Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI BRIEF: US 2Q GDP Below Expected -0.9%; Spending Slows

- MNI: U.S. Staffing Firms Say Job Openings Data Inflated

- MNI US-CHINA: Biden-Xi Call Maintains Support For "One-China," No Mention Of Tariffs

US

FED: U.S. jobs openings data is inflated and policymakers shouldn't rely on it as a key guide for the path of interest rate policy, staffing companies and economists at labor market data firms told MNI.

- "Duplicate listings, sponsored jobs, and syndication is going on and that has been accelerating in the last five to ten years in the recruitment advertising industry," said Toby Dayton, CEO of LinkUp. "The JOLTS data and the government data unfortunately also has some of those inflated numbers," he said, suggesting it could be inflated by around 2 million openings. For more see MNI Policy main wire at 1024ET.

- White House: "The call was a part of the Biden Administration's efforts to maintain and deepen lines of communication between the United States and the PRC and responsibly manage our differences and work together where our interests align."

- WH: "The two presidents discussed a range of issues important to the bilateral relationship and other regional and global issues, and tasked their teams to continue following up on today's conversation, in particular to address climate change and health security."

- WH: "On Taiwan, President Biden underscored that the United States policy has not changed and that the United States strongly opposes unilateral efforts to change the status quo or undermine peace and stability across the Taiwan Strait."

US TSYS: GDP Contraction Cools Forward Hike Expectations

Rates and stocks rallied after this morning's recession metric cooled: U.S. GDP contracted by 0.9% in the second quarter, far below analyst expectations for a 0.4% gain, driven by decreases in inventory investment, housing and government spending, according to Wed's advance est by Bureau of Economic Analysis.

- Short end rallied/yield curves bull steepened (well off high -14.369, 2s10s at -20.337 after the bell) as expectations over another 75bp hike in Sep cool - 50bp looking more likely at the moment but remain data dependent.

- Balance of rates followed suit, setting modest session highs by midmorning, 30YY at 3.0162% after the bell.

- Tsys hold range after $38B 7Y note auction (91282CFC0) stops through (after three consecutive tails): 2.730% high yield vs. 2.735% WI; 2.60x bid-to-cover vs. 2.48x last month.

- Focus turns to Friday's data calendar w/ Personal Income (0.5% est), Personal Spending (0.9% est), ECI (1.2% est), Chicago PMI (55.0 est) and U-Mich (51.1 est.).

- Fed comes out of blackout tomorrow, still no scheduled speakers as yet - but will most likely see some commentary on networks.

- Currently, the 2-Yr yield is down 13bps at 2.8683%, 5-Yr is down 14.8bps at 2.6945%, 10-Yr is down 11.4bps at 2.6705%, and 30-Yr is down 4.8bps at 3.017%.

OVERNIGHT DATA

- US JOBLESS CLAIMS -5K TO 256K IN JUL 23 WK

- US PREV JOBLESS CLAIMS REVISED TO 261K IN JUL 16 WK

- US CONTINUING CLAIMS -0.025M to 1.359M IN JUL 16 WK

- Consumer spending also slowed to 1.0% in the quarter from 1.8% in the first quarter, the lowest since 2Q 2020 early in the pandemic. Services spending, particularly on restaurants and hotels and health care, picked up but was offset by a decrease in spending on goods.

- PCE inflation, the Fed's preferred indicator for consumer price trends, rose 7.1% in the second quarter, the same as the first quarter. Core PCE inflation edged down to 4.4% from 5.2% in the first quarter

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 381.28 points (1.18%) at 32580.19

- S&P E-Mini Future up 52.25 points (1.3%) at 4076.75

- Nasdaq up 134.2 points (1.1%) at 12167.68

- US 10-Yr yield is down 11.3 bps at 2.6723%

- US Sep 10Y are up 19.5/32 at 121-1

- EURUSD down 0.0014 (-0.14%) at 1.0186

- USDJPY down 2.3 (-1.68%) at 134.27

- WTI Crude Oil (front-month) down $0.21 (-0.22%) at $97.05

- Gold is up $20.92 (1.21%) at $1755.02

- EuroStoxx 50 up 44.42 points (1.23%) at 3652.2

- FTSE 100 down 2.98 points (-0.04%) at 7345.25

- German DAX up 115.73 points (0.88%) at 13282.11

- French CAC 40 up 81.27 points (1.3%) at 6339.21

US TSY FUTURES CLOSE

- 3M10Y -6.88, 27.561 (L: 23.934 / H: 38.039)

- 2Y10Y +1.712, -19.998 (L: -23.044 / H: -14.369)

- 2Y30Y +8.183, 14.716 (L: 4.231 / H: 18.259)

- 5Y30Y +10.084, 32.161 (L: 20.641 / H: 34.406)

- Current futures levels:

- Sep 2Y up 6/32 at 105-9.25 (L: 104-31.875 / H: 105-13.125)

