Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

MNI INTERVIEW: US Inflation To Linger As Fed Loosens-Warsh

MNI BOC BRIEF: Trudeau Hopes BOC Will Cut Sooner Rather Than Later

MNI INTERVIEW: Investors Jump Gun On BOC Cuts- Ex Deputy Lane

MNI BOE BRIEF: Most Likely Rate Cut This Year - BOE Broadbent

MNI INTERVIEW: Better ONS Data Suggest Easing UK Labour Market

US

INTERVIEW (MNI): US Inflation To Linger As Fed Loosens-Warsh

U.S. inflation could end 2024 well above the Federal Reserve’s 2% target, in part because policymakers’ discussion about cutting interest rates and ending quantitative tightening has already sharply loosened financial conditions, former Fed Board Governor Kevin Warsh told MNI.

NEWS

BOC BRIEF (MNI): Trudeau Hopes BOC Will Cut Sooner Rather Than Later

Canadian Prime Minister Justin Trudeau said inflation figures published earlier on Tuesday make him hopeful the central bank will soon be able to cut interest rates, adding that's not his decision to make and also ruling out slashing government spending to help lower prices

INTERVIEW (MNI): Investors Jump Gun On BOC Cuts- Ex Deputy Lane

Former Bank of Canada Deputy Governor Timothy Lane says some investors are still too aggressive looking for lower interest rates amid stubborn inflation and an economy that continues to confound predictions for a recession.

BOE BRIEF (MNI): Most Likely Rate Cut This Year - BOE Broadbent

A rate cut this year was now the most likely outcome, Bank of England Deputy Governor told the Treasury Select Committee Tuesday, while Governor Andrew Bailey said he saw signs of key inflation components easing.

BOE INTERVIEW (MNI): Better ONS Data Suggest Easing UK Labour Market

Doubts over UK employment data cited as a reason for policy caution by the Bank of England have largely been cleared up, leaving a picture of a gradual easing of the worker shortages which tightened the labour market and crimped economic growth, academic and Office for National Statistics research associate Donald Houston told MNI.

US (MNI): Haley Pledges To Stay In Presidential Race Beyond South Carolina Primary

Longshot Republican presidential candidate Nikki Haley has pledged to stay in the two-horse Republican race with former President Donald Trump beyond Saturday's primary election in her home state of South Carolina - which Trump is tipped to win heavily.

US-RUSSIA (MNI): WH: New Sanctions To Target "Sources Of Revenue For Russian Economy"

White House National Security Advisor Jake Sullivan has told reporters that a new package of Russia sanctions, expected to come on Friday in response to the death of Russian opposition figure Alexei Navalny, will target, "a range of different elements of the Russian defense industrial base and sources of revenue for the Russian economy that power Russia's war machine."

US-TURKEY (MNI): Senate Foreign Relations Members Meet Govt Officials In Ankara

A meeting between a US delegation including Senate Foreign Relations Committee Chair Chris Murphy (D-CT), Senator Jeanne Shaheen (D-NH), and US Ambassador to Turkey Jeff Flake and a Turkish delegation led by Foreign Minister Hakan Fidan is underway in Ankara, Turkey.

ISRAEL (MNI): US Vetoes UNSC Resolution, But Ceasefire Talk Signals Shifting Stance

For the third time the United States has vetoed a United Nations Security Council resolution calling for an 'immediate humanitarian ceasefire' in Gaza.

US TSYS Markets Roundup: Firmer/Narrow Range Ahead Wed's FOMC Minutes

- Treasury futures modestly firmer after the bell, off midmorning highs but holding near last Friday's pre-PPI levels: TYH4 currently +6.5 at 109-30.5 vs. 110-05 high. still below initial technical resistance at 110-17 (Feb 15 high); technical support at 109-17/15 (50.0% of Oct 19 - Dec 27 climb / Low Feb 16).

