Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI: Fed’s Waller Determined To Bring Inflation Back To Target

- MNI BRIEF: Fed's Bostic Expects No Recession As Economy Slows

- MNI: Price Views Stable, Households More Pessimistic - NY Fed

NY Federal Reserve

NY Federal Reserve

US

FED: Federal Reserve officials remain uncompromising in their mission to return U.S. inflation back to the central bank’s 2% target, Governor Christopher Waller said in prepared remarks Tuesday.

- “We have reaffirmed this numerical goal repeatedly since 2012, and, in tightening monetary policy since early last year, we’ve made clear that we’re determined to bring inflation down to 2%,” he said at a conference sponsored by the Mercatus Center at George Mason University.

- Market participants are wondering just how much damage to the economy the Fed is willing to inflict if the remaining disinflation is painful. MNI reported earlier this year that officials would consider a possible shift to an inflation target band at its next framework review, which begins next year and will be unveiled in 2025. The Fed has raised interest rates starting in March of last year, bringing them to a 22-year high of 5.25-5.5%.

FED: Federal Reserve Bank of Atlanta President Raphael Bostic on Tuesday reaffirmed his view that the Fed's benchmark interest rate is high enough to get inflation under control without dragging the economy into recession.

- "Our policy rate is sufficiently restrictive position to get inflation down to 2%. We have clearly moved into a restrictive place, the economy is clearly slowing down, and a lot of our policy impact has yet to come," he told the American Bankers Association's annual convention.

- In his quarterly forecasts last month, "I have the economy slowing down, but not moving into a recessionary mode because there's a lot of momentum that was present. And I think that is going to be able to stop a lot of the slowdown." The outbreak of war in the Middle East adds to the list of unanticipated events of recent years and underscores that officials need to be nimble and ready to adapt, he said.

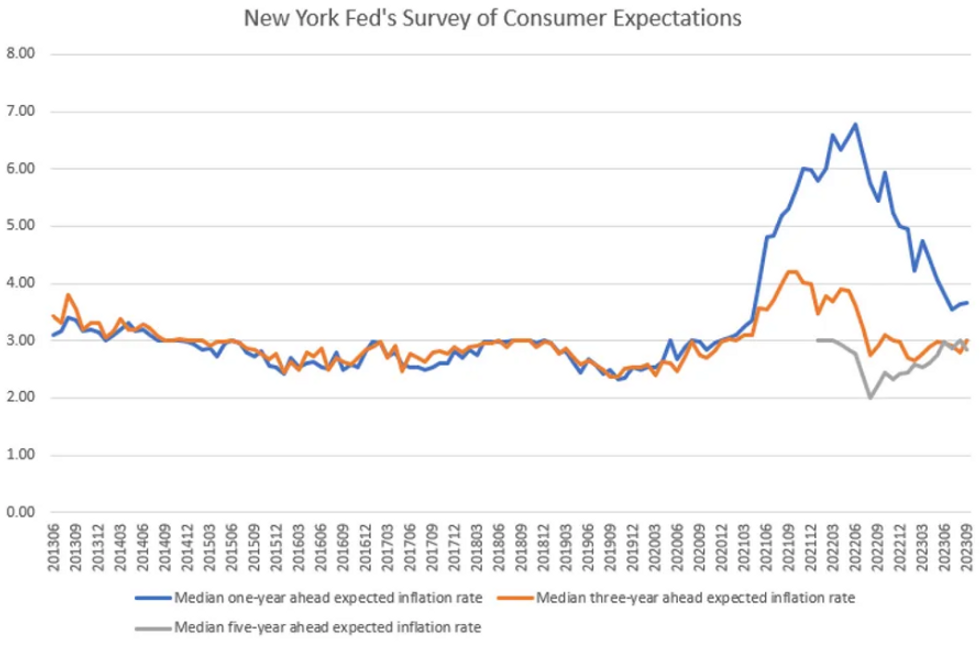

US DATA: U.S. consumer inflation expectations were largely stable in September but households grew slightly more pessimistic about credit conditions and their ability to make minimum debt payments, the New York Fed said in its monthly consumer survey.

