Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI POLICY: Evans Sees Fed QE For Quite a While as Prices Lag

- MNI BRIEF: Fed's Evans May Reconsider Adjusting QE in Spring

- JOHNSON ORDERS NATIONAL LOCKDOWN ACROSS ENGLAND STARTING JAN. 5, bbg

- U.K TO IMPOSE TIER 4 RESTRICTIONS EVERYWHERE: ITV'S PESTON, Bbg

- CHINA COULD ASK U.S. COMPANIES TO REVEAL MILITARY TIES: GLOBAL TIMES

US

FED: The Federal Reserve will keep buying debt and hold interest rates close to zero for a long time as inflation averages less than 2%, even if vaccines bring the pandemic under control this year, Chicago President Charles Evans said Monday.

- "To meet our objectives and manage risks, the Fed's policy stance will have to be accommodative for quite a while. Economic agents should be prepared for a period of very low interest rates and an expansion of our balance sheet as we work to achieve both our dual mandate objectives," Evans said in remarks prepared for the Allied Social Science Associations annual meeting. For more, see 01/04 MNI Policy Mainwire at 1035ET.

EUROPE

UK: PM Johnson To Address Nation At 2000GMT As Lockdown Speculation Intensifies

- UK PM Boris Johnson is to address the nation at 2000GMT (2100CET, 1500ET) this evening, with the expectation that he will announced a further tightening of COVID-19 restrictions, and potentially a full lockdown similar to that imposed in March 2020.

- No. 10 spokesman said 'The spread of the new variant of COVID-19 has led to rapidly escalating case numbers across the country. The PM is clear that further steps must now be taken to arrest this rise and to protect the NHS and save lives. He will set those out this evening.'

- Unclear whether another lockdown will result in additional economic support measures from the Treasury.

