Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Fed's New Framework Tested By Inflation Surge

- FED VC QUARLES: FED WILL WAIT TO SEE JOB MARKET DATA BEFORE ACTING, Bbg

SF Fed Daly interview on CNBC:

- DALY SAYS WE ARE TALKING ABOUT TALKING ABOUT TAPERING, Bbg

- In regards to productivity and employment gains:

- WE NEED TO BE PATIENT ... WE HAVEN'T SEEN SUBSTANTIAL FURTHER PROGRESS JUST YET, Bbg

US

FED: The Federal Reserve is facing tough questions about the viability of its new outcome-based approach to monetary policy less than a year after announcing the shift -- and before the new framework gets properly implemented, top former policymakers told MNI.

- "Over the last six months to a year the strategy looks less and less credible, " said Charles Plosser, ex-president of the Philadelphia Fed. "It looks and less and less believable that they're not going to change their minds." For more see MNI Policy main wire at 0922ET.

US TSY SUMMARY

Rates and equities reverted back to negative correlation for the day, rates near highs after the bell (bonds lead, curves bull flattening) while equities pared early gains/traded weaker in the second half (eminis -6.0 after rates close).

- Modest support after flurry of housing data (new home sales decline 5.9%/Apr), consumer confidence (117.2 for May vs 117.5 in Apr). Fed speakers

Clarida at crypto conf: (PUTTING A LOT OF WEIGHT ON INFLATION EXPECTATIONS" Bbg, adding "MAY COME A TIME AT UPCOMING

MEETINGS TO TALK TAPER." - Strong $60B 2Y note (91282CCD1) auction trades through with high yield of 0.152% vs. 0.160% WI, strongest in over a year. Tsy futures gain slightly, extend duration..

- Bid-to-cover 2.74x, highest since Aug '20, compares to 2.49x 5 month average.

- Indirects take-up climbs to 57.06% vs. 43.35% in April; direct bidder take-up at 18.03% vs. 18.42% last month, primary dealer take-up of 24.91% well below 5-month average of 32.15%.

- Heavy Jun/Sep quarterly Tsy futures roll volume near 7M ahead Friday's first notice when Sep takes lead contract. Roll appr 60% complete after the bell.

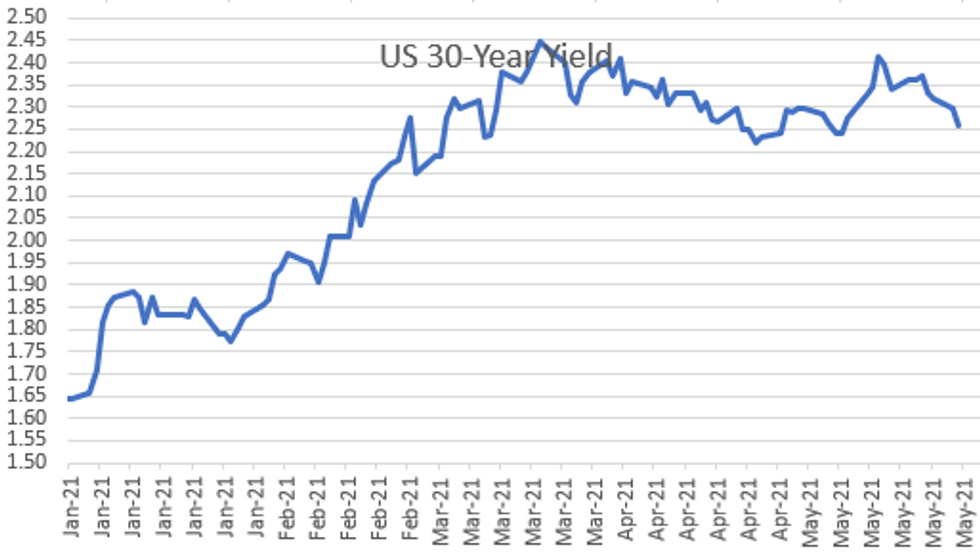

- The 2-Yr yield is down 0.6bps at 0.1433%, 5-Yr is down 3.2bps at 0.771%, 10-Yr is down 4.1bps at 1.5604%, and 30-Yr is down 4.3bps at 2.2562%.

