Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI: Powell Re-Designated Fed Chair Pending Confirmation

- MNI: WHITE HOUSE: Biden Speaks After Strong January Jobs Report

- Former Tsy Sec Summers: Fed Could Hike at All Seven Meetings by Yr-End .. potential for an outsize rate hike, Bbg

- ECB'S KNOT SEES RATE HIKE AS EARLY AS 4Q, Bbg

- KLAAS KNOT SEES EURO AREA INFLATION ABOVE 4% FOR MUCH OF 2022, Bbg

US

FED: Jerome Powell will become chair pro tempore of the Federal Reserve after his term expires Saturday and while he awaits a Senate confirmation vote, the Fed said Friday.

- All three Fed governors voted for the action, and Powell abstained "to avoid even the potential appearance of a conflict of interest," the Fed said.

- The Senate Banking Committee is expected to vote on Powell and four other Fed governor nominees on Feb. 15, before sending the names to the full Senate. Powell is expected to be confirmed easily.

- The Fed last appointed a chair pro tempore in 1996, when Alan Greenspan was awaiting his renomination confirmation.

- The Rescue Plan got the economy going. Bipartisan Infrastructure Plan in place for renewing bridges, roads, ports, internet.

- Federal government now buys all American made products. All components are American.

- January was a very hard month for Americans. Now America has the tools to handle Covid and get back to work.

- Need to keep wages growing. More high paying jobs.

- CEO of Intel announced USD$20 billion manufactory center. Semiconductors power everything. Nothing will function without this industry. Developing semiconductor industry will ease inflation. Automobile industry driving inflation because of semiconductor shortage.

- House of Rep just passed America COMPETES which will stimulate semiconductor industry and ease supply chain crisis.

- Capitalism without competition is not capitalism. Biden will break up monopolies which are causing inflation.

UK

BOE: May and August hikes with gilt sales beginning November, Berenberg- "We do not agree with the market's conclusion that the BoE is likely to tighten policy even faster than previously expected for the remainder of 2022."

- "The BoE's updated projections and assessing the commentary from Governor Andrew Bailey's press conference, the BoE has implicitly signalled that rates are more likely to rise at a slower pace than the market anticipated before the meeting."

- "We now look for two further 25bp hikes instead of one in 2022. We now expect the BoE to hike the Bank Rate by 25bps in both May and August to take the Bank Rate to 1% by year-end. We also bring forward our call for the BoE to start 'active' quantitative tightening via gilt sales to November 2022 from early 2023 as previously expected. We continue to project two 25bp rate hikes each year in 2023 and 2024. That would take the Bank Rate to 2.0% by end-2024, versus 1.75% previously."

US Eurodollar/Treasury Roundup: Covid Drag Overestimated

US FI markets trading broadly weaker after the bell, nice risk-on tone to the end the week with equities making new session highs late (ESH2 taps 4530.75) after trading weaker on this morning's headline Jan employment release.

- Sell-side economists overestimated knock-on effects of Covid variant on the economy while giving Wednesday's huge ADP miss (-301k) too much credit in adjusting Jan NFP forecasts lower (some called for -250k job losses).

- Friday's stellar gain of +467k jobs in Jan and up-revision totals for November and December of +709k weighed heavily on rates (and equities briefly) as markets rushed to reprice more aggressive rate hikes in 2022 and spill-over to 2023.

- Short end rates now price in appr 50% chance of 50bp liftoff in March and another 50bp go in Jun, with 150bps total hikes by year end.

- Equities traded weaker post data but recovered and traded higher into late trade. Markets will be keeping close eye on next Thu's CPI inflation metric (0.4% est vs. 0.5% in Dec) while latest earnings cycle winds down.

- Overall option volumes were not overwhelming, some continued unwinds of existing long put and put spds, some repositioning to hedge greater chance of 50bps hike in June. Implied weaker after initial gains on severity of post-data sell-off, settled in as real vol evaporated in the second half.