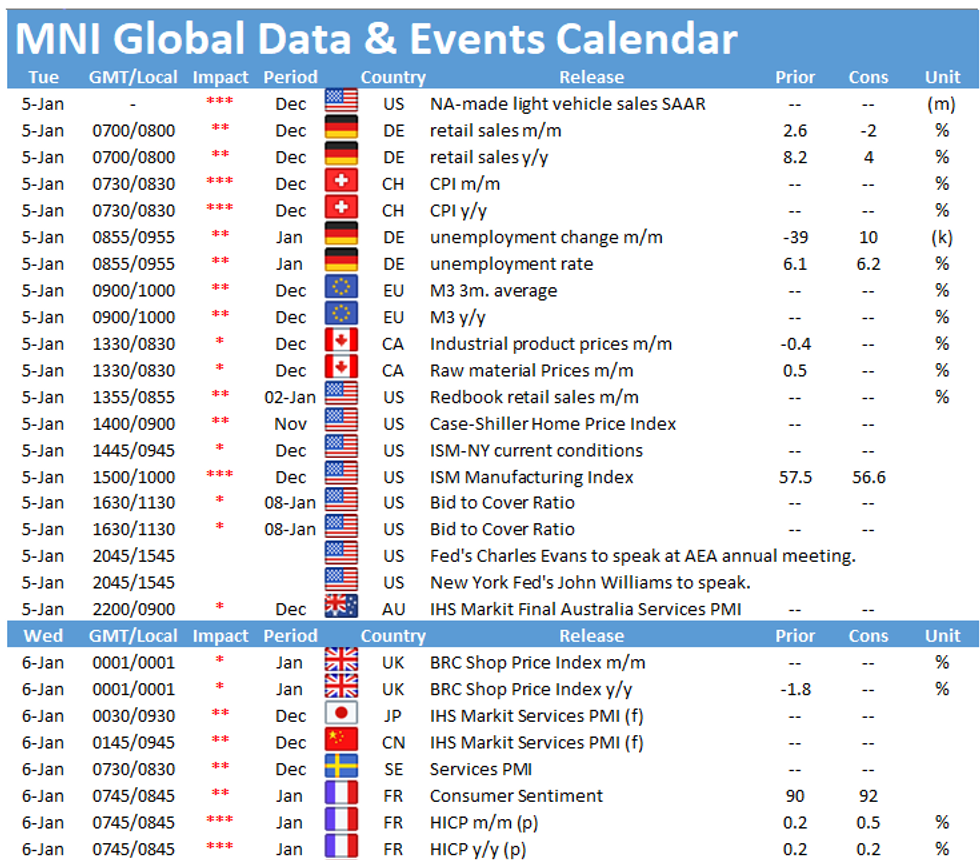

OVERNIGHT DATA

US NOV CONSTRUCT SPENDING +0.9%

US NOV PRIVATE CONSTRUCT SPENDING +1.2%

US NOV PUBLIC CONSTRUCT SPENDING -0.2%

US DATA: FINAL DEC MFG PMI 57.1 VS 56.3 EXP., 56.5 FLASH

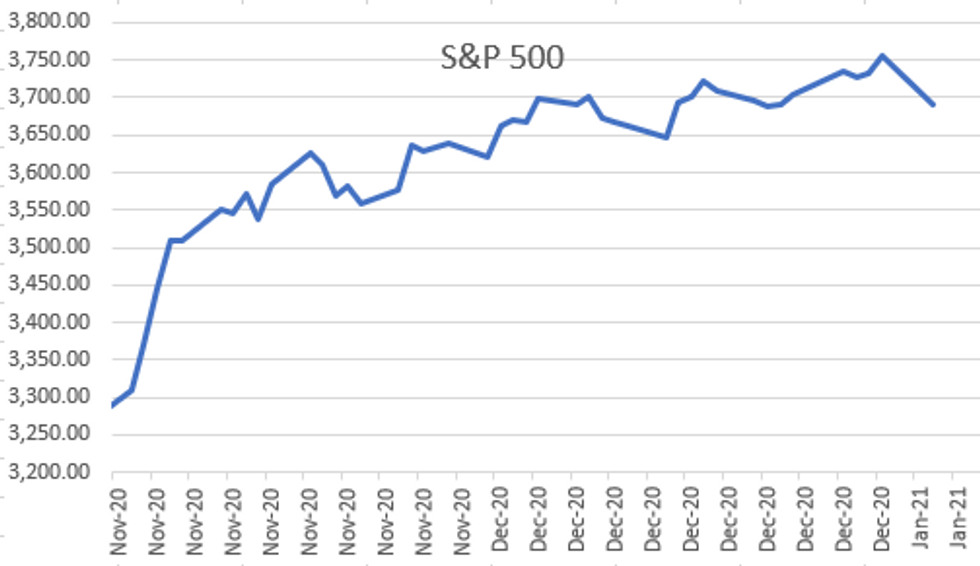

MARKETS SNAPSHOT

- DJIA down 472.72 points (-1.54%) at 30138.38

- S&P E-Mini Future down 65.75 points (-1.75%) at 3683.5

- Nasdaq down 213.4 points (-1.7%) at 12677.29

- US 10-Yr yield is unchanged 0 bps at 0.9132%

- US Mar 10Y are up 1/32 at 138-3.5

- EURUSD up 0.0037 (0.3%) at 1.2252

- USDJPY down 0.07 (-0.07%) at 103.14

- WTI Crude Oil (front-month) down $0.98 (-2.02%) at $47.54

- Gold is up $43.64 (2.3%) at $1942.32

- EuroStoxx 50 up 11.75 points (0.33%) at 3564.39

- FTSE 100 up 111.36 points (1.72%) at 6571.88

- German DAX up 7.96 points (0.06%) at 13726.74

- French CAC 40 up 37.55 points (0.68%) at 5588.96

US TSY SUMMARY

Rates bounced off early weakness to new session highs by midday as equities steadily reversed gains into the close.

- Decent jump in volumes: (TYH>1.15M after the bell), early surge as futures sell-off, long end leading move (10Y B/E rate 2Y high at 2.0025%; 10YY +.0317 at 0.9448%; 30YY +.0355 at 1.6804%). No obvious driver on early rate sales, potential unwind of extension trades going into year end, participants eager to get 2021 underway.