- Sep 5Y up 14.25/32 at 113-23.75 (L: 112-28.5 / H: 113-31.5)

- Sep 10Y up 19.5/32 at 121-1 (L: 119-23.5 / H: 121-08.5)

- Sep 30Y up 17/32 at 143-9 (L: 141-07 / H: 143-27)

- Sep Ultra 30Y down 15/32 at 157-0 (L: 154-25 / H: 158-14)

US 10Y FUTURES TECH: (U2) Key Resistance Cleared

- RES 4: 123-13+ 1.764 proj of the 14 - 23 - 28 price swing

- RES 3: 122-29+ High Mar 31

- RES 2: 121-28+ 1.382 proj of the 14 - 23 - 28 price swing

- RES 1: 121-10 1.236 proj of the 14 - 23 - 28 price swing

- PRICE: 121-03 @ 15:39 BST Jul 28

- SUP 1: 119.19+/118-23+ Low Jul 27 / 50-day EMA

- SUP 2: 117-14+ Low Jul 21 and key near-term support

- SUP 3: 116-11 Low Jun 28

- SUP 4: 115-20 Low Jun 17

Treasuries have traded higher and cleared resistance at 120-16+, the Jul 6 high and bull trigger. The outlook is bullish and the break higher has confirmed a resumption of the current bull cycle. The contract has also established a bullish price sequence of higher highs and higher lows. This opens 121-10 next, a Fibonacci retracement. On the downside, the 50-day EMA, at 118-23+, is a firm support. Key support is at 117-14+, the Jul 21 low.

US EURODOLLAR FUTURES CLOSE

- Sep 22 +0.055 at 96.720

- Dec 22 +0.065 at 96.40

- Mar 23 +0.090 at 96.60

- Jun 23 +0.115 at 96.785

- Red Pack (Sep 23-Jun 24) +0.10 to +0.120

- Green Pack (Sep 24-Jun 25) +0.080 to +0.095

- Blue Pack (Sep 25-Jun 26) +0.080 to +0.085

- Gold Pack (Sep 26-Jun 27) +0.065 to +0.080

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.74000 to 2.30343% (+0.73886/wk)

- 1M +0.00085 to 2.37314% (+0.12085/wk)

- 3M -0.02357 to 2.78229% (+0.01600/wk) * / **

- 6M -0.03000 to 3.34071% (+0.01785/wk)

- 12M -0.04986 to 3.76214% (-0.05215/wk)

- * Record Low 0.11413% on 9/12/21; ** New 3.5Y high: 2.80586% on 7/27/22

- Daily Effective Fed Funds Rate: 1.58% volume: $98B

- Daily Overnight Bank Funding Rate: 1.57% volume: $287B

- Secured Overnight Financing Rate (SOFR): 1.53%, $941B

- Broad General Collateral Rate (BGCR): 1.51%, $385B

- Tri-Party General Collateral Rate (TGCR): 1.51%, $368B

- (rate, volume levels reflect prior session)

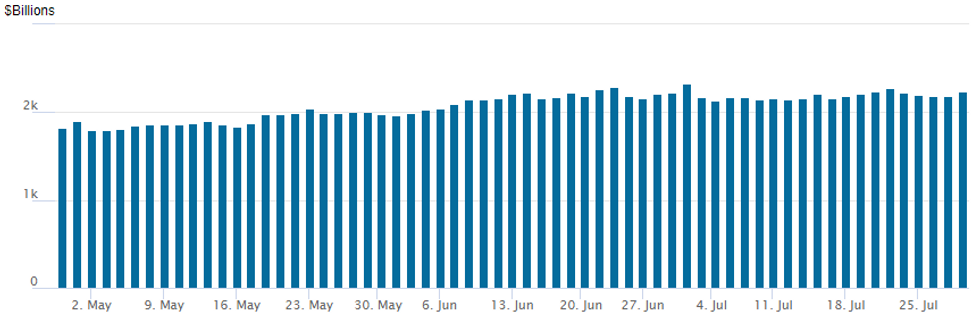

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage climbs to $2,239.883B w/ 111 counterparties vs. $2,188.994B prior session. Record high still stands at $2,329.743B from Thursday June 30.

PIPELINE: $2.25B GM, $1.35B CIBC Launched

$5.1B total to price Thursday, $19.4B total on week

- Date $MM Issuer (Priced *, Launch #)

- 07/28 $2.25B #General Motors $1B 7Y +270, $1.25B 10Y +295

- 07/28 $1.35B #CIBC 3Y +115 (drops 3Y SOFR)

- 07/28 $1B *Posco $700M 3Y +160, $300M 5Y +185

- 07/28 $500M #Appalachian Power 10Y +185

EGBs-GILTS CASH CLOSE: Front-End Yields Crash On Global Growth Fears

European yields collapsed Thursday with many instruments hitting the best levels in 3 months, led by the front end as the rally post-Fed carried through with a disappointing US GDP figure today.

