Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- EXXON and JP Morgan planning on re-staffing offices in May and July respectively

- TWO NEW CLOTTING CASES AFTER J&J SHOTS BEING INVESTIGATED: CDC

- CDC ISSUES NEW MASKING GUIDELINES FOR FULLY VACCINATED PEOPLE: Says people can forgo wearing masks at some indoor settings and outdoor exercise.

FOMC PREVIEWS

BofA Preview: Strong Data, But More Progress Needed BofA sees the focus at the April FOMC on the language in the statement and in Powell's presser. Powell and the FOMC "to give a more positive view of the economy but reiterate that the economy needs to make further progress before signalling any policy change and risks remain from the virus."

- Statement: Changes to the assessment of the economy to reflect better growth data in COVID sensitive sectors while emphasizing the improvement is just beginning, and mentioning the recent but likely transitory strength in inflation.

- Press conference: BofA looking to see if Powell reiterates "some time" before "substantial further progress" or changes the description of the path. BofA: "We believe 'some time' is still appropriate, but there is a risk that he shifts".

- Powell likely to explain difference between desired output level vs growth rate (esp on jobs).

- Robust discussion on the concern over shortages (both labor and for supply chain) – Powell to note these are temporary challenges and that capacity will return.

- Future action: Powell may signal that discussions on defining "substantial further progress" planned at the June FOMC. EFFR to have to drop to at least 0.06% before the Fed acts; odds of an IOER / RRP tweak at this meeting just 15-25%.

- "A hawkish surprise would be if the Fed acknowledged progress more prominently, paving the way to an advance warning of tapering asset purchases."

- Statement: To reflect a cautiously more optimistic outlook.

- Press conference: Powell to reiterate that the FOMC awaits more evidence that rehiring is continuing.

- Future action: More formal guidance "well ahead" of tapering may emerge at/before the June FOMC.

- Technical changes to IOER / ON RRP possible at this meeting, but base case is delay.

NatWest Preview: Routine Updating Of The Statement. NatWest expects little new from the April FOMC, apart from a possible tweak in the Statement language.

- Statement: If the FOMC wants to make modest changes, they could make the description of current economic conditions slightly more positive than in March, consistent with recent data (e.g. changing "Following a moderation in the pace of the recovery, indicators of economic activity and employment have turned up recently" by adding "sharply").

- Could reword the reference to inflation by acknowledging a temporary move above 2% in inflation in 2021.

- Seems premature to remove the reference that the pandemic "poses considerable risks".

- Press conference: Powell to reiterate comments in his recent 60 Minutes interview when he said the economy was at an "inflection point" with stronger growth and hiring ahead.

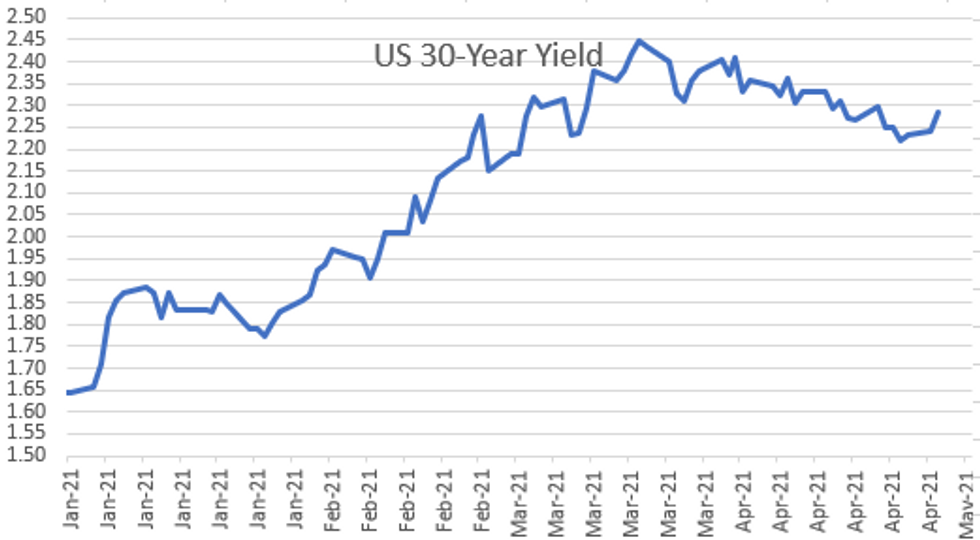

US TSY SUMMARY: Tsy Ylds Jump in Lead-Up To FOMC

Treasury futures under pressure all day saw bonds extend session lows through the second half, while recovering slightly after some chunky Block buys in 5s and 10s.