- Steady risk-on unwind followed as equities came under consistent sell pressure all day: likely combination of position squaring ahead GA run-offs Tuesday, political sideshow Wednesday w/electoral vote count; ongoing angst over Covid lockdown measures w/UK PM Johnson calling for national lockdown starting Tuesday.

- More practical position squaring ahead Friday's Dec employ data (+62k est vs. +245k prior).

- Jump in corporate issuance after weeks of inaction, over $27B issuance spurred deal-tied hedging in second half.

- The 2-Yr yield is down 0.8bps at 0.1132%, 5-Yr is down 1bps at 0.3513%, 10-Yr is unchanged at 0.9132%, and 30-Yr is up 0.7bps at 1.6522%.

US TSY FUTURES CLOSE:

Rates trading steady/mixed after the bell, well off early session lows as risk appetite evaporated since the open. Hedging of over $27B high-grade debt issuance helped keep rates in check. Yield curves steeper/off highs.

- 3M10Y +1.515, 84.212 (L: 82.373 / H: 87.04)

- 2Y10Y +1.091, 80.105 (L: 78.743 / H: 82.85)

- 2Y30Y +2.06, 154.247 (L: 151.98 / H: 156.679)

- 5Y30Y +2.26, 130.516 (L: 128.231 / H: 131.165)

- Current futures levels:

- Mar 2Y steady at at 110-15.62 (L: 110-15.12 / H: 110-15.87)

- Mar 5Y up 1/32 at 126-6.25 (L: 126-02.25 / H: 126-07)

- Mar 10Y up 1/32 at 138-3.5 (L: 137-26 / H: 138-05.5)

- Mar 30Y down 8/32 at 172-30 (L: 172-04 / H: 173-11)

- Mar Ultra 30Y down 21/32 at 212-29 (L: 211-18 / H: 213-26)

US EURODLR FUTURES CLOSE:

Futures trading mostly higher after the bell, near top end of range. Lead quarterly EDH1 held marginal gain since 3M LIBOR set -0.00113 to 0.23725% (-0.00173 net last wk).

- Mar 21 +0.005 at 99.835

- Jun 21 +0.005 at 99.840

- Sep 21 +0.005 at 99.835

- Dec 21 +0.010 at 99.80

- Red Pack (Mar 22-Dec 22) +0.005 to +0.010

- Green Pack (Mar 23-Dec 23) +0.005 to +0.010

- Blue Pack (Mar 24-Dec 24) steady to +0.005

- Gold Pack (Mar 25-Dec 25) steady to +0.005

US TSY: Short Term Rates

US DOLLAR LIBOR: Latest settles:

- O/N +0.00700 at 0.08463% (-0.00337 net last wk)

- 1 Month -0.00413 to 0.13975 (-0.00123 net last wk)

- 3 Month -0.00113 to 0.23725% (-0.00173 net last wk)

- 6 Month -0.00175 to 0.25588% (-0.00903 net last wk)

- 1 Year -0.00125 to 0.34063% (+0.00150 net last wk)

- Daily Effective Fed Funds Rate: 0.09% volume: $34B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $76B

- Secured Overnight Financing Rate (SOFR): 0.07%, $1.095T

- Broad General Collateral Rate (BGCR): 0.06%, $351B

- Tri-Party General Collateral Rate (TGCR): 0.06%, $340B

- (rate, volume levels reflect prior session)

- Tsy 2.25Y-4.5Y, $8.801B accepted vs. $21.593B submission

- Next scheduled purchase:

- Tue 1/05 1100-1120ET: Tsy 20Y-30Y, appr $1.750B

- Wed 1/06 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

- Thu 1/07 1100-1120ET: Tsy 20Y-30Y, appr $1.750B

- Fri 1/08 1100-1120ET: Tsy 0Y-2.25Y, appr $12.825B

PIPELINE

2021 Starts off with a surge in high-grade debt issuance: $27.5B

- Date $MM Issuer (Priced *, Launch #)