- Median inflation expectations rose 0.1 percentage point and 0.2 pp at the one- and three-year-ahead horizons to 3.7% and 3.0%, respectively, according to the bank's Survey of Consumer Expectations. At the five-year ahead horizon, median expectations decreased 0.2 pp to 2.8%. Median home price growth expectations decreased to 3.0% from 3.1% in August, while year-ahead expected college costs decreased sharply to 5.8% from 8.2%.

- Labor market expectations were mixed with unemployment expectations rising but perceived job loss risk improving. Households' perceptions and expectations for credit conditions deteriorated slightly. The average perceived probability of missing a minimum debt payment over the next three months increased by 1.4 pp to 12.5%, the highest reading since May 2020. The increase was largest for respondents below the age of 40, with some college education, and those with an annual household income below USD50k.

US TSYS Fed Tapping Brakes on More Hikes

- Cash Tsys resumed after extended Columbus Day holiday weekend Tuesday, 10Y yield -.1417 vs. last Friday's close at 4.6592%. Curves flattened with Bonds outperforming much of the session: 3M10Y -12.731 at -84.122, 2Y10Y -3.841 at -32.301.

- Tsy futures bounced off session lows following positive comments by Atlanta Fed Bostic as he reaffirmed his view that the Fed's benchmark interest rate is high enough to get inflation under control without dragging the economy into recession.

- Treasury futures pared gains after $46B 3Y note auction (91282CJC6) tailed: 4.740% high yield vs. 4.722% WI; 2.56x bid-to-cover vs. 2.75x prior month. The weak auction coupled with headlines the US is considering sending a second aircraft carrier to Israel spurred additional risk unwinds as stocks moved off midday highs.

- MN Fed Pres Kashkari said after the bell the rise now in 10-year yield "is a bit perplexing; one story is it is higher-growth expectations. We are seeing higher long-term treasury yields, but not higher inflation expectations." Note, SF Fed Daly speaks at the Chicago Council on Global Affairs at 1800ET.

- Rate hike projections into early 2024 held steady to slightly softer vs. late Monday: November steady at 14% (22.2% Mon morning vs. 30.5% late Fri) w/ implied rate change of +3.5bp to 5.364%, December cumulative of 7.5bp (vs. 8.2bp early Tue) at 5.404%, January 2024 5.9bp (vs. 6.4bp early Tue) at 5.387%.

- Wednesday Data Calendar: PPI, Fed Speak, FOMC Sep Minutes.

OVERNIGHT DATA

- US AUG WHOLESALE INV -0.1%; SALES 1.8%

- US REDBOOK: OCT STORE SALES +4.0% V YR AGO MO

- US REDBOOK: STORE SALES +4.0% WK ENDED OCT 07 V YR AGO WK

MARKETS SNAPSHOT

- Key late session market levels:

- DJIA up 156.14 points (0.46%) at 33763.17

- S&P E-Mini Future up 27.25 points (0.62%) at 4396.5

- Nasdaq up 98.2 points (0.7%) at 13583.84

- US 10-Yr yield is down 15.6 bps at 4.6447%

- US Dec 10-Yr futures are down 2/32 at 107-25

- EURUSD up 0.0033 (0.31%) at 1.0601

- USDJPY up 0.2 (0.13%) at 148.7

- WTI Crude Oil (front-month) down $0.44 (-0.51%) at $85.93

- Gold is down $1.74 (-0.09%) at $1859.74

- European bourses closing levels:

- EuroStoxx 50 up 92.66 points (2.25%) at 4205.23

- FTSE 100 up 136 points (1.82%) at 7628.21

- German DAX up 295.41 points (1.95%) at 15423.52

- French CAC 40 up 141.03 points (2.01%) at 7162.43

US TREASURY FUTURES CLOSE

- 3M10Y -13.974, -85.365 (L: -90.292 / H: -78.511)

- 2Y10Y -4.241, -32.701 (L: -33.982 / H: -27.736)

- 2Y30Y -3.324, -15.107 (L: -16.138 / H: -7.742)

- 5Y30Y +0.625, 21.372 (L: 20.466 / H: 25.885)

- Current futures levels:

- Dec 2-Yr futures down 1.5/32 at 101-15.875 (L: 101-12.75 / H: 101-18.25)