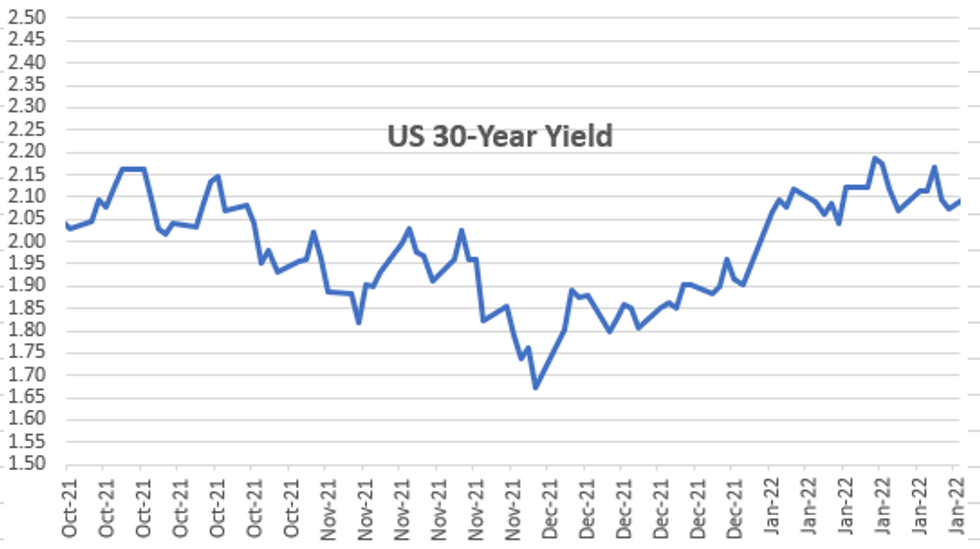

- The 2-Yr yield is up 12.2bps at 1.318%, 5-Yr is up 11.3bps at 1.7831%, 10-Yr is up 10bps at 1.9302%, and 30-Yr is up 8bps at 2.2312%.

OVERNIGHT DATA

- US JAN NONFARM PAYROLLS +467K; PRIVATE +444K, GOVT +23K

- US PRIOR MONTHS PAYROLLS REVISED: DEC +510K; NOV +647K

- US JAN AVERAGE WEEKLY HOURS 34.5 HRS

- US JAN UNEMPLOYMENT RATE 4.0%

- CANADA JAN EMPLOYMENT -200.1K; JOBLESS RATE 6.5%

- CANADA JAN FULL-TIME JOBS -82.7K; PART-TIME -117.4K

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 200.46 points (0.57%) at 35309.54

- S&P E-Mini Future up 59.75 points (1.34%) at 4528.5

- Nasdaq up 336.2 points (2.4%) at 14213.39

- US 10-Yr yield is up 10 bps at 1.9302%

- US Mar 10Y are down 27.5/32 at 126-25

- EURUSD up 0.001 (0.09%) at 1.145

- USDJPY up 0.26 (0.23%) at 115.23

- WTI Crude Oil (front-month) up $1.99 (2.2%) at $92.24

- Gold is up $1.65 (0.09%) at $1806.50

- EuroStoxx 50 down 54.44 points (-1.31%) at 4086.58

- FTSE 100 down 12.44 points (-0.17%) at 7516.4

- German DAX down 268.91 points (-1.75%) at 15099.56

- French CAC 40 down 54.25 points (-0.77%) at 6951.38

US TSYS FUTURES CLOSE

- 3M10Y +4.992, 167.261 (L: 158.662 / H: 169.796)

- 2Y10Y -4.022, 59.252 (L: 58.092 / H: 63.267)

- 2Y30Y -5.974, 89.41 (L: 87.497 / H: 95.216)

- 5Y30Y -4.114, 43.855 (L: 41.766 / H: 48.121)

- Current futures levels:

- Mar 2Y down 8.125/32 at 108-1.125 (L: 108-00.75 / H: 108-08.875)

- Mar 5Y down 20.5/32 at 118-11 (L: 118-10.25 / H: 119-00)

- Mar 10Y down 28/32 at 126-24.5 (L: 126-23.5 / H: 127-24)

- Mar 30Y down 1-21/32 at 153-08 (L: 153-02 / H: 155-13)

