- Tsys maintained decent support all session, heavy volumes a little deceiving as Dec/Mar futures rolling picked up in earnest, TYZ/TYH over 320,000 by the bell.

- Equities surged to new session highs late, apparently on the back of fiscal relief hopes after Senate Majority Leader Mitch McConnell "agreed to resume negotiations with Democrats over a potential new Covid-19 bill as cases continue to surge around the country, Senate Minority Leader Chuck Schumer said" CNBC.

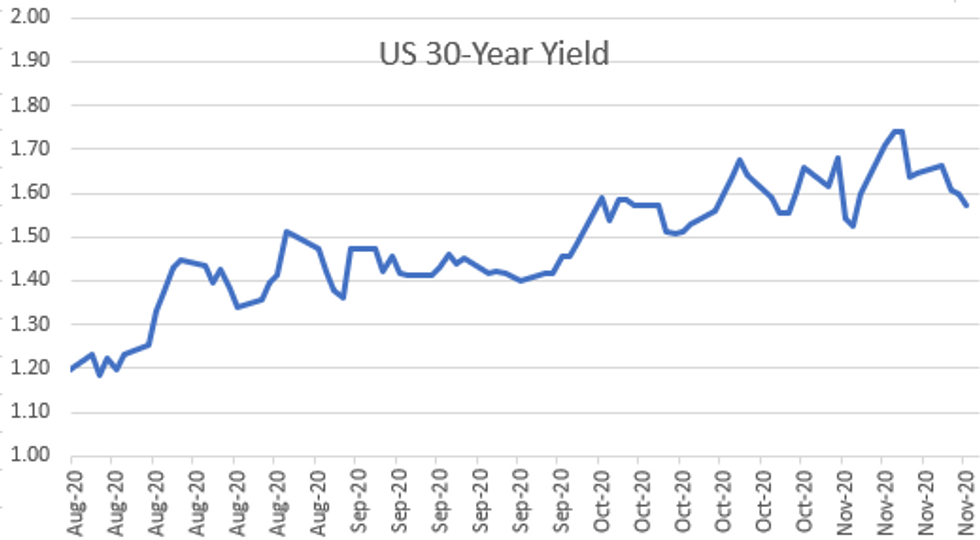

- The 2-Yr yield is down 0.4bps at 0.1693%, 5-Yr is down 1bps at 0.3857%, 10-Yr is down 1.6bps at 0.8537%, and 30-Yr is down 2.3bps at 1.5771%.

US TSY FUTURES CLOSE: Rates Retain Bid Despite Equity Bounce

Despite the breadth of the move, the risk-off rally in rates was rather subdued Thursday, COVID-19 spread and concern over stricter quarantine measures supportive for rates though equities managed to break session range late to trade modestly higher. Yield curves flatter, update:

- 3M10Y -1.111, 78.292 (L: 76.444 / H: 80.377)

- 2Y10Y -1.730, 67.754 (L: 67.341 / H: 69.061)

- 2Y30Y -2.608, 139.866 (L: 138.905 / H: 142.34)

- 5Y30Y -1.890, 118.424 (L: 117.862 / H: 120.459)

- Current futures levels:

- Dec 2Y up 0.25/32 at 110-12 (L: 110-11.62 / H: 110-12.25)

- Dec 5Y up 2/32 at 125-17.75 (L: 125-16 / H: 125-19)

- Dec 10Y up 6/32 at 138-12 (L: 138-07 / H: 138-14.5)

- Dec 30Y up 28/32 at 173-13 (L: 172-24 / H: 173-18)

- Dec Ultra 30Y up 1-29/32 at 217-28 (L: 216-18 / H: 218-17)

US TSY FUTURES: December/March Futures Roll Update

Dec/Mar roll volume accelerates ahead Nov 30 "first notice" date approaches, position holders contend with shortened Thanksgiving holiday workweek. Dec futures won't expire until mid-late December: 10s, 30s and Ultras on 12/21; 2s & 5s 12/31.

- TUZ/TUH appr 104,900 0.25 last; 7% complete

- FVZ/FVH appr 268,900 -10.0 last; 7% complete

- TYZ/TYH appr 323,000 12.5 last; 7% complete

- UXYZ/UXYH under 98,100, 19.0 last; 7% complete

- USZ/USH 81,300, -1-10.5 last; 8% complete

- WNZ/WNH 156,300, 1-20.5 last; 4% complete

US EURODLR FUTURES CLOSE: Mostly Bid

Mostly bid, steady at points in Whites-Greens, long end leading but off session lows. Lead quarterly EDZ0 holds bid since 3M LIBOR set -0.01112 to 0.21263% (-0.00937/wk).