OVERNIGHT DATA

- US MAY PHILADELPHIA FED NONMFG INDEX 36.9

- US MAR CASE-SHILLER SEAS ADJ HOME PRICE INDEX +1.6% M/M

- US MAR CASE-SHILLER UNADJ HOME INDEX +2.2% M/M; +13.3% Y/Y

- US MAR CASE-SHILLER NATIONAL IDX +1.5% SA, +2% NSA, +13.2% Y/Y

- US MAR FHFA HPI SA +1.4% V +1.1% FEB; +13.9% Y/Y

- US Q1 FHFA HPI Q/Q SA +3.5% V +12.6% Q1 2020

- US REDBOOK: MAY STORE SALES +13.2% V YR AGO MO

- US REDBOOK: STORE SALES +13.6% WK ENDED MAY 22 V YR AGO WK

- US REDBOOK: WILL RESUME MONTH-TO-MONTH DATA COMPARISON IN FEB 2022

- US CONF BOARD CONSUMER CONFIDENCE 117.2 IN MAY V APR 117.5

- US APR NEW HOME SALES -5.9% TO 0.863M SAAR

- US MAR NEW HOME SALES REVISED TO 0.917M SAAR

- FED: 48 COUNTERPARTIES TAKE $432.9B AT FIXED-RATE REVERSE REPO

- CANADIAN APRIL FLASH FACTORY SALES -1.1%

MONTH-END EXTENSIONS/PRELIM: Barclays/Bbg Extension Estimates for US

Preliminary forecast summary compared to avg increase for prior year and same time in 2020. TIPS 0.02Y. Note: fairly steady to year ago levels, while MBS extension est gains.

| Indices | Estimate | 1Y Avg Incr | Last Year |

| US Tsys | 0.12 | 0.08 | 0.11 |

| Agencies | 0.04 | 0.11 | 0.01 |

| Credit | 0.10 | 0.08 | 0.08 |

| Govt/Credit | 0.10 | 0.08 | 0.10 |

| MBS | 0.13 | 0.06 | 0.05 |

| Aggregate | 0.11 | 0.08 | 0.09 |

| Long Gov/Cr | 0.10 | 0.09 | 0.10 |

| Iterm Credit | 0.08 | 0.07 | 0.08 |

| Interm Gov | 0.09 | 0.08 | 0.08 |

| Interm Gov | 0.09 | 0.08 | 0.08 |

| High Yield | 0.1 | 0.06 | 0.04 |

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 79.44 points (-0.23%) at 34312.83

- S&P E-Mini Future down 12.25 points (-0.29%) at 4182.25

- Nasdaq down 23.6 points (-0.2%) at 13639.01

- US 10-Yr yield is down 3.9 bps at 1.5621%

- US Jun 10Y are up 11/32 at 132-31

- EURUSD up 0.0037 (0.3%) at 1.2253

- USDJPY down 0.04 (-0.04%) at 108.71

- WTI Crude Oil (front-month) down $0.15 (-0.23%) at $65.91

- EuroStoxx 50 up 0.46 points (0.01%) at 4036.04

- FTSE 100 down 21.8 points (-0.31%) at 7029.79

- German DAX up 27.58 points (0.18%) at 15465.09

- French CAC 40 down 18.22 points (-0.28%) at 6390.27

US TSY FUTURES CLOSE:

- 3M10Y -4.494, 154.608 (L: 154.523 / H: 159.022)

- 2Y10Y -3.434, 141.347 (L: 141.313 / H: 145.461)

- 2Y30Y -3.684, 210.946 (L: 210.875 / H: 215.06)

- 5Y30Y -1.253, 148.21 (L: 148.015 / H: 149.75)

- Current futures levels:

- Jun 2Y up 0.5/32 at 110-13.75 (L: 110-13.125 / H: 110-13.875)

- Jun 5Y up 5.25/32 at 124-14.5 (L: 124-09 / H: 124-14.75)

- Jun 10Y up 11.5/32 at 132-31.5 (L: 132-19 / H: 132-31.5)

- Jun 30Y up 30/32 at 158-20 (L: 157-21 / H: 158-20)

- Jun Ultra 30Y up 1-17/32 at 187-17 (L: 185-27 / H: 187-17)

US EURODOLLAR FUTURES CLOSE

- Jun 21 +0.0025 at 99.865

- Sep 21 +0.005 at 99.860

- Dec 21 steady at 99.810

- Mar 22 +0.005 at 99.830

- Red Pack (Jun 22-Mar 23) +0.010 to +0.030

- Green Pack (Jun 23-Mar 24) +0.035 to +0.050

- Blue Pack (Jun 24-Mar 25) +0.060 to +0.065

- Gold Pack (Jun 25-Mar 26) +0.065

Short Term Rates

US DOLLAR LIBOR: Latest Settles

- O/N +0.00138 at 0.06063% (+0.00088/wk)

- 1 Month -0.00100 to 0.09000% (-0.00163/wk)

- 3 Month -0.00238 to 0.13850% (-0.00850/wk) ** (Record Low)

- 6 Month +0.00012 to 0.17675% (-0.00200/wk)

