Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI BRIEF: Fed's Favored Inflation Expect Index Near 7yr High

- MNI BRIEF: Fed Finds Central Treasury Clearing Efficient

- MNI POLICY: U.S. Currency Report Drops 'Manipulator' Label

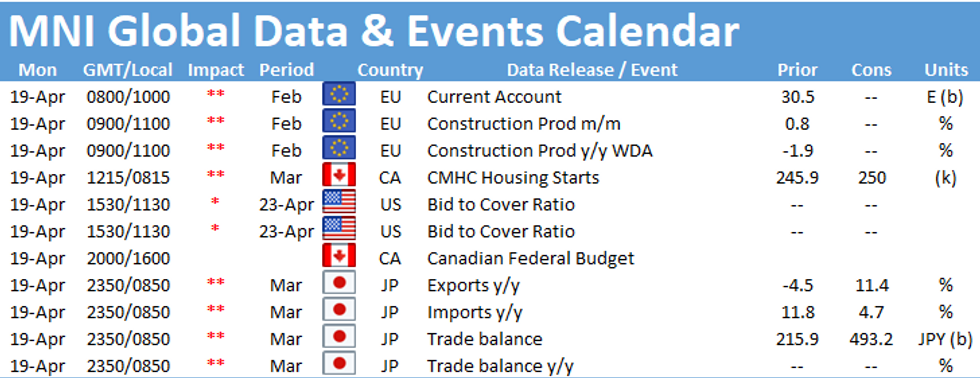

- MNI PREVIEW: Canada Budget May Extend Unanchored Deficits

US TSY SUMMARY: Risk-On Even Before Strong Housing Data

Weaker across the curve all session, Tsy futures holding near middle session range, yield curves see-sawed to flatter levels after the close, equities new highs (ESM1 4180.)- Risk-on after strong data: housing starts (1.457M) and permissions (1.720M) both beat expectations, with Tsy futures making new lows, 10YY tapped 1.5957% high vs. 1.5728% currently. Sources noted real$ and fast$ sold 5s and 10s early on, bank selling 30s, prop 2-way in 5s.

- Moderate two-way positioning ensued as accts looked to square up ahead weekend and lack of data until Thursday next week, Fed enters media blackout at midnight through April 29.

- Large $15B Bank of America 6pt jumbo debt issuance launched late, rounding out heavy week of issuance from GSIBs ($13B JPM, $6B GS, $8B World Bank, $4.25B IADB, $2.25B BNP Paribas).

- No react to to Fed Gov Waller comments "FED'S DOT PLOT OF FORECASTS ON RATES ISN'T HELPING US" Bbg mirrored Fed Chair on Wed: mkt places too much importance on dot-plot, stresses outcomes / goals need to be met: labor market recovery, inflation stable at 2% (not temporary), moving above 2%.

- The 2-Yr yield is up 0.2bps at 0.1612%, 5-Yr is up 0bps at 0.8178%, 10-Yr is down 0.7bps at 1.5693%, and 30-Yr is down 1bps at 2.2595%.

US

FED: One of the Fed's preferred gauges for inflation expectations has edged above 2%, fresh data release Friday showed, hitting the highest level since December 2014.

- The Index of Common Inflation Expectations was updated with data through March and shows that inflation expectations came in at 2.01%, after falling to 1.93% in March 2020 and steadily drifting lower since the financial crisis. The CIE index combines 21 market and survey measures into a single view of how households and businesses expect prices to behave.

- Outlining the CIE's relevance, Fed Vice Chair Richard Clarida said Wednesday at a Manhattan Institute event if the index of expectations were to "drift up persistently" or fall considerably below 2%, "that would indicate to me that policy would need to be adjusted." He added that the Fed's "metric of success" on the central bank's new long-term framework is keeping expectations about future price increases anchored at 2%.

- Settlement fails would also have been lower if trades were centrally cleared, the authors said. The estimated benefits would likely be even greater if dealers' auction purchases were included in the analysis, or if the increased central clearing included repo transactions.

- MNI has reported that the Fed is pushing for wider clearing of Treasuries to help dealers provide liquidity during market volatility.

TSY: The U.S. Treasury said Friday Taiwan, Switzerland, and Vietnam may be manipulating their currency, but there's insufficient evidence to formally label the countries currency manipulators.

- In its semi-annual currency manipulation report, the Treasury said over the four quarters through December 2020, five major U.S. trading partners -- Vietnam, Switzerland, Taiwan, India, and Singapore -- intervened in the foreign exchange market in a sustained, asymmetric manner with the effect of weakening their currencies. For more see MNI Policy main wire at 0900ET.

