Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI INTERVIEW: US Productivity Boom Can Mask Price Pressures

- MNI US DATA: Mortgage Applications Buoyed By Pullback In Mortgage Rates

- MNI US: Atlanta Fed Wage Growth Tracker Holds At 5.0%

US

INTERVIEW (MNI): US Productivity Boom Can Mask Price Pressures The Federal Reserve appears appropriately wary of counting on the recent U.S. productivity boom to deliver faster growth and contain inflation, as price pressures will reemerge once productivity growth inevitably tapers off, Evan Koenig, former principal policy adviser at the Dallas Fed, told MNI.

- Rising productivity growth as supply chains heal and firms adjust to fewer workers allows the Fed to deliver low unemployment, higher wages and faster growth by offsetting the inflationary effects of tight labor markets. Artificial intelligence could continue to enhance productivity over the long run. But productivity gains can’t protect the economy indefinitely against inflation, he said.

- With trend inflation still running above target at around 3%, the Fed will reduce short rates slowly and only as long as data continue to show demand and labor market tightness easing, Koenig said in an interview.

NEWS

US (MNI): Biden And Trump Secure Overall Majority Of Delegates In 12 March Primaries: Both President Joe Biden and former President Donald Trump crossed the 50% thresholds in their primary election races after results from 12 March contests came in.

MNI INTERVIEW (MNI): Boost To UK Consumer As Inflation Slows-ONS: The outlook for the UK economy has brightened from a year ago, as easing cost-of-living pressures boost consumption, though growth is likely to remain subdued in coming months, Office for National Statistics Chief Economist Grant Fitzner told MNI on Wednesday.

SECURITY (MNI): Finnish PM-Europe Must Take Care Of Own Defense: In an address to the European Parliament Finnish Prime Minister Petteri Orpo has delivered a call for greater defense spending across Europe amid concerns about future US commitment to defending NATO allies under Article 5, especially if Donald Trump wins re-election in November.

DENMARK (MNI): PM Commits To Hitting 2% Of GDP On Defense Next Year Financed By Debt: Danish Prime Minister Mette Frederiksen has committed her gov't to spending 2% of GDP on its own defense from next year, faster than initially planned.

UKRAINE (MNI): Czech Advisor-Artillery Shells To Reach Ukraine By June At Earliest: Euractiv reporting comments from Tomas Pojar, the Czech national security adviser, claiming that first supplies artillery ammunition for Ukraine organized as part of a Czech-led effort would be delivered by June at the latest.

US TSYS Tsys Under Pressure Ahead Thursday PPI, Retail Sales

- Treasury futures extended lows in late NY trade, Jun'23 10Y futures through yesterday's low of 111-02.5 to 110-29 (-8.5), focus on technical support at 110-21 (Low Mar 4). Tsy 10Y yield climbs to 4.1957%, curves near steady to late Tuesday levels, 2s10s +.317 at -43.443.

- No particular headline driver, limited data on the day: MBA Mortgage Applications at 7.1% vs. 9.7% prior. Carryover weakness after Tuesday's higher than hoped for CPI inflation data in the lead up to Thursday's PPI and Retail sales

- Projected rate cut pricing over the next three meetings evaporating: March 2024 chance of 25bp rate cut currently -0.8% w/ cumulative of -0.02bp at 5.328%; May 2024 at -12.4% vs. -14.5% late Tuesday w/ cumulative -3.3bp at 5.297%; June 2024 -59.5% vs. -63% late Tuesday w/ cumulative cut -18.2bp at 5.148%. July'24 cumulative -31.2bp at 4.993%.

- Treasury futures pared losses briefly (USM4 120-17, -7 vs. 120-04 low) after $22B 30Y auction (912810TX6) re-open stops through for the fourth consecutive time: 4.331% high yield vs. 4.352% WI; 2.47x bid-to-cover vs. 2.40x in the prior month. Indirect take-up 69.29% vs. 70.70% prior; direct bidder take-up climbs to 16.77% vs. 14.49% prior; primary dealer take-up 13.93% vs. 14.52%.

OVERNIGHT DATA

US DATA (MNI) Mortgage Applications Buoyed By Pullback In Mortgage Rates: MBA composite mortgage applications increased a seasonally adjusted 7.1% last week.

- It was led by refis (+12%) having previously lagged purchase applications (+5%) in recent weeks.

- Applications have increased 17.5% over the past two weeks but are still 8% below the recent peak from mid-Jan.

- The latest increase came with an 18bp decline in the 30Y conforming rate to 6.84%, closer to the 6.79% averaged through mid-Dec to early Feb after three weeks a little over 7%.

- In a sign of mild tightening for larger borrowing, the regular-jumbo spread pushed a little lower to -20bps, close to its recent low of -29bps from mid-Dec.

US (MNI): Atlanta Fed Wage Growth Tracker Holds At 5.0%: The Atlanta Fed wage tracker was unchanged at 5.0% in Feb (% Y/Y 3mma for median wages).