- Dec 20 +0.005 at 99.752

- Mar 21 +0.010 at 99.790

- Jun 21 +0.010 at 99.795

- Sep 21 steady at 99.785

- Red Pack (Dec 21-Sep 22) steady to +0.010

- Green Pack (Dec 22-Sep 23) steady to +0.010

- Blue Pack (Dec 23-Sep 24) +0.015 to +0.015

- Gold Pack (Dec 24-Sep 25) +0.025 to +0.030

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles

- O/N +0.00013 at 0.08238% (-0.00087/wk)

- 1 Month -0.00100 to 0.14550% (+0.00912/wk)

- 3 Month -0.01112 to 0.21263% (-0.00937/wk)

- 6 Month -0.00138 to 0.25550% (+0.00950/wk)

- 1 Year -0.00012 to 0.33863% (-0.00075/wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $60B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $163B

- Secured Overnight Financing Rate (SOFR): 0.07%, $941B

- Broad General Collateral Rate (BGCR): 0.05%, $340B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $318B

- (rate, volume levels reflect prior session)

- Tsy 7Y-20Y, $3.601B accepted vs. $9.870B submission

- Next scheduled purchases:

- Fri 11/20 1010-1030ET: Tsy 0Y-2.25Y, appr $12.825B

PIPELINE: Allstate Launched Late

- Date $MM Issuer (Priced *, Launch #)

- 11/19 $3B #Charter Comm's $1B +11Y +147, $650M tap 30Y +207, $1.35B +40Y +227

- 11/19 $1.8B #AES Corp $800M 5Y +100, $1B 10Y +160

- 11/19 $1.2B #Allstate 5Y +40a, 10Y +70a

- 11/19 $555M #Uzbekistan 10Y 3.7%

- 11/19 $500M *Goldman Sachs +5Y +255

- 11/19 $500M *Massachusetts Electric 10Y +88

- 11/?? $Benchmark Rep of Serbia

FOREX: US$ Sheds Gains

USD shed early gains from late morning through the second half, finishing weaker as equities bounced to session highs on hopes of fiscal relief negotiations resuming. Earlier, covid spikes and lockdown risk kept currency underpinned on safe haven. All eyes today were on EM and especially the CBRT.

- CBRT didn't disappoint and hiked 475bps to 15% as economists expected.

- USDTRY dropped 20 big figures on the release and made an attempt at the 100d MA situated today at 7.5063 (printed 7.5151 low so far).

- SARB kept their rate unchanged at 3.5% as expected, which provided initial gains for the Rand, but the move quickly reversed.

- SARB noted data dependency, and USDZAR is now stable at 15.50 at the time of typing.

- Cable fell from 1.3212 down to 1.3196, following report that one of Barnier's Brexit negotiator tested positive for Civid and that talks were on hold for a short period of time.

- Cable quickly recovered, with the downside initial dip looking to have been mostly algo and FM led. Cable at 1.3275.

- EURUSD up 0.0024 (0.2%) at 1.1877

- USDJPY down 0.01 (-0.01%) at 103.81

EGBs-GILTS CASH CLOSE: Safe Havens Benefit From COVID Headlines

Thursday saw a risk-off move into safe havens in the morning and the late afternoon, while periphery spreads came in from early wides (Greece excepted).

- COVID lockdown concerns boosted Bunds and Gilts early, and the suspension of the Brexit talks at the Frost/Barnier level (due to a participant from the EU side testing COVID-positive) helped buoy them later on.

- Focus on Brexit will continue Friday as we enter another key phase, with EU budget wrangling also getting attention, particularly in the case of peripheries.

- Friday's docket is headed by UK Oct retail sales. ECB speakers also feature (incl Lagarde and Weidmann). Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is down 0.8bps at -0.735%, 5-Yr is down 1bps at -0.748%, 10-Yr is down 1.7bps at -0.571%, and 30-Yr is down 2.5bps at -0.174%.

- UK: The 2-Yr yield is down 0.3bps at -0.029%, 5-Yr is down 0.8bps at 0.008%, 10-Yr is down 1.4bps at 0.323%, and 30-Yr is down 1.1bps at 0.92%.

- Italian BTP spread up 0.4bps at 121.3bps

- Spanish bond spread up 0.6bps at 64.1bps

- Portuguese PGB spread up 0.2bps at 60.6bps

- Greek bond spread up 4.4bps at 126.2bps

UP TODAY

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.