- Dec 5-Yr futures down 3.25/32 at 105-12.5 (L: 105-04 / H: 105-18)

- Dec 10-Yr futures down 1.5/32 at 107-25.5 (L: 107-10.5 / H: 107-31.5)

- Dec 30-Yr futures up 5/32 at 112-6 (L: 110-30 / H: 112-19)

- Dec Ultra futures up 15/32 at 116-17 (L: 114-24 / H: 117-00)

US 10Y FUTURE TECHS: (Z3) Post-NFP Recovery Builds

- RES 4: 109-24+ 50-day EMA

- RES 3: 108-26+ High Sep 22

- RES 2: 108-12 20-day EMA

- RES 1: 107-31 High Oct 10

- PRICE: 107-29+ @ 13:21 BST Oct 10

- SUP 1: 106-03+/00 Low Sep 4 / Round number support

- SUP 2: 105-17 2.0% lower 10-dma envelope

- SUP 3: 105-14+ 3.0% Lower Bollinger Band

- SUP 4: 104-26 2.00 proj of the Jul 18 - Aug 4 - Aug 10 price swing

Markets traded firmer into the Monday close, with prices fading - but only slightly - off the week’s high. This builds the post-NFP recovery further. Last week’s lows are yet to be re-tested, and a further stabilization in prices could show signs of a near-term reversal. For now, a bear trend in Treasuries remains intact, with the pressure going through on the back of the NFP release making for a strong negative close. Last week’s fresh cycle lows confirm a resumption of the downtrend and maintain the price sequence of lower lows and lower highs. Support at 107-07, the Sep 28 low, has been cleared signaling scope for the 106-00 handle next.

SOFR FUTURES CLOSE

- Dec 23 -0.005 at 94.580

- Mar 24 -0.005 at 94.720

- Jun 24 -0.015 at 94.950

- Sep 24 -0.025 at 95.230

- Red Pack (Dec 24-Sep 25) -0.035 to -0.035

- Green Pack (Dec 25-Sep 26) -0.035 to -0.03

- Blue Pack (Dec 26-Sep 27) -0.025 to -0.015

- Gold Pack (Dec 27-Sep 28) -0.005 to +0.010

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00770 to 5.34877 (+0.02208 total last wk)

- 3M +0.01903 to 5.42577 (+0.01124 total last wk)

- 6M +0.02993 to 5.48439 (-0.01281 total last wk)

- 12M +0.04918 to 5.44574 (-0.06970 total last wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $100B

- Daily Overnight Bank Funding Rate: 5.32% volume: $248B

- Secured Overnight Financing Rate (SOFR): 5.31%, $1.404T

- Broad General Collateral Rate (BGCR): 5.30%, $565B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $558B

- (rate, volume levels reflect prior session)

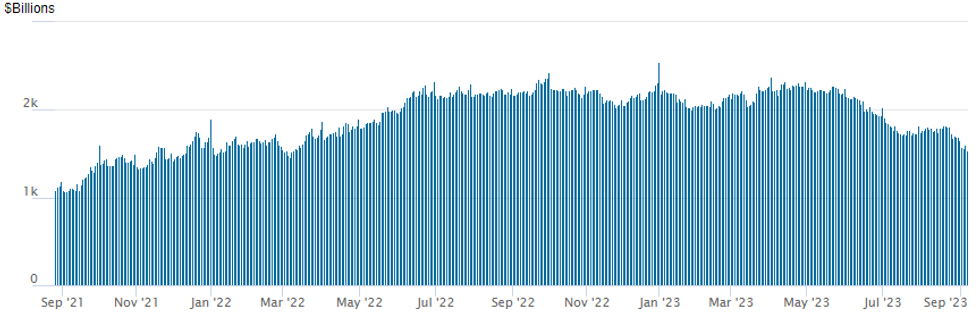

FED REVERSE REPO OPERATION

NY Federal Reserve/MNI

Repo operation usage falls to new cycle low of $1,222.440B (lowest since mid-September 2021) w/98 counterparties vs. $1,283.461B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE $4B BPCE 4Pt Debt Launched

- Date $MM Issuer (Priced *, Launch #)