- KAPLAN: CLIMATE CHANGE HAS SIGNIFICANT EFFECT ON ECONOMY, Bbg

- KAPLAN: CLIMATE CHANGE HAS BIG FINL STABILITY CONSIDERATIONS, Bbg

- KAPLAN: CLIMATE CHANGE IS EXAMPLE OF TAIL RISK FOR BUSINESSES. Bbg

CANADA

CANADA: Canada's longest ever spell without a budget ends Monday with Finance Minister Chrystia Freeland likely maintaining record deficits absent a strong "fiscal anchor" and arguing the economy still needs unbridled assistance.

- The deficit for the fiscal year that began April 1 could come in at CAD160 billion on expanded pandemic and social spending programs, according to RBC economists, larger than Freeland's Nov. 30 estimate of CAD121 billion. The previous year's shortfall will be in line with the government's estimate of CAD382 billion according to RBC. That would be 17.5% of GDP, seven times the cash record of CAD56 billion set in 2009-10 and approaching the record 22.5% of GDP set in World War II.

OVERNIGHT DATA

- US MAR HOUSING STARTS 1.739M; PERMITS 1.766M

- US FEB STARTS REVISED TO 1.457M; PERMITS 1.720M

- US MAR HOUSING COMPLETIONS 1.580M; FEB 1.355M (REV)

- MICHIGAN PRELIM. APRIL CONSUMER SENTIMENT AT 86.5; EST. 89

- MICHIGAN 1-YR INFLATION EXPECTATIONS AT 3.7% AFTER 3.1%, (9 year highs)

- University of Michigan Mid-Apr Current Index 97.2

- FOREIGN HOLDINGS OF CANADA SECURITIES +8.5B CAD IN FEB

- CANADIAN HOLDINGS OF FOREIGN SECURITIES +10.5B CAD IN FEB

MARKETS SNAPSHOT

Key late session market levels

- DJIA up 180.96 points (0.53%) at 34216.69

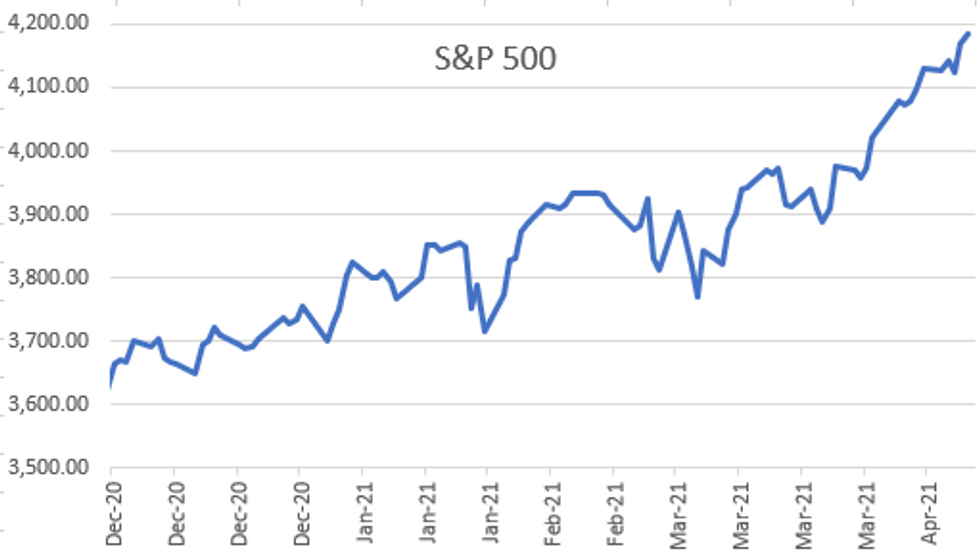

- S&P E-Mini Future up 16 points (0.38%) at 4178.25

- Nasdaq up 10.3 points (0.1%) at 14049.16

- US 10-Yr yield is down 0.7 bps at 1.5693%

- US Jun 10Y are down 8/32 at 132-13

- EURUSD up 0.0012 (0.1%) at 1.1979

- USDJPY up 0.02 (0.02%) at 108.78

- WTI Crude Oil (front-month) down $0.32 (-0.5%) at $63.13

- Gold is up $14.07 (0.8%) at $1777.90

European bourses closing levels:

- EuroStoxx 50 up 39.56 points (0.99%) at 4032.99

- FTSE 100 up 36.03 points (0.52%) at 7019.53

- German DAX up 204.42 points (1.34%) at 15459.75

- French CAC 40 up 52.93 points (0.85%) at 6287.07

US TSY FUTURES CLOSE

- 3M10Y -0.162, 155.405 (L: 153.216 / H: 158.05)

- 2Y10Y -0.886, 140.407 (L: 138.874 / H: 143.053)

- 2Y30Y -1.278, 209.359 (L: 207.18 / H: 211.912)

- 5Y30Y -1.233, 143.776 (L: 142.316 / H: 145.858)

- Current futures levels:

- Jun 2Y down 0.5/32 at 110-11.625 (L: 110-11.25 / H: 110-12)