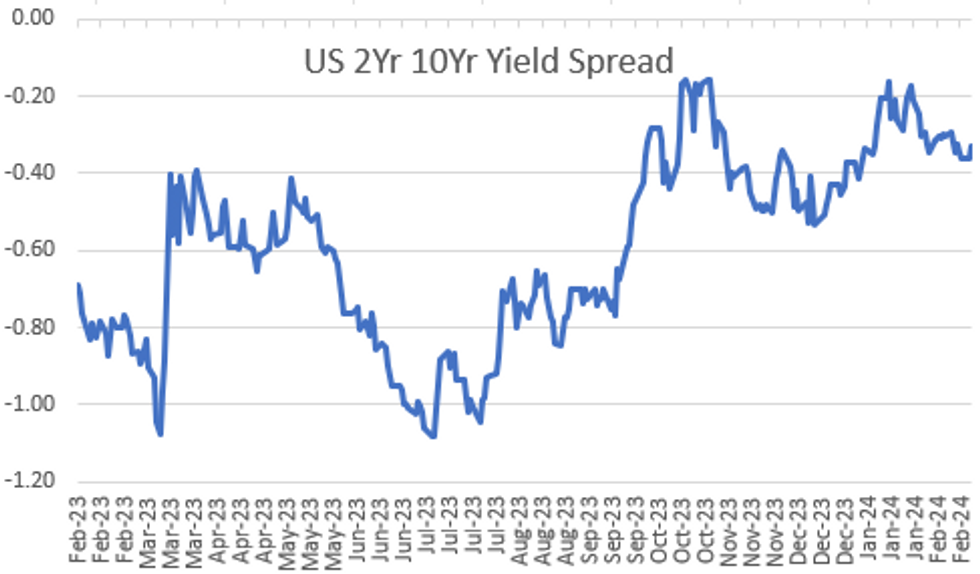

- Curves steeper but off highs: 2s10s +2.801 at -33.652 vs. -31.373 high; 10Y yield currently 4.2714%, -.0078.

- Tsys mirrored modest support in EGBs overnight following a larger than expected 25bp reduction in 5Y LPR during Asia-Pac hours, muted react to softer ECB Q4 negotiated wages to 4.5% from 4.7%.

- Tsys drew additional support after Canadian CPI data came out lower than expected (+2.9% vs. +3.2% est, +3.4% prior). Otherwise, no react to US data: JAN. Leading Indicator -0.4% M/M vs. -0.3% est, US Philly Fed Non-Mfg index -8.8 vs . -3.7 prior.

- No scheduled Fed speakers on today's docket, holding to the sidelines ahead of the Jan 31 FOMC minutes release tomorrow at 1400ET.

OVERNIGHT DATA

US JAN. LEADING INDICATOR FALLS 0.4% M/M; EST. -0.3%

US FEB PHILADELPHIA FED NONMFG INDEX -8.8

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 54.48 points (-0.14%) at 38570.3

- S&P E-Mini Future down 31 points (-0.62%) at 4988.5

- Nasdaq down 173.2 points (-1.1%) at 15601.83

- US 10-Yr yield is down 0.8 bps at 4.2714%

- US Mar 10-Yr futures are up 6.5/32 at 109-30.5

- EURUSD up 0.0031 (0.29%) at 1.081

- USDJPY down 0.11 (-0.07%) at 150.02

- WTI Crude Oil (front-month) down $1.01 (-1.28%) at $78.18

- Gold is up $6.82 (0.34%) at $2024.04

- European bourses closing levels:

- EuroStoxx 50 down 2.79 points (-0.06%) at 4760.28

- FTSE 100 down 9.29 points (-0.12%) at 7719.21

- German DAX down 23.83 points (-0.14%) at 17068.43

- French CAC 40 up 26.67 points (0.34%) at 7795.22

US TREASURY FUTURES CLOSE

- 3M10Y +0.601, -110.448 (L: -114.693 / H: -108.287)

- 2Y10Y +2.801, -33.652 (L: -35.158 / H: -31.373)

- 2Y30Y +4.357, -16.45 (L: -19.622 / H: -13.499)