Mixed data, housing robust as consumer confidence climbs to 121.7 from 109.0 prior while Richmond Fed factory index held steady to prior moth at 17.0 -- well off 22.0 estimate. Focus on Wed's FOMC rate annc.

- Bonds lead midday sell-off, trading desks cited auction set-ups ahead the $62B 7Y auction, rollers in 2s and 5s, fast$ selling 7s. Otherwise rather quiet on the headline front (lull ahead Wed's FOMC, heavy earning slate next week and NFP next week Fri (current median est +900k), though EXXON and JPM planning on re-staffing offices in May and July respectively provides some positive news.

- Decent $62B 7Y Tsy-note auction (1.306% high yld vs. 1.305% WI). 30YY currently 1.2743% highs -- back near last week Wednesday's highs. Trade volumes rather sedate, however, participants migrating to sidelines ahead Wed's FOMC policy annc.

- Desks posited large 11k FVM1 Block buy at 123-26.5 (through the 123-26.25 offer at time) may have been first half of legged of steepener as 30Y bonds continue to grind lower. 30YY currently 2.2942% -- puts it back to middle of last week Tue's level; 5YY 0.8829 high puts it back to April 13 mid-session.

- The 2-Yr yield is up 1.2bps at 0.1798%, 5-Yr is up 5.2bps at 0.8813%, 10-Yr is up 5.7bps at 1.6234%, and 30-Yr is up 5.3bps at 2.2927%.

OVERNIGHT DATA

- U.S. APRIL CONSUMER CONFIDENCE INDEX RISES TO 121.7 FROM 109.0

- U.S. APRIL RICHMOND FED FACTORY INDEX AT 17 (flat to last month, well off 22.0 estimate)

- US FEB FHFA HPI SA +0.9% V +1.0% JAN; +12.2% Y/Y

- US FEB CASE-SHILLER SEAS ADJ HOME PRICE INDEX +1.2% M/M

- US FEB CASE-SHILLER UNADJ HOME INDEX +1.2% M/M; +11.9% Y/Y

- US FEB CASE-SHILLER NATIONAL IDX +1.1% SA, +1.1% NSA, +12% Y/Y

- US REDBOOK: APR STORE SALES +13.5% V YR AGO MO

- US REDBOOK: STORE SALES +13.9% WK ENDED APR 24 V YR AGO WK

- US REDBOOK: WILL RESUME MONTH-TO-MONTH DATA COMPARISON IN FEB 2022

MARKETS SNAPSHOT

Key late session market levels

- DJIA up 42.42 points (0.12%) at 34020.7

- S&P E-Mini Future up 3 points (0.07%) at 4181.75

- Nasdaq down 42.6 points (-0.3%) at 14097.16

- US 10-Yr yield is up 5 bps at 1.6163%

- US Jun 10Y are down 10.5/32 at 132-1.5

- EURUSD up 0.0002 (0.02%) at 1.2088

- USDJPY up 0.64 (0.59%) at 108.72

- WTI Crude Oil (front-month) up $1.29 (2.08%) at $63.05

- Gold is down $3.79 (-0.21%) at $1777.17

European bourses closing levels:

- EuroStoxx 50 down 8.92 points (-0.22%) at 4011.91

- FTSE 100 down 18.15 points (-0.26%) at 6944.97

- German DAX down 47.07 points (-0.31%) at 15249.27

- French CAC 40 down 1.76 points (-0.03%) at 6273.76

MONTH-END EXTENSION ESTS: Preliminary Barclays/Bbg Extension Estimates for US

Forecast summary compared to the avg increase for prior year and the same time in 2020. TIPS 0.16Y; Govt inflation-linked, 0.17. Note broad decline in Govt/Credit and Intermediate credit from year ago levels, while MBS extension est surges.