- Jun 5Y down 5/32 at 123-30.75 (L: 123-28 / H: 124-01)

- Jun 10Y down 9/32 at 132-12 (L: 132-06.5 / H: 132-17.5)

- Jun 30Y down 1-0/32 at 158-0 (L: 157-16 / H: 158-15)

- Jun Ultra 30Y down 1-24/32 at 187-19 (L: 186-19 / H: 188-15)

US EURODOLLAR FUTURES CLOSE

- Jun 21 -0.005 at 99.810

- Sep 21 -0.005 at 99.805

- Dec 21 -0.005 at 99.740

- Mar 22 -0.005 at 99.775

- Red Pack (Jun 22-Mar 23) -0.02 to -0.005

- Green Pack (Jun 23-Mar 24) -0.035 to -0.02

- Blue Pack (Jun 24-Mar 25) -0.045 to -0.04

- Gold Pack (Jun 25-Mar 26) -0.04 to -0.035

Short Term Rates

US DOLLAR LIBOR: Latest settles

- O/N -0.00050 at 0.07275% (-0.00200/wk)

- 1 Month +0.00088 to 0.11588% (+0.00463/wk)

- 3 Month -0.00150 to 0.18825% (+0.00075/wk) (Record Low of 0.17525% on 2/19/21)

- 6 Month +0.00600 to 0.22363% (+0.01325/wk)

- 1 Year +0.00463 to 0.29238% (+0.00663/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $66B

- Daily Overnight Bank Funding Rate: 0.06%, volume: $242B

- Secured Overnight Financing Rate (SOFR): 0.01%, $928B

- Broad General Collateral Rate (BGCR): 0.01%, $384B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $359B

- (rate, volume levels reflect prior session)

- TIPS 7.5Y-30Y, appr $1.199B accepted vs. $1.770B submission

- Next scheduled purchases:

- Mon 4/19 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.825B

- Tue 4/20 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Wed 4/21 1010-1030ET: Tsy 4.5Y-7Y, appr $6.025B

- Thu 4/22 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 4/23 1010-1030ET: TIPS 1Y-7.5Y, appr $2.425B

PIPELINE: $15B Bank of America Launched, Back to 6Pts

- Date $MM Issuer (Priced *, Launch #)

- 04/16 $15B Bank of America $2.25B 4NC3 +65, $600M 4NC3 FRN SOFR+69, $3.75B 6.25NC5.25 +90, $400M 6.25NC5.25 FRN SOFR+97, $4.5B 11NC10 +110, $3.5B 21NC20 +115

- 04/15 $13B *JP Morgan $3.5B 6NCn +77, $500M 6NC5 FRN SOFR, $3.5B 11NC10 +102, $2B 21NC20 +100, $3.5B 31NC30 +107

- 04/15 $6B *Goldman Sachs $3.75B 11NC10 +105, $2.25B 21NC20 +105

- 04/13 $8B *World Bank (IBRD) $3B 2Y -5, $5B 7Y +7

- 04/13 $4.25B *IADB 5Y +0.0

- 04/12 $2.25B *BNP Paribas 11NC10 +120

FOREX: AUD, NZD Reverse Winning Streak

- Antipodean currencies snapped an extended winning streak Friday, prompting NZD and AUD to underperform all others into the Friday close. NZD/USD returned below the 50- and 100-dmas, but still managed to hold decent weekly gains.

- Markets largely shrugged off the release of the US Treasury's FX report, despite the US noting that Switzerland, Taiwan and Vietnam all met the criteria to be tagged as an FX manipulator. The SNB responded by reaffirming their commitment to CHF intervention to ensure domestic price stability. The CHF was among the session's best performers, alongside CAD.

- The USD index continues to oscillate either side of the 50-dma, with the trajectory of US yields still a key driver. The Treasury curve flattened modestly Friday, helping keep a lid on the greenback.

- Focus in the coming week turns to the ECB rate decision, a slew of UK data including inflation and jobs numbers as well as the prelim April global PMIs. Rates decisions from the Canadian, Indonesian and Russian central banks also cross.

EGB/Gilt Summary: Ending The Week On A Soft Note

European government bonds have broadly traded sideways through the day and have failed to claw back the losses posted earlier in the session.

- The gilt curve has bear steepened with the 2s30s spread 3bp wider.

- Bund yields are now 1-2bp higher with the curve 1bp steeper.

- OATs similarly remain a touch weaker on the day. Last yields: 2-year -0.6636%, 5-year -0.5609%, 10-year -0.0199%, 30-year 0.8313%.

- BTPs trade in line with core EGBs, with the longer end of the curve slightly underperforming.

- The UK and EU today pledged to work together in calming tensions in Northern Ireland following the recent spate of rioting.

- Focus next week will be the ECB Governing Council meeting on Thursday and any additional clarity on the roll out of the Johnson & Johnson Covid vaccine.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.