- 5Y30Y +3.436, 19.44 (L: 16.164 / H: 20.978)

- Current futures levels:

- Mar 2-Yr futures up 2.875/32 at 102-1.5 (L: 101-29.875 / H: 102-03.375)

- Mar 5-Yr futures up 5.5/32 at 106-22 (L: 106-14 / H: 106-26)

- Mar 10-Yr futures up 6.5/32 at 109-30.5 (L: 109-19 / H: 110-05)

- Mar 30-Yr futures up 5/32 at 118-12 (L: 117-22 / H: 118-24)

- Mar Ultra futures up 2/32 at 124-12 (L: 123-22 / H: 124-29)

US 10Y FUTURE TECHS: (H4) Shallow Bounce, Bear Threat Remains

- RES 4: 112-00 Round number resistance

- RES 3: 111-21+ High Feb 5

- RES 2: 110-31+ 20-day EMA

- RES 1: 110-17+ High Feb 15

- PRICE: 110-01+ @ 1400 ET Feb 20

- SUP 1: 109-17/15 50.0% of Oct 19 - Dec 27 climb / Low Feb 16

- SUP 2: 109-05+ Low Nov 28

- SUP 3: 108-19+ 61.8% of the Oct 19 - Dec 27 bull phase

- SUP 4: 108-14 Low Nov 15

Prices recovered slightly through the Tuesday London close, however the shallow bounce does little to counter the over-arching bear threat in Treasuries. The break lower last week confirmed a resumption of the downleg that started Dec 27. The 110-00 handle has been cleared and sights are on 109-17, a pierced Fibonacci retracement that could prove key at the weekly close. A clear break would open 109-05+, the Nov 28 low. Initial firm resistance is at 110-25+, the 20-day EMA.

SOFR FUTURES CLOSE

- Mar 24 +0.003 at 94.713

- Jun 24 +0.020 at 94.970

- Sep 24 +0.025 at 95.290

- Dec 24 +0.035 at 95.620

- Red Pack (Mar 25-Dec 25) +0.045 to +0.060

- Green Pack (Mar 26-Dec 26) +0.040 to +0.055

- Blue Pack (Mar 27-Dec 27) +0.030 to +0.040

- Gold Pack (Mar 28-Dec 28) +0.020 to +0.025

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00443 to 5.32028 (-0.00487 total last wk)

- 3M +0.01172 to 5.32574 (+0.00497 total last wk)

- 6M +0.03525 to 5.26641 (+0.04250 total last wk)

- 12M +0.07159 to 5.0494 (+0.09765 total last wk)

- Secured Overnight Financing Rate (SOFR): 5.30% (-0.01), volume: $1.666T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $681B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $669B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $110B

- Daily Overnight Bank Funding Rate: 5.31% (-0.01), volume: $280B

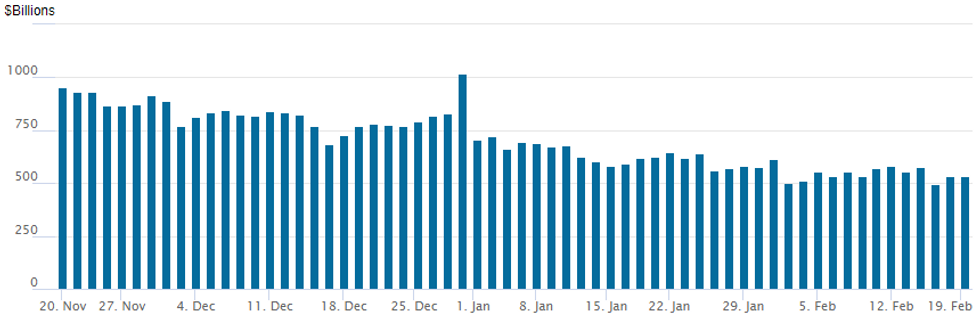

US FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

- RRP usage recedes to $530.879B vs. 532.125B last Friday; compares to $493.065B on Thursday, Feb 15 -- the lowest since early June 2021 .