- 1 Year -0.00225 to 0.25600% (-0.00363/wk)

- Daily Effective Fed Funds Rate: 0.06% volume: $64B

- Daily Overnight Bank Funding Rate: 0.05% volume: $265B

- Secured Overnight Financing Rate (SOFR): 0.01%, $858B

- Broad General Collateral Rate (BGCR): 0.01%, $372B

- Tri-Party General Collateral Rate (TGCR): 0.01%, $350B

- (rate, volume levels reflect prior session)

- Tsys 10Y-22.5Y, $1.401B accepted vs. $5.084B submission

- Next scheduled purchases:

- Wed 5/26 1010-1030ET: Tsy 2.25Y-4.5Y, appr $8.425B

- Thu 5/27 1010-1030ET: Tsy 22.5Y-30Y, appr $2.025B

- Fri 5/28 1010-1030ET: Tsy 0Y-2.25Y, appr $12.425B

PIPELINE: Get While the Getting's Good, $7B AstraZeneca Launches

AstraZeneca launches $7B over six tranches, drops the 3Y FRN. Chatter had been the pharmaceutical would issue two tranches over 30Y. No investor interest there.

- Date $MM Issuer (Priced *, Launch #)

- 05/25 $7B #AstraZeneca 7pt jumbo: $1.4B 2Y +20, $1.6B 3NC1 +40, $1.25B 5Y +45, $1.25B 7Y +55, $750M 10Y +70, $750M 30Y +80. For comparison: AZN issued $3B last year Aug 3: $1.2B +5Y +55, $1.3B 10Y +85, $500M 30Y +100.

- 05/25 $2.75B Westpac $1.45B 5Y +40, $300M 5Y FRN SOFR+52, $1B 10Y +60

- 05/25 $2.5B #Deutsche Bank $1B 3Y +60, $1.5B 11NC10 +148

- 05/25 $2.3B #Hormel $950M 3NC1 +35, $750M 7Y +52, $600M 30Y +82

- 05/25 $2B *Emirate of Abu Dhabi 7Y +45

- 05/25 $500M *JAB Holdings 30Y +150

- 05/25 $Benchmark AAC Tech 5Y +185a, 10Y +225s

EGBs-GILTS CASH CLOSE: Villeroy Comments Help Underpin Afternoon Gains

Bunds and Gilts bull flattened Tuesday with periphery spreads compressing sharply. Gains were posted mainly in the afternoon.

- ECB's Villeroy said ECB can be patient as inflation is low; and that the idea of reducing the pace of PEPP buys in Q3 is "purely speculative" - helping boost the space, but particularly BTPs.

- In supply, UK sold GBP4bln of Mar-39 Gilt linker via syndication - which saw record demand and the highest amount in cash terms for a linker syndication; EU tapped Apr-36 bond for E460mln; Dutch sold E1.7bln of Jan-47 DSL at auction.

- German IFO slightly beat expectations; UK public sector borrowing lower than expected.

- On Weds, Italy sells up to E4.75bln of short-term BTP and BTPei; Germany sells E2.5bln of Bund. We get French confidence data and another appearance by Villeroy.

Closing yields/10-Yr Spreads to Bunds:

- Germany: The 2-Yr yield is down 0.7bps at -0.663%, 5-Yr is down 2.3bps at -0.553%, 10-Yr is down 2.7bps at -0.167%, and 30-Yr is down 2.3bps at 0.396%.

- UK: The 2-Yr yield is down 1.6bps at 0.016%, 5-Yr is down 1.8bps at 0.321%, 10-Yr is down 2.5bps at 0.786%, and 30-Yr is down 3.9bps at 1.32%.

- Italian BTP spread down 3.8bps at 112.6bps / Spanish spread down 2.3bps at 66bps

FOREX: Greenback Regains Posture in NY Hours

- Having traded poorly for much of the morning, the USD regained some posture throughout NY hours, helping drag EUR/USD off the day's best levels of 1.2266. An appearance from Fed's Clarida may have elicited some USD buying, as he stated that there may be a time in upcoming meetings when the Fed can discuss the scaling back of asset purchases.

- The JPY traded poorly throughout, falling against most others in G10 as global equity markets made headway toward all time highs. The S&P 500 cash index traded within 25 points of the early May highs, while the Stoxx 600 in Europe hit another record level. This positive sentiment bled well into EUR/JPY which cleared resistance to trade at 133.61, the highest level since early 2018.

- SEK and NOK were the strongest currencies in G10, while JPY and GBP traded poorly.

- There are no material economic releases Wednesday, keeping focus on central bank policy for now. ECB's Villeroy, Fed's Quarles and BoC's Lane make up the speaker slate.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.