- Mar Ultra 30Y down 3-3/32 at 184-09 (L: 184-03 / H: 188-08)

US 10Y FUTURES TECHS: (H2) Through Bear Trigger

- RES 4: 129-31 Low Dec 8

- RES 3: 129.14 High Jan 5

- RES 2: 129-03 50-day EMA

- RES 1: 128-08+/22+ 20-day EMA / High Jan 24

- PRICE: 126-26+ @ 17:13 GMT Feb 4

- SUP 1: 126-23+ Low Feb 04

- SUP 2: 126-23 Low Jul 17, 2019 (cont)

- SUP 3: 126-17+ 1.0% 10-dma Envelope

- SUP 4: 126-10+ 61.8% retracement of the 2018 - 2020 bull cycle

Treasuries extended lower Friday, clearing the bear trigger and underpinning the bearish theme first flagged by the potential triangle formation or pennant that appeared on the daily chart. Key support at 127-02 - the Jan 19 low - has given way, confirming a resumption of the downtrend that now targets 126-23 and vol band support at 126-17+. Key resistance is unchanged at 128-27, Jan 13 high. Clearance of this hurdle would signal a short-term reversal.

US EURODOLLAR FUTURES CLOSE

- Mar 22 -0.085 at 99.395

- Jun 22 -0.135 at 98.955

- Sep 22 -0.150 at 98.645

- Dec 22 -0.160 at 98.355

- Red Pack (Mar 23-Dec 23) -0.17 to -0.14

- Green Pack (Mar 24-Dec 24) -0.14 to -0.135

- Blue Pack (Mar 25-Dec 25) -0.14 to -0.135

- Gold Pack (Mar 26-Dec 26) -0.13 to -0.11

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N -0.00143 at 0.07700% (-0.00400/wk)

- 1 Month +0.00400 to 0.11529% (+0.00900/wk)

- 3 Month +0.02400 to 0.33900% (+0.02243/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month +0.02672 to 0.55543% (+0.02100/wk)

- 1 Year +0.05514 to 0.99900% (+0.05114/wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $72B

- Daily Overnight Bank Funding Rate: 0.07% volume: $277B

- Secured Overnight Financing Rate (SOFR): 0.05%, $935B

- Broad General Collateral Rate (BGCR): 0.05%, $344B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $332B

- (rate, volume levels reflect prior session)

- No buy-operation Friday, resume next week:

- Tue 02/08 1010-1030ET: Tsy 22.5Y-30Y, appr $1.825B

- Thu 02/10 1010-1030ET: Tsy 7Y-10Y, appr $3.225B vs. $2.425B prior

FED Reverse Repo Operation

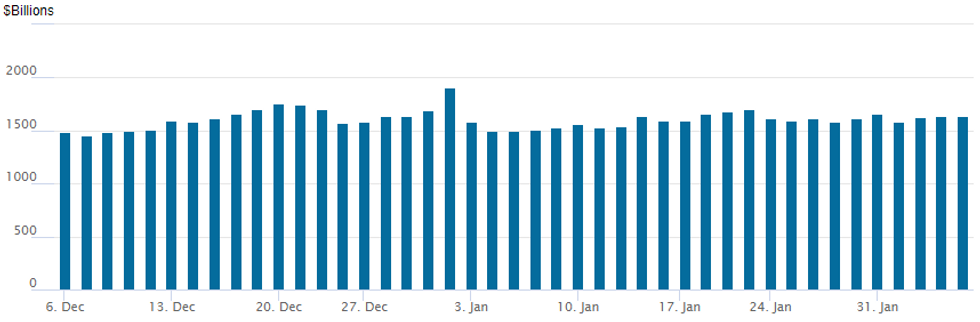

NY Fed reverse repo usage inches higher to $1,642.892B w/79 counterparties vs. $1,640.397B prior session -- remains well off all-time high of $1,904.582B on Friday, December 31.

PIPELINE: Decent Week

Decent week for issuance at $20.62B total despite many sidelined ahead today's Jan employment data and ongoing earnings cycle. Earnings start to wind down next week while some issuers may still opt to withhold issuing more debt ahead CPI inflation metric next Thursday (+0.4% est vs. 0.5% last Month).