- Meanwhile, the latest number of counterparties slips to 90 from 94 Friday (compares to 65 on January 16, the lowest since July 7, 2021).

PIPELINE $4.5B HCA Health Care 4Pt Launched

Still waiting for Mizuho and Saudi National Bank 5Y Sukuk to issue.- Date $MM Issuer (Priced *, Launch #)

- 2/20 $4.5B #HCA Health Care $1B 7Y +120, $1.3B 10Y +135, $1.5B 30Y +160, $700M 40Y +170

- 2/20 $1.5B #Marriott Int $500M +5Y +90, $1B +10Y +120

- 2/20 $1.5B #Westpac New Zealand $750M 3Y +75, $750M 5Y +95

- 2/20 $1.4B $American Water Capital $700M 10Y +92, $700M 30Y +107

- 2/20 $1.4B #Georgia Power $500M 3Y +62, $900M 10Y +92

- 2/20 $1B #DTE Electric $500M -3Y +47, $500M 10Y +93

- 2/20 $1B #Verizon 30Y WNG +115

- 2/20 $500M #CBRE Services 5Y +130

- 2/20 $500M *Korea Housing Finance Corp (KHFC) 3.5Y 4.942%

- 2/20 $Benchmark Mizuho 6.25NC5.25 +112, 11.25NC10.25 +130

- 2/20 $Benchmark Saudi National Bank 5Y Sukuk +120a

FOREX Greenback Firmly Off The Lows In Late Session Trade

- While the USD index remains around 0.20% lower on Tuesday, reflective of the lower US yields, the greenback is now well off session lows as we approach the APAC crossover. The greenback bid over the past few hours coincides closely with the weakness for equities with e-mini S&P briefly extending losses to 1.1% on the day.

- Major pairs have seen roughly a 30-pip adjustment which sees USDJPY claw back to the 150.00 mark and EURUSD edge back towards 1.0800. NZDUSD remains the outperformer on the day, still up 0.31%.

- Overall, today’s price action extends NZDUSD's short-term bounce, tipping the pair to print higher highs and higher lows for a fifth consecutive session. Spot briefly rose to a one-month high and notably above first key resistance at the 50-dma of 0.6183. This extends the recovery off the February lows to over 150 pips.

- Elsewhere, the Canadian dollar holds notably weaker following the lower-than-expected CPI - USD/CAD briefly showing to a new daily high of 1.3530 in the aftermath of the data but remaining short of Thursday pre-PPI highs at 1.3552.

- While the CPI was softer than expected on the headline (as well as the core metrics) there are a couple of one-offs here that may suggest this pace of disinflation will not be maintained. This potentially leaves CAD more subject to global sentiment shifts, rather than BoC policy ruminations - as flagged by a number of sell-side desks this week.

- Australian Wage Price Index data will cross first on Wednesday before the UK’s public sector net borrowing figures for January. Focus will then turn to the release of the FOMC minutes before European flash PMIs on Thursday.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/02/2024 | 0001/0001 | * |  | UK | XpertHR pay deals for whole economy |

| 21/02/2024 | 0030/1130 | *** |  | AU | Quarterly wage price index |

| 21/02/2024 | 0700/0700 | *** | | UK | Public Sector Finances |

| 21/02/2024 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 21/02/2024 | 1100/1100 | ** | | UK | CBI Industrial Trends |

| 21/02/2024 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 21/02/2024 | 1300/0800 | | US | Atlanta Fed's Raphael Bostic | |

| 21/02/2024 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 21/02/2024 | 1400/1400 | | UK | BOE's Dhingra MNI Connect Event on BoE projections | |

| 21/02/2024 | 1500/1600 | ** |  | EU | Consumer Confidence Indicator (p) |

| 21/02/2024 | 1630/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 21/02/2024 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 21/02/2024 | 1800/1300 | | US | Fed Governor Michelle Bowman | |

| 21/02/2024 | 1900/1400 | *** | | US | FOMC Rate Decision |

| 22/02/2024 | 2200/0900 | *** | | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.