- Job stayers wage growth held at 4.7%.

- Job switchers wage growth eased three tenths to 5.3%.

- The premium for job switchers narrowed to 0.6pps, although it was briefly lower in mid-2023 when it touched 0.4pps in Aug.

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA up 61.81 points (0.16%) at 39056.62

- S&P E-Mini Future down 3.5 points (-0.07%) at 5235.75

- Nasdaq down 50.3 points (-0.3%) at 16207.99

- US 10-Yr yield is up 4.5 bps at 4.1957%

- US Jun 10-Yr futures are down 8/32 at 110-29.5

- EURUSD up 0.0022 (0.2%) at 1.095

- USDJPY up 0.16 (0.11%) at 147.8

- WTI Crude Oil (front-month) up $2.27 (2.93%) at $79.87

- Gold is up $15.18 (0.7%) at $2174.86

- European bourses closing levels:

- EuroStoxx 50 up 17.35 points (0.35%) at 5000.55

- FTSE 100 up 24.36 points (0.31%) at 7772.17

- German DAX down 3.73 points (-0.02%) at 17961.38

- French CAC 40 up 50.1 points (0.62%) at 8137.58

US TREASURY FUTURES CLOSE

- 3M10Y +3.796, -121.877 (L: -133.288 / H: -121.747)

- 2Y10Y +0.513, -43.247 (L: -45.695 / H: -42.362)

- 2Y30Y -0.109, -27.7 (L: -29.739 / H: -25.867)

- 5Y30Y -0.505, 15.789 (L: 14.947 / H: 17.275)

- Current futures levels:

- Jun 2-Yr futures down 2.25/32 at 102-11.25 (L: 102-11.125 / H: 102-14.25)

- Jun 5-Yr futures down 5.5/32 at 107-4.75 (L: 107-04.75 / H: 107-13)

- Jun 10-Yr futures down 8.5/32 at 110-29 (L: 110-29 / H: 111-10.5)

- Jun 30-Yr futures down 18/32 at 120-6 (L: 120-04 / H: 121-05)

US 10Y FUTURE TECHS: (M4) Pullback Considered Corrective

- RES 4: 113-14 2.0% 10-dma envelope

- RES 3: 112-29+ 76.4% retracement of the Feb 1 - 23 bear leg

- RES 2: 112-10+ 61.8% retracement of the Feb 1 - 23 bear leg

- RES 1: 112-04+ High Mar 8

- PRICE: 111-00 @ 16:20 GMT Mar 13

- SUP 1: 110-30 Low Mar 13

- SUP 2: 110-21 Low Mar 4

- SUP 3: 110-05+/109-25+ Low Mar 1 / Low Feb 23 and bear trigger

- SUP 4: 109-14+ Low Nov 28

A bullish theme in Treasuries remains intact despite this week’s step lower following the US CPI release. The recent upside break of the 50-day EMA and the breach of 111-27, 50% of the downleg off the Feb 1 high, reinforces a bullish theme. A resumption of gains would open 112-10+, the 61.8% retracement. For bears, a stronger reversal lower would return focus back to 109-25+, Feb 23 low and bear trigger. Initial firm support is 110-21, Mar 4 low.

SOFR FUTURES CLOSE

- Mar 24 -0.003 at 94.670

- Jun 24 -0.015 at 94.885

- Sep 24 -0.030 at 95.180

- Dec 24 -0.040 at 95.490

- Red Pack (Mar 25-Dec 25) -0.045 to -0.04

- Green Pack (Mar 26-Dec 26) -0.04 to -0.03

- Blue Pack (Mar 27-Dec 27) -0.025 to -0.02

- Gold Pack (Mar 28-Dec 28) -0.025 to -0.02

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M -0.00011 to 5.32533 (+0.00663/wk)

- 3M +0.00411 to 5.32927 (+0.00843/wk)

- 6M +0.01749 to 5.25075 (+0.02091/wk)

- 12M +0.02823 to 5.01058 (+0.02364/wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.699T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $684B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $676B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $86B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $259B

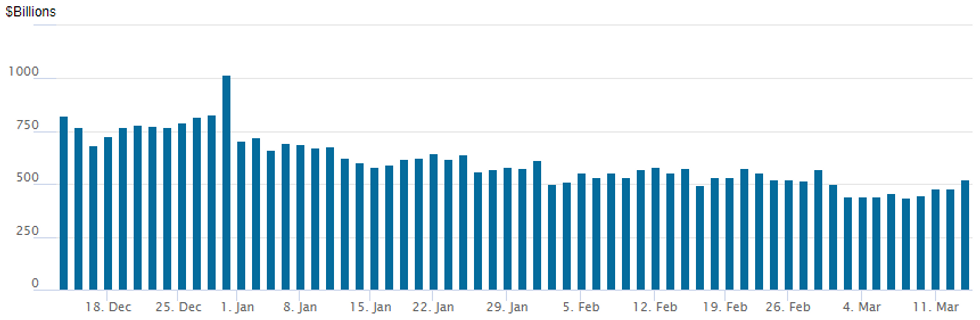

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage rebounds to $521.738B from $476.862B on Tuesday, compares to $436.754B last Thursday - the lowest level since May 2021.