- Date $MM Issuer (Priced *, Launch #)

- $2.82B Priced Thursday, $20.62B total for week

- 02/03 $2.02B *McAfee 8NC3 7.375$a

- 02/03 $800M *Scientific Games Holdings 8NC3 6.625%

EGBs-GILTS CASH CLOSE: Hawkishness Increasingly Priced In

Yields continued to soar across the curve Friday as a much stronger-than-expected US employment report dispelled any lingering doubts that the global monetary regime will be much more restrictive in 2022.

- Weakness was evident from the very start of the session as hawkish sentiment carried over from Thursday's ECB/BoE decisions, with short-end Euribor most noticeably being sold as near-term ECB hikes were priced in.

- Periphery EGBs also got hit hard amid ECB tightening prospects; GGB/Bund spread hit the widest since May 2020.

- Long-end Gilts marginally outperformed Bunds though yields ended well up from intraday lows; UK short-end underperformed Germany though.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 8bps at -0.252%, 5-Yr is up 9.1bps at 0.048%, 10-Yr is up 6.1bps at 0.204%, and 30-Yr is up 2bps at 0.352%.

- UK: The 2-Yr yield is up 11.5bps at 1.259%, 5-Yr is up 8.5bps at 1.305%, 10-Yr is up 3.9bps at 1.407%, and 30-Yr is up 2bps at 1.476%.

- Italian BTP spread up 4.4bps at 154.4bps / Greek up 12.1bps at 206.5bps

FOREX: EURUSD Holds Firm Despite Stellar US Employment Data

- An above consensus US NFP print of +467k jobs, accompanied by impressive upward revisions to prior month’s figures, was initially supportive for the US Dollar, recouping losses as US treasury yields spiked following the data.

- Despite the initial USD relief rally, the gains were slowly eroded throughout the session with a bounce in global equity indices also hampering the greenback’s progress. As of writing, the US dollar index is up 0.04%, however, if the index were to slip into negative territory this would represent five consecutive declining sessions.

- The dollar’s most apparent weakness is shown by EURUSD that although marginally lower from the NFP release, remains 0.1% higher for Friday after a morning breach of the 2022 highs to 1.1484. Cluster resistance is seen between 1.1484-1.1495 and the single currency’s resilience on Friday may signal the strong potential for further short-term gains.

- With EUR crosses well supported, the relative dollar strength was seen most notably against AUD and NZD both retreating over 0.75%. Both GBP (-0.44%) and CHF (-0.59%) also came under pressure with USDJPY consolidating above the 115.00 mark, up 0.25% for the session.

- Elsewhere, the Canadian dollar also struggled following a much poorer set of employment figures. Despite consolidating, the USDCAD outlook remains bullish. The recent break of the 50-day EMA has opened 1.2843, as a Fibonacci retracement target. First support is at 1.2650, the Jan 27 low.

- With China returning next week, Monday’s calendar looks fairly light for major data. Of note, ECB President Lagarde is due to testify at a virtual hearing before the European Parliament Economic and Monetary Affairs Committee.

- US CPI will headline the week’s data docket, scheduled for release on Thursday.

Data Calendar for Monday

| Date | GMT/Local | Impact | Flag | Country | Event |

| 07/02/2022 | 0030/1130 | *** |  | AU | Retail trade quarterly |

| 07/02/2022 | 0030/1130 | ** | | AU | Retail Trade |

| 07/02/2022 | 0145/0945 | ** |  | CN | IHS Markit Final China Services PMI |

| 07/02/2022 | 0645/0745 | ** |  | CH | unemployment |

| 07/02/2022 | 0700/0800 | ** |  | DE | industrial production |

| 07/02/2022 | 0700/0700 | * |  | UK | Halifax House Price Index |

| 07/02/2022 | 1545/1645 |  | EU | ECB Lagarde Intro at EU Parliament | |

| 07/02/2022 | 1630/1130 | * |  | US | US Treasury Auction Result for 26 Week Bill |

| 07/02/2022 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 07/02/2022 | 2000/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.