| Estimate | 1Y Avg Incr | Last Year | |

| US Tsys | 0.09 | 0.08 | 0.13 |

| Agencies | 0.06 | 0.04 | 0.03 |

| Credit | 0.07 | 0.1 | 0.2 |

| Govt/Credit | 0.08 | 0.09 | 0.17 |

| MBS | 0.25 | 0.06 | 0.05 |

| Aggregate | 0.12 | 0.08 | 0.08 |

| Long Gov/Cr | 0.05 | 0.09 | 0.06 |

| Iterm Credit | 0.08 | 0.08 | 0.2 |

| Interm Gov | 0.09 | 0.08 | 0.1 |

| Interm Gov/Cr | 0.08 | 0.08 | 0.15 |

| High Yield | 0.09 | 0.11 | 0.08 |

US TSY FUTURES CLOSE

- 3M10Y +6.004, 160.897 (L: 154.485 / H: 161.506)

- 2Y10Y +4.291, 143.988 (L: 139.263 / H: 144.539)

- 2Y30Y +4.683, 211.71 (L: 206.645 / H: 211.752)

- 5Y30Y +0.872, 141.762 (L: 139.042 / H: 141.762)

- Current futures levels:

- Jun 2Y down 0.5/32 at 110-11.125 (L: 110-11 / H: 110-11.75)

- Jun 5Y down 4.5/32 at 123-26 (L: 123-25 / H: 123-31)

- Jun 10Y down 11.5/32 at 132-0.5 (L: 131-30.5 / H: 132-12.5)

- Jun 30Y down 1-2/32 at 157-12 (L: 157-10 / H: 158-16)

- Jun Ultra 30Y down 2-1/32 at 185-28 (L: 185-28 / H: 187-31)

US EURODOLLAR FUTURES CLOSE

- Jun 21 -0.005 at 99.810

- Sep 21 -0.005 at 99.795

- Dec 21 -0.005 at 99.735

- Mar 22 -0.005 at 99.765

- Red Pack (Jun 22-Mar 23) -0.02 to -0.005

- Green Pack (Jun 23-Mar 24) -0.045 to -0.025

- Blue Pack (Jun 24-Mar 25) -0.06 to -0.05

- Gold Pack (Jun 25-Mar 26) -0.075 to -0.065

Short Term Rates

US DOLLAR LIBOR: Latest settles

- O/N +0.00025 at 0.07400% (+0.00062/wk)

- 1 Month -0.00075 to 0.11025% (-0.00075/wk)

- 3 Month -0.00687 to 0.17713% (-0.00425/wk) ** (New Record Low 0.17288% on 4/22/21)

- 6 Month +0.01237 to 0.21425% (+0.01012/wk)

- 1 Year +0.00063 to 0.28263% (+0.00175/wk)

- Daily Effective Fed Funds Rate: 0.07% volume: $72B

- Daily Overnight Bank Funding Rate: 0.06%, volume: $276B

- Secured Overnight Financing Rate (SOFR): 0.01%, $875B

- Broad General Collateral Rate (BGCR): 0.01%, $369B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $350B

- (rate, volume levels reflect prior session)

- No buy operations Tuesday and Wednesday, Pause for FOMC

- Next scheduled purchases:

- Thu 4/29 1010-1030ET: Tsy 20Y-30Y, appr $1.750B

- Fri 4/30 1100-1120ET: Tsy 0Y-2.25Y, appr $12.825B

PIPELINE: $3.5B Italy 2Pt Priced

- Date $MM Issuer (Priced *, Launch #)

- 04/27 $5.5B #Citigroup $2B 4NC3 +63, $500M 4NC3 FRN SOFR, $3B 11NC10 +95 (adds to $2.5B issued mid-Jan; compares to $3.5B 6NC5 +275 issued early April 2020)

- 04/27 $3.5B *Italy $2B 3Y +50, $1.5B 30Y +195; $2B 3Y: re-offer price of 99.673%, equivalent to a 0.986% gross annual yld in US$; $1.5B 30Y: re-offer price of 98.897%, equivalent to a 3.938% gross annual yld in US$

- 04/27 $Benchmark Hyundai Motor Indonesia 5Y +135a

- 04/27 $Benchmark Development Bank of Kazakhstan 10Y investor calls

FOREX: USD/JPY Bounces Further Off Friday Low

- Despite flatlining equity markets, JPY edged back into a negative territory Tuesday, with USD/JPY picking up some upside momentum after the London close. This extends the bounce from Friday's lows to well over 100 pips, with the pair nearing in on the 38.2% retracement of the April downtick. JPY was comfortably the poorest performer in G10.