- Meanwhile, the latest number of counterparties inches up to 77 vs. 73 yesterday (compares to 65 on January 16, the lowest since July 7, 2021).

PIPELINE $6.5B Corporate Debt Issuance to Price Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 3/13 $1.5B *Dexia 3Y SOFR+40

- 3/13 $1B #State Street Corp 3Y +60

- 3/13 $1B #Bank of Ireland 6NC5 +142

- 3/13 $1B *Kommunivest WNG 2Y +27

- 3/13 $1B #Nordea Bank $500M 3Y +62, $500M 3Y SOFR+74

- 3/13 $1B #Smith & Nephew $350M 3Y +80, $650M 10Y +125

EGBs-GILTS CASH CLOSE: BTP Spreads Tighten Further

Gilts underperformed Bunds Wednesday, with follow through from the prior session's above-expected US inflation data and heavy supply helping drive core FI weakness.

- Data was fairly limited, with the session's highlight - UK activity data - in line with expectations, and a Eurozone IP miss shrugged off.

- Focus was moreso on heavy auction supply (BTPs, Bund, PGBs, and Gilt linkers among others).

- The outcome of the ECB’s operational framework review brought no notable hawkish surprises, and pointed to slightly easier refinancing conditions versus most expectations.

- The latter dynamic helped periphery EGBs outperform, with 10Y BTP spreads compressing further to the tightest to Bunds in 2.5 years.

- The UK curve bear steepened on the day, with the belly outperforming on a weak German curve.

- Thursday sees multiple ECB speakers (including Schnabel and Knot), alongside largely 2nd tier European data (including final Spanish inflation).

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 4bps at 2.887%, 5-Yr is up 3.3bps at 2.392%, 10-Yr is up 3.6bps at 2.366%, and 30-Yr is up 5bps at 2.522%.

- UK: The 2-Yr yield is up 5.3bps at 4.273%, 5-Yr is up 7bps at 3.941%, 10-Yr is up 7.5bps at 4.021%, and 30-Yr is up 6.4bps at 4.467%.

- Italian BTP spread down 5bps at 122.9bps / Spanish down 1.6bps at 79.5bps

FOREX Greenback Edging Lower, USDMXN Extends Decline To Seven-Month Low

- While equities consolidate at their elevated levels, the short-term path of least resistance remains lower for the greenback, and as such, the USD index is down 0.20% on Wednesday. Ranges and intra-day G10 adjustments have been contained on the session as the dust settled post US CPI and markets await US PPI and Retail Sales data tomorrow.

- However, the solid risk environment continues to bolster the likes of AUD and NZD, with EURUSD also rising 0.25% to trade back above 1.0950, with the pullback earlier in the week appearing to be a correction and a flag formation - a bullish continuation pattern. A resumption of gains would pave the way for a climb towards 1.0998 next, the Jan 5 high. The 76.4% retracement of the Dec 28 - Feb 14 bear leg is at 1.1034. On the downside, initial firm support to watch is 1.0853, the 50-day EMA.

- Emerging market currencies were the main beneficiaries on Wednesday, as the low volatility, high carry trades continued to be favoured. While the HUF and CLP were among the best performers, the Mexican peso made some significant technical progress, prompting USDMXN to trade at a fresh seven-month low. Price action continues to narrow the gap to 16.6262, the Jul 28 2023 low, a breach of which would place the pair at the lowest level since late 2015.

- AUDJPY (+0.37%) trades within reach of the day's highs - but short of the best levels seen last week at 98.21. Strength and clearance here would make cycle highs at 99.06 the next key resistance - but unlikely to come into range in the near-term outside of major dovish BoJ / hawkish RBA surprises next week.

- US PPI, Retail Sales and unemployment claims data headlines Thursday’s economic data calendar, ahead of next week’s busy central bank docket.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/03/2024 | 0700/0800 | *** |  | SE | Inflation Report |

| 14/03/2024 | 0800/0900 | *** |  | ES | HICP (f) |

| 14/03/2024 | 0930/1030 |  | EU | ECB's Elderson at European Banking Federation meeting | |

| 14/03/2024 | 1100/1200 | | EU | ECB's Schnabel Speech at MMCG meeting | |

| 14/03/2024 | 1230/0830 | *** |  | US | Jobless Claims |

| 14/03/2024 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 14/03/2024 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 14/03/2024 | 1230/0830 | *** | | US | PPI |

| 14/03/2024 | 1230/0830 | *** | | US | Retail Sales |

| 14/03/2024 | 1400/1000 | * | | US | Business Inventories |

| 14/03/2024 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 14/03/2024 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 14/03/2024 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 14/03/2024 | 1800/1900 | | EU | ECB's De Guindos fireside chat at Foros |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.