- Growth'/recession fears outweighed higher-than-expected German inflation data.

- Schatz saw one of their biggest-ever rallies (nearly 20bp lower on the session). Gilts were stronger but lagged the Bund rally, with the UK/German 10Y spread testing the April peak.

- Periphery spreads tightened slightly with an easier monetary outlook providing relief.

- Friday sees a slew of data including multiple Eurozone preliminary July CPI reports and Euro area preliminary Q2 GDP.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 19.6bps at 0.248%, 5-Yr is down 18.5bps at 0.523%, 10-Yr is down 12bps at 0.826%, and 30-Yr is down 8.9bps at 1.109%.

- UK: The 2-Yr yield is down 16.3bps at 1.719%, 5-Yr is down 13.8bps at 1.594%, 10-Yr is down 9.3bps at 1.868%, and 30-Yr is down 8.6bps at 2.438%.

- Italian BTP spread down 3.5bps at 234.7bps / Spanish down 2.9bps at 116.4bps

FOREX: USDJPY Sinks To One-Month Low Following Negative US GDP Data

- The market’s dovish reaction following yesterday’s FOMC was exacerbated by disappointing US GDP data on Thursday. The annualized Q/q reading fell 0.9%, well below the surveyed median estimate, sparking a wave of greenback selling following the data.

- The USD weakness was hardest felt against the JPY, with the pair extending its overnight downward trajectory. USDJPY broke through the 135.11 low seen overnight with the pair almost entirely narrowing the gap to key support at 134.26/27 - the 50-dma EMA/ June 23 low. The pair remains down 1.55% approaching the APAC crossover.

- Despite the move in US yields, the USD index remains unchanged on Thursday largely reflected by a mixed reaction among major currencies and an emphasis on the broad-based yen strength. The dovish reaction in US fixed income markets and the subsequent narrowing of yield differentials took the shine off the market’s favourite JPY-short trade and in the face of surging equities, EURJPY and AUDJPY are the weakest pairs on the board.

- Threats to global growth and ongoing headwinds across Europe leaves the technical picture for EURJPY a lot more exposed. Notable support and the bear trigger has been breached below 136.87, the Jul 8 low. A sustained clearance of this level would strengthen bearish conditions and target 136.25 and 135.40 next.

- In similar vein, EURCHF’s break earlier this week below 0.9807 and the 0.98 has seen the pair continue to make fresh cycle lows and print at the lowest levels since the removal of the floor in January 2015, just above 0.9700.

- A flurry of data to finish the week on Friday with multiple Eurozone GDP and Inflation releases, including the Eurozone HICP Flash Estimate.

- In the US, Core PCE Price Index, Employment Cost Index and Personal Income/Spending data will precede the MNI Chicago Business Barometer and UMichigan sentiment figures.

Friday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/07/2022 | 0530/0730 | ** |  | FR | Consumer Spending |

| 29/07/2022 | 0530/0730 | *** | | FR | GDP (p) |

| 29/07/2022 | 0600/0800 | ** |  | SE | Unemployment |

| 29/07/2022 | 0600/0800 | ** |  | DE | Import/Export Prices |

| 29/07/2022 | 0630/0830 | ** |  | CH | retail sales |

| 29/07/2022 | 0645/0845 | *** | | FR | HICP (p) |

| 29/07/2022 | 0700/0900 | * | | CH | KOF Economic Barometer |

| 29/07/2022 | 0700/0900 | *** |  | ES | GDP (p) |

| 29/07/2022 | 0700/0900 | *** | | ES | HICP (p) |

| 29/07/2022 | 0755/0955 | ** | | DE | Unemployment |

| 29/07/2022 | 0800/1000 | * |  | NO | Norway Unemployment Rate |

| 29/07/2022 | 0800/1000 | *** | | DE | GDP (p) |

| 29/07/2022 | 0800/1000 | *** |  | IT | GDP (p) |

| 29/07/2022 | 0830/0930 | ** |  | UK | BOE Lending to Individuals |

| 29/07/2022 | 0830/0930 | ** | | UK | BOE M4 |

| 29/07/2022 | 0900/1100 | *** |  | EU | HICP (p) |

| 29/07/2022 | 0900/1100 | *** | | EU | GDP preliminary flash est. |

| 29/07/2022 | 0900/1100 | *** | | IT | HICP (p) |

| 29/07/2022 | 0900/1100 | *** | | EU | EMU Preliminary Flash GDP Y/Y |

| 29/07/2022 | 1000/1200 | | IT | PPI | |

| 29/07/2022 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 29/07/2022 | 1230/0830 | ** |  | US | Personal Income and Consumption |

| 29/07/2022 | 1230/0830 | ** | | US | Employment Cost Index |

| 29/07/2022 | 1345/0945 | ** | | US | MNI Chicago PMI |

| 29/07/2022 | 1400/1000 | *** | | US | Final Michigan Sentiment Index |

| 29/07/2022 | 1500/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.