- 01/04 $10B #Broadcom $750M 7Y +135, $2.75B 10Y +155, $1.75B 12Y +170, $3B 20Y +185, $1.75B 30Y +210 (last year May 5, AVGO issued $8B: $1B 3Y +200, $2.25B 5Y +280, $2.75B 10Y +350, $2B 12Y +365)

- 01/04 $3B #Mexico 50Y 3.75%

- 01/04 $3B #Toronto Dominion (TD) $1.15B 2Y +18, $600M 2Y FRN SOFR+24, $1.25B 5Y +43

- 01/04 $3B #Home Depot $500M 7Y +35, $1.25B 10Y +52, $1.25B 30Y +77 (last year, Mar 26, HD issued $5B: $750M 7Y+190, $1.5B 10Y+195, $1.25B 20Y+195, $1.5B 30Y+200)

- 01/04 $2.5B #Sumitomo Mitsui Fncl Grp (SMFG) $500M 3Y +35, $1B 5Y +60, $500M 10Y +80, $500M 20Y +85

- 01/04 $2B #Metropolitan Life $625M 3Y +25, $625M 3Y FRN SOFR+32, $750M 10Y +68

- 01/04 $1.5B #John Deere 5Y +37, 10Y +57

- 01/04 $1.5B #Athene Global Funding $750M 3Y +80, $250M 3Y FRN L+73, $500M 5Y +110a

- 01/04 $1B *Exp/Imp Bank of India 10Y +145

- On tap for Tuesday:

- 01/05 $1B European Inv Bank (EIB) 5Y +7

FOREX

The Greenback was a beneficiary as virus fears hit global sentiment and risk was trimmed. Global indices remained heavy throughout the US morning and the Dollar Index reversed all prior losses to briefly turn positive on the day. * EURUSD after trading with a bid tone all morning, marginally failed to make a new recent high at 1.2309 and finally gave in to the equities weakness, trading back down to 1.2255 amid the USD demand. USDJPY remained stable and flat on the session as haven flows into both currencies limited the pair's range.

- GBP came under heavy pressure as UK's Johnson announced he will address the nation later today to announce further restrictions. As the case count continues to mount, the BBC have reported he is likely to announce a lockdown similar to measures imposed in March. Cable is down 0.85% having briefly tested above the 1.37 handle earlier in the day. EURGBP has seen a larger move and is currently up 1.2% at 0.9045.

- AUD(-0.53%), NZD(-0.42%) and CAD(-0.46%) all saw outflows as Equities traded lower, having previously traded higher following positive sentiment during Asia and European sessions.

- A sharp move lower in WTI Crude futures (Down 2%) translated into a turnaround in currencies such as USDBRL (+1.31%), with EURNOK and USDRUB reversing and both ending towards their best levels.

EGBs-GILTS CASH CLOSE: Strong But Shaky Start To 2021

After a sharp rally on the Gilt open, core Europe FI spent most of the rest of the session fading before rallying anew mid-afternoon.

- The catalyst for the late-day rebound was news of a nationwide England lockdown announcement set to be announced by UK PM Johnson at 2000GMT (following Scotland's decision to do the same). Equities fell to session lows while GBP weakened.

- The early FI bid was helped by weaker-than-expected Italy/Spain Dec PMIs.

- Lots of syndications announced: Ireland and Slovenia 10-Yr, Italy 15-Yr, plus Slovenia 2050 Tap.

- ECB's Lane speaks at 2045GMT. France flash CPI early Tues. Closing Levels / 10-Yr Periphery EGB Spreads:

- Germany: The 2-Yr yield is down 2.2bps at -0.722%, 5-Yr is down 2.4bps at -0.762%, 10-Yr is down 3.5bps at -0.604%, and 30-Yr is down 3.8bps at -0.196%.

- UK: The 2-Yr yield is up 0.7bps at -0.153%, 5-Yr is down 1.8bps at -0.103%, 10-Yr is down 2.4bps at 0.173%, and 30-Yr is down 2bps at 0.73%.

- Italian BTP spread up 4bps at 115.2bps / Spanish up 1.1bps at 62.7bps.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.