- The greenback held its ground after stabilising on Monday. The USD Index now trades either side of the 100-dma at 91.05 and will need to build a base above here to stage any broader recovery.

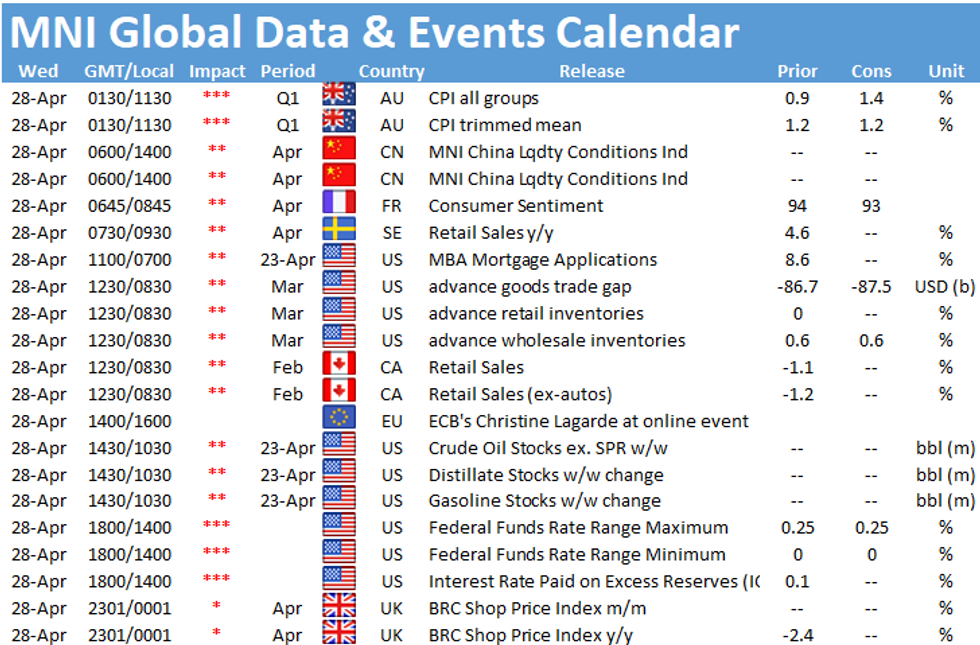

- Focus Wednesday rests on the FOMC. Their April decision is not seen as a major factor for markets at this juncture, with the board expected to stay the course on policy and steer clear of any discussion over the tapering of asset purchases.

- Data due Wednesday includes Australian CPI for Q1, Canadian retail sales and US trade balance data for March. Central bank speakers include ECB's Lagarde, Rehn and Schnabel as well as Fed Chair Powell's post-decision presser.

EGBs-GILTS CASH CLOSE: BTPs Widen On Issuance

Gilts underperformed with a parallel shift in the curve Tuesday, while Bunds were basically unchanged. Periphery spreads drifted wider.

- BTPs led the periphery widening (and the session's price action), amid today's auctions of short-term/linkers and dual-tranche USD issuance syndication, and ahead of auctions tomorrow of up to E7.25bln of BTPs / E1.25bln of CCTeu.

- 10-Yr BTP yields fell just short of 2021 peak of 0.842% (day's high was 0.832%).

- UK sold E6bn of 30-Yr Gilt via syndication. EIB announced a mandate for a E100mn digital bond based on the Ethereum blockchain.

- Otherwise most attention is on the US Fed decision Wednesday.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is up 0.1bps at -0.688%, 5-Yr is up 0.1bps at -0.599%, 10-Yr is up 0.4bps at -0.249%, and 30-Yr is up 0.4bps at 0.292%.

- UK: The 2-Yr yield is up 1.4bps at 0.065%, 5-Yr is up 1.7bps at 0.344%, 10-Yr is up 1.8bps at 0.774%, and 30-Yr is up 1.8bps at 1.301%.

- Italian BTP spread up 1.8bps at 107bps / Spanish spread up 1.1bps at 66.5bps

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.