- 10/10 $4B #BPCE $1.1B 4NC3 +185, $300M 4NC3 SOFR+198, $1.25B 6NC5 +210, $1.35B 11NC10 +35

- 10/10 $4B #Energy Transfer $1B 3Y +130, $500M 5Y +150, $1B 7Y +175, $1.5B 10Y +190

- 10/10 $1B Civitas Resources 7NC3 8.75%a

- 10/10 $500M *General Mills WNG 5Y +103

- Expected to issue Wednesday

- 10/11 $500M JBIC WNG 5Y SOFR+62a

- 10/11 $Benchmark KFW 2Y SOFR+23a, 7Y SOFR+50a

EGBs-GILTS CASH CLOSE: Bunds Underperform, BTPs And Gilts Rally

Gilts easily outperformed Bunds Tuesday.

- With few Europe-specific drivers to price action, focus was again on the prospect of central bank tightening cycles having already reached their conclusion amid an uncertain geopolitical backdrop.

- With limited data, and speakers not really bringing anything new (BoE's Mann late Monday, and ECB's Holzmann maintained characteristically hawkish tones), weakness across EGBs and Gilts through early afternoon was largely a function of a bounce in equities.

- For the 2nd consecutive session, though, early weakness reversed after the US cash equity open, with 10Y German yields falling 7bp from session highs and UK falling 10bp.

- On the day, the German curve twist flattened, with the UK's bull flattening.

- Periphery spreads tightened, led by BTP/Bund leading the way and crashing below 200bp amid positive risk appetite and limited prospects of further ECB tightening.

- Wednesday's data slate is thin (final German CPIs), with more focus on Bund and Gilt supply, speakers including ECB's Knot and Villeroy, and the ECB inflation expectations survey.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany:

- Germany: The 2-Yr yield is up 3.1bps at 3.07%, 5-Yr is up 2.2bps at 2.665%, 10-Yr is up 0.3bps at 2.775%, and 30-Yr is down 1bps at 3.007%.

- UK: The 2-Yr yield is down 3.5bps at 4.799%, 5-Yr is down 4.8bps at 4.426%, 10-Yr is down 5bps at 4.426%, and 30-Yr is down 5.5bps at 4.919%.

- Italian BTP spread down 11.4bps at 195bps / Spanish down 4.8bps at 110.5bps

FOREX Equities Advance Further Weighs On Greenback, EMFX Outperforms

- Despite the most recent downtick, the overall supportive price action for major equity benchmarks, and US yields hitting the lowest levels of the session are weighing on the dollar index, which now sits around 0.4% lower on Tuesday.

- In G10, the likes of EUR and GBP are performing well, both rising around 0.45% and while USDJPY is unchanged on the session, the latest price action has prompted a decent 50 pip selloff for the pair to 148.55.

- USDJPY support at last Tuesday’s low of 147.43, remains intact. The recovery from this level last week is bullish and - for now - the uptrend remains intact. Clearance of 147.43 would be a bearish development and signal scope for a deeper retracement. On the topside, a clear break of the 150.00 handle would be required to reinforce bullish conditions.

- For EURUSD, the pair looks set to finish higher for a fifth consecutive session on Tuesday, showing above the 20-day EMA in the process. As a result, the outlook is beginning to improve for the pair, however momentum measures and the medium-term trend direction remain lower for now.

- The softer greenback and improved sentiment have underpinned a solid recovery for the likes of MXN and ZAR, both rising over 1.3%.

WEDNESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/10/2023 | 0600/0800 | *** |  | DE | HICP (f) |

| 11/10/2023 | 0815/0415 |  | US | Fed Governor Michelle Bowman | |

| 11/10/2023 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 11/10/2023 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 11/10/2023 | 1230/0830 | * |  | CA | Building Permits |

| 11/10/2023 | 1230/0830 | *** | | US | PPI |

| 11/10/2023 | 1415/1015 | | US | Fed Governor Christopher Waller | |

| 11/10/2023 | 1615/1215 | | US | Atlanta Fed's Raphael Bostic | |

| 11/10/2023 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 11/10/2023 | 1800/1400 | * | | US | FOMC Rate Decision |

| 11/10/2023 | 2030/1630 | | US | Boston Fed's